How Vulnerable Is the US Economy to a Geopolitical Shock?

The US-Iran conflict has reignited recession fears. Here's what the data from five decades of geopolitical shocks actually shows about when or how these events matter.

Geopolitical events are almost never the primary driver of the business cycle. They generate headlines, short-term market moves, and a wave of media commentary, eager to connect the dots between a dramatic event and whatever the economy does next. What matters far more than the event itself is the momentum of the underlying economy heading into it.

An accelerating economy can absorb nearly any geopolitical shock without falling into recession. An economy that is already deteriorating is vulnerable to even modest disruptions, because those disruptions only need to add pressure to a cycle that has already turned.

That distinction is critical for evaluating what the US-Iran conflict means for the economy today.

What History Shows

Geopolitical events are most frequently cited as recession triggers in public commentary, but often, they are misread.

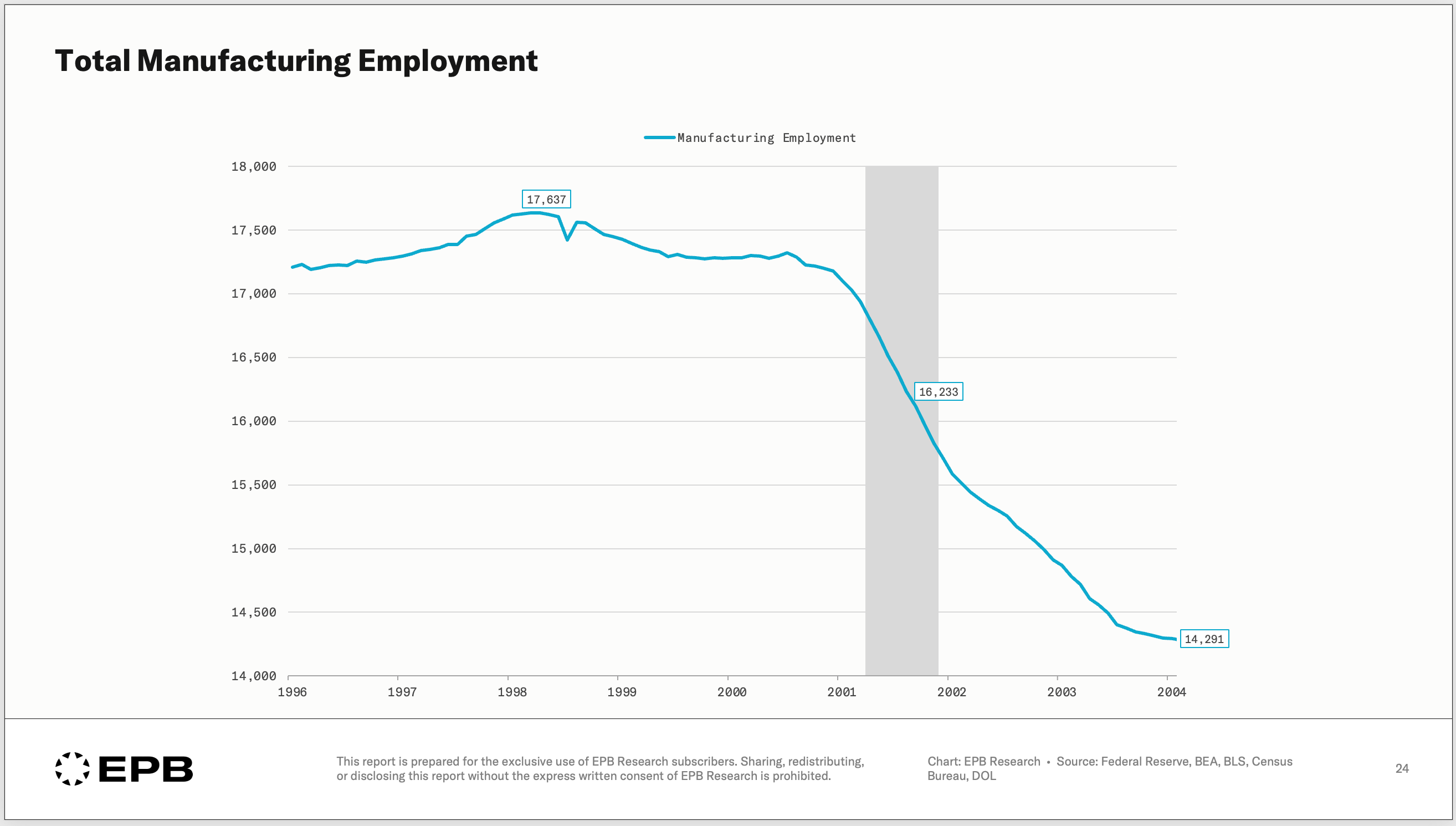

The September 11 attacks did not cause the 2001 recession. Manufacturing employment had already peaked in 1998, more than two years before the attacks occurred.

The devastating attacks caused a legitimate pullback in corporate investment and financial market chaos, but it's clear that a major business cycle deterioration was already well underway.

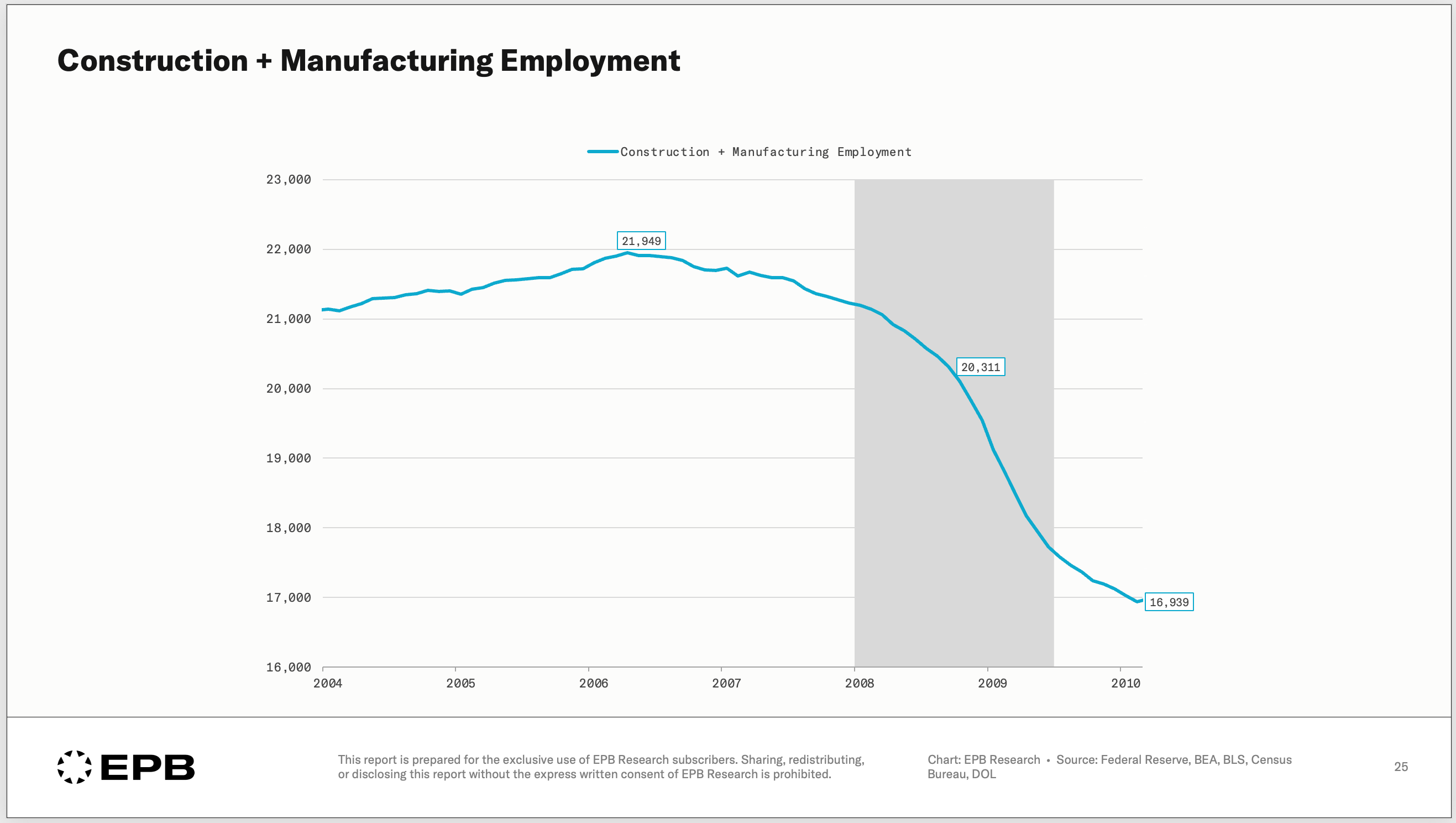

The 2008 oil price spike did not cause the financial crisis. This is often described as the final piece that really broke the consumer.

But again, the cyclical economy had been contracting since 2006, two full years before oil reached its peak. Residential construction had already collapsed. Credit markets were already tightening. The energy shock added pressure to an economy already in serious trouble, but the recession itself had been set in motion years earlier by the housing cycle and the credit conditions that followed.

The pattern across both events is the same. The cyclical sectors of the economy turned first. The geopolitical shock arrived in an economy that was already weakening substantially. The shock accelerated the deterioration rather than causing it.

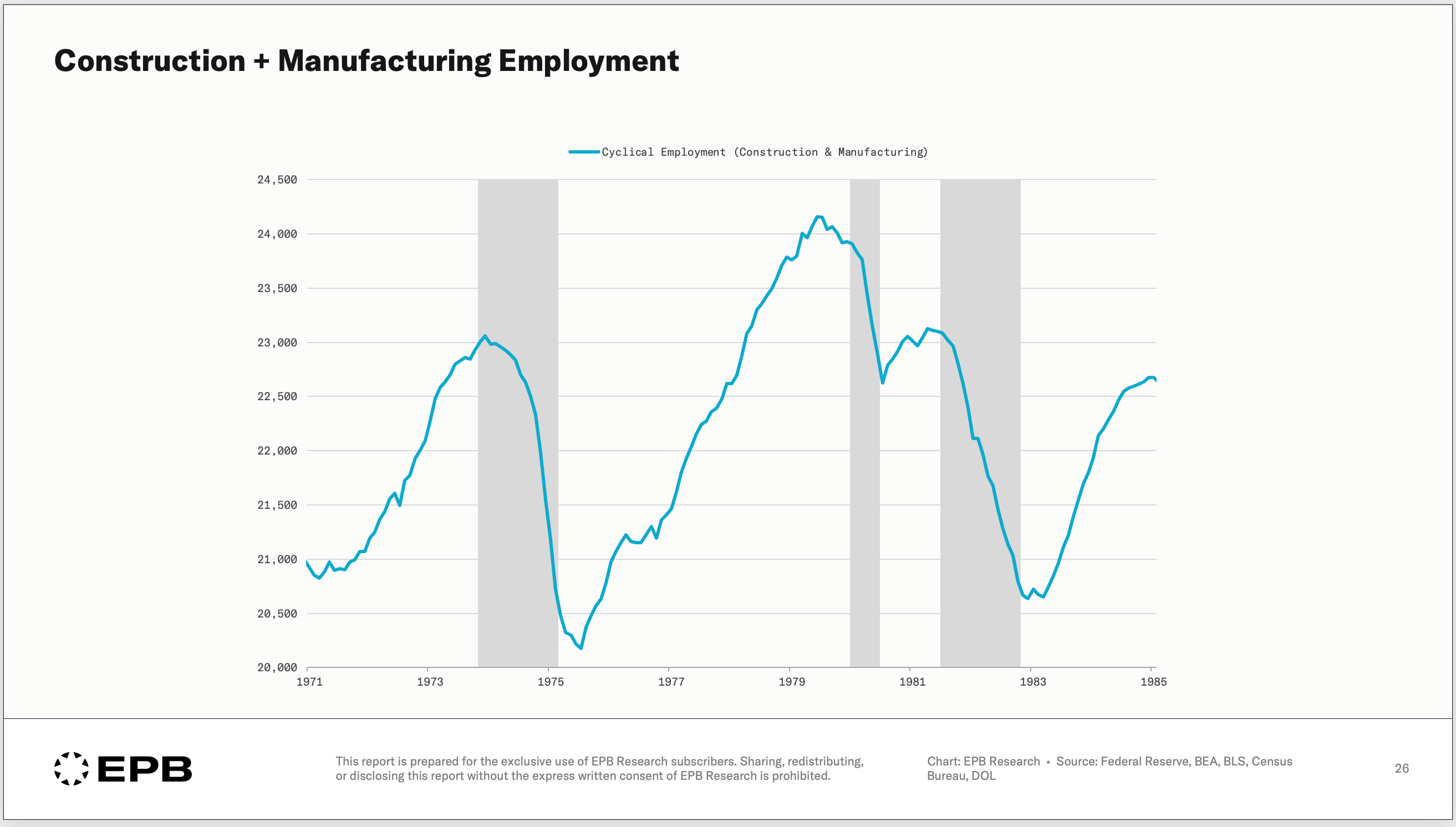

Now, there are also cases where shocks arrived before the cyclical economy had peaked. During the Iranian Revolution in January 1979 and the oil embargo in October 1973, construction and manufacturing employment had not yet reached its cyclical peak at the moment the shocks occurred.

In both cases, the shocks did not immediately produce recessions in the way that later oil shocks did. Let’s explore further.

The Data

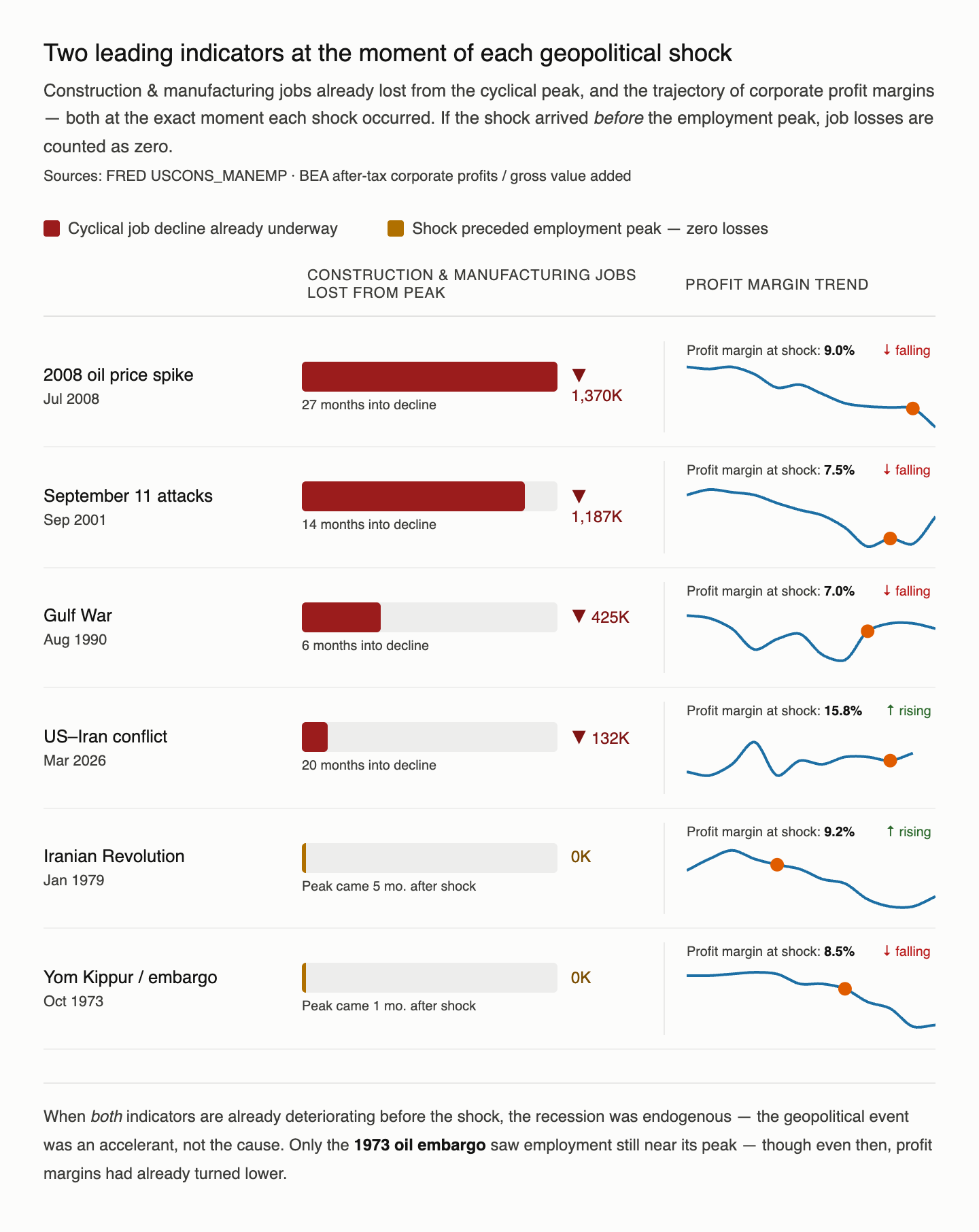

The table below maps two critically important variables at the moment each major geopolitical or oil-related shock occurred: the number of construction and manufacturing jobs already lost from the cyclical employment peak, and the direction/level of corporate profit margins at the time of the shock.

The 2008 oil spike, the September 11 attacks, and the Gulf War, all shared two characteristics. The cyclical economy was already in decline, with hundreds of thousands of jobs already lost, and corporate profit margins were falling at the time of the shock. The two shocks from the 1970s were slightly different.

The economy had not lost jobs, but profit margins averaged about 9%.

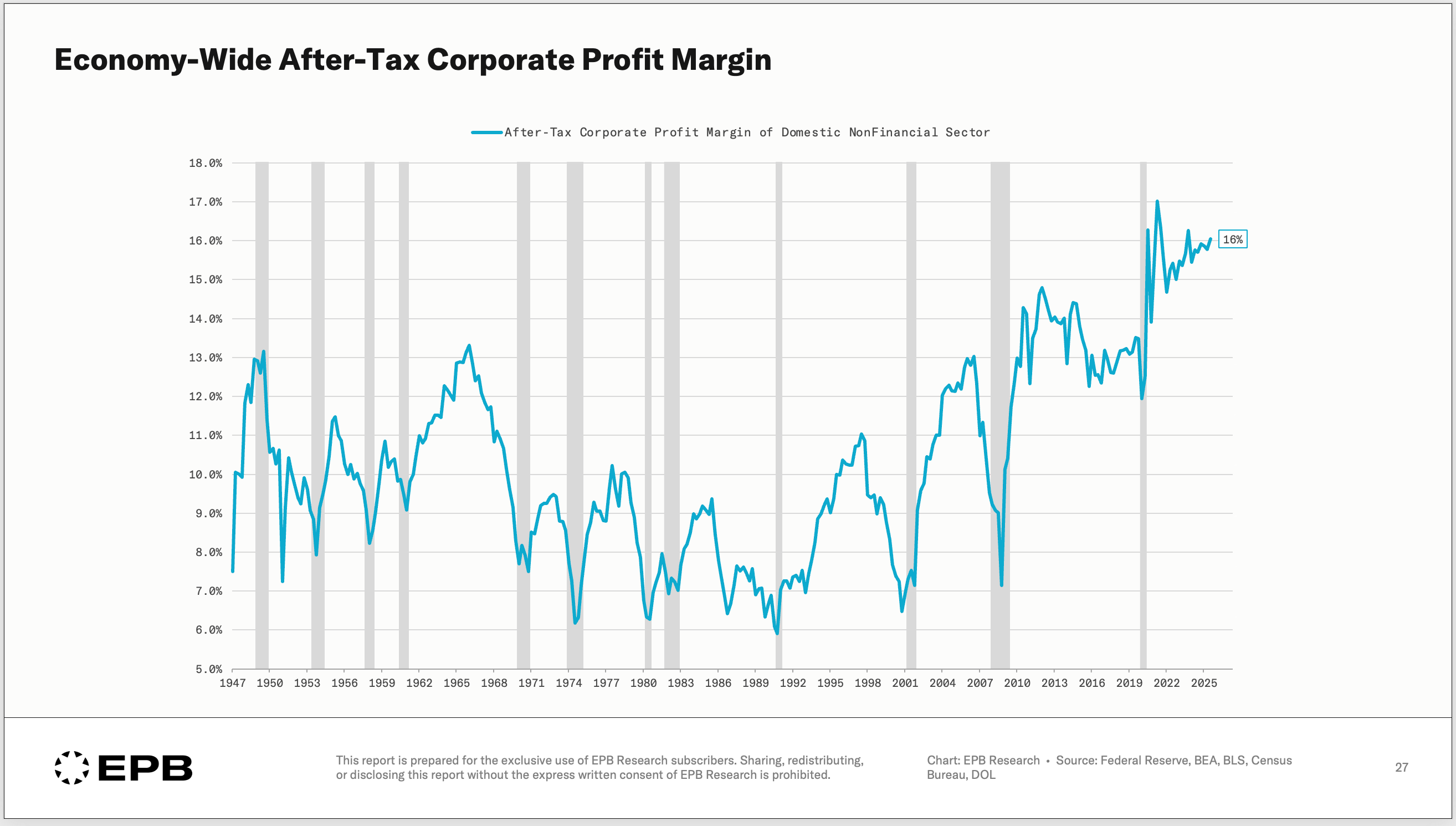

Today’s reading sits in a middle position. The cyclical economy is 20 months into decline with 132,000 jobs lost, which is a real deterioration but nowhere near the scale of 2001 or 2008. At the same time, corporate profit margins are near 15.8%, which is substantially higher than they were heading into any of the recessionary shocks in this dataset.

Is There a Shock Buffer?

Profit margins deserve particular attention because they directly shape how businesses respond to deteriorating conditions. When margins are high, companies have room to absorb revenue pressure by accepting lower profitability rather than cutting payroll, which is a costly and difficult decision to quickly reverse.

When margins are thin, any revenue softness or cost increases force major headcount adjustments for survival.

Heading into the Gulf War, corporate margins were at 7% and falling. Heading into the September 11 attacks, they were at 7.5% and falling. Heading into the 2008 oil spike, they had dropped to 9% and were falling sharply as the housing collapse was already destroying profitability across the financial sector.

Today, margins are at 15.8% and so far, stable. That gap is meaningful. It represents the difference between an economy where businesses are already under pressure and will respond quickly to new shocks, and an economy where businesses have the financial cushion to absorb a period of disruption without immediately eliminating jobs.

Now, it is worth mentioning that profit margins are not evenly distributed across the economy, and the household buffer is extremely thin compared to the corporate buffer.

The Oil Transmission Mechanism

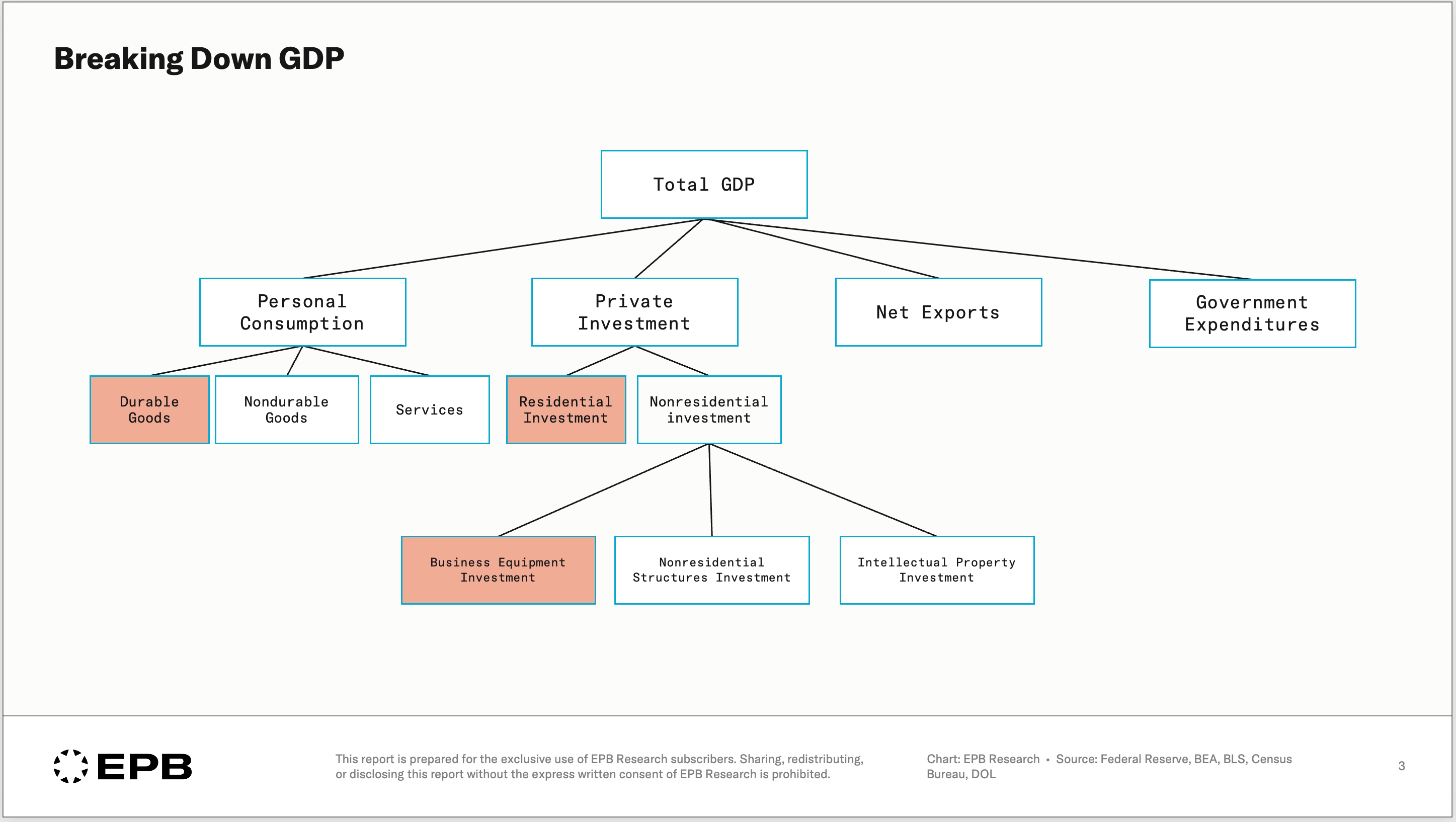

A sustained increase in energy prices can act as a tax on consumer spending or as a profit-margin compressor. When households spend more on gasoline and utilities, they have less to spend on discretionary goods. The first place that reduction shows up in the economic data is durable goods consumption, which are primarily big-ticket and more discretionary-type items.

Durable goods consumption is part of the 20% of the economy that drives all the major fluctuations in economic activity.

If energy prices stay elevated for multiple quarters rather than spiking briefly and reversing, the cyclical economy faces pressure from two directions simultaneously: the existing weakness that has been building since 2023, and a new demand-side headwind from higher energy costs. That combination would be more concerning than either factor in isolation.

The key distinction is between a brief spike and a sustained elevation. Oil markets have moved in response to the conflict, but as of now, the move does not yet represent the kind of prolonged elevation that would register as a meaningful cyclical drag, particularly considering the buffer that is present - at least on the corporate side.

Bottom Line

The US-Iran conflict deserves serious attention. It is a real event with potential economic consequences, particularly through its effect on oil prices and energy costs. But serious analysis requires separating what is knowable from what is speculative, and what is signal from what is noise.

The historical record is clear: geopolitical shocks do not write their own recessions. They accelerate deterioration that is already in motion, or they pass through economies that have the underlying strength to absorb them.

It goes without saying that a shock can be large enough to overcome any set of initial conditions, like economic lockdowns. Shocks definitely come with varying magnitudes, and that matters.

Today, the important cyclical engine of the economy has been weakening for 20 months, which is a real vulnerability. The weakening has been long in duration but mild in magnitude.

On the other side, corporate profit margins are at historically elevated levels.

The economy does not enter this shock from a position of strength in the cyclical sectors, but it also does not enter it with completely depleted buffers that were present in 2001 or 2008.

EPB Research subscribers receive regular updates on the full Business Cycle Sequence, including granular breakdowns of each cyclical component and what the latest data means for monetary policy, corporate profits, and the labor market.

Hello EPB RESEARCH. I am a 77 year old, self-employed sociologist and serial entrepreneur who lives with his wife in Western Colorado. I am benefiting from your scholarship and forethought, because in Colorado, intellectually-curious people are a rarity. Thank you.

Cheers. Levelheaded as always. If only the ideologically 'pure' media would be as calm and collected. Over there, Russia's and China's economies are constantly about to crash, Trump is destroying the world, while our oceans are boiling.

In reality many wealthy western European nations not only have inadequate politicians, slowing economies, failing educational systems and decreasing productivity growth, before 2030 many will experience electricit- black outs and perhaps even rationing because of the EUs and UKs ridiculous energy 'transition'.

In the Netherlands we're already asked to run our washing machines etc at night because the grid is maxed out. New neighborhoods cannot be connected to the grid while businesses can't expand and are put on waiting lists for electricity.

Don’t be surprised if collective farming is next…