AI Investment Is Masking a Weaker Economy

Strip out AI investment and the case for rate cuts becomes difficult to ignore. Key cyclical sectors are still struggling.

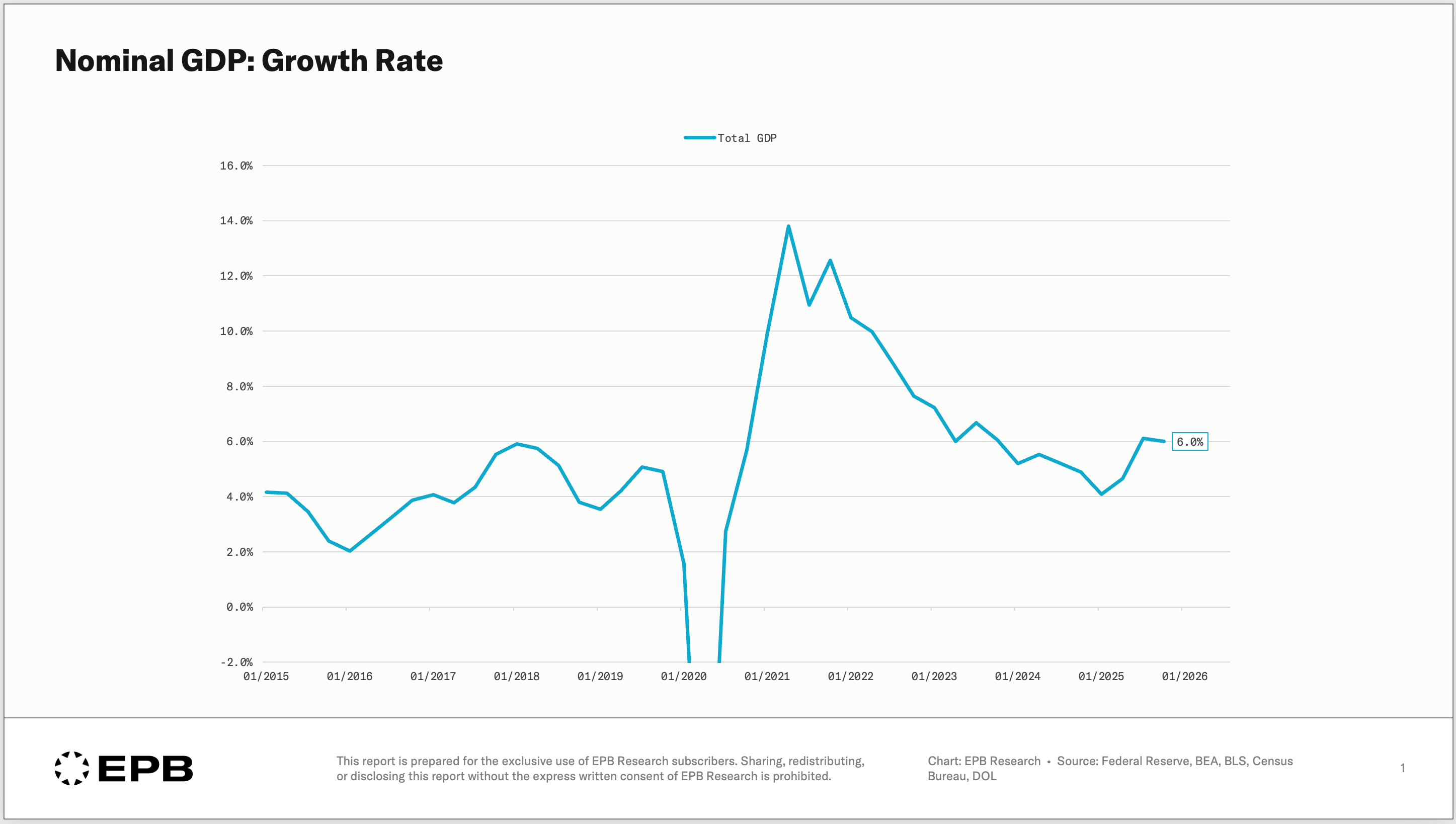

Nominal GDP is growing at 6.0%.

On the surface, this looks like a healthy economy.

A 6% pace of nominal growth is slightly above the pre-pandemic average, and there are no obvious signs of distress in the headline number.

If you stopped your analysis here, you would conclude that the economy is fine and that monetary policy is working.

In fact, the case for rate hikes could even come to the table. But lately, interest rates have been falling, exactly the opposite of what you’d expect from these stronger headline figures.

Stopping your analysis at the headline is exactly how you end up being wrong at the major turning points.

Stripping Away the Noise

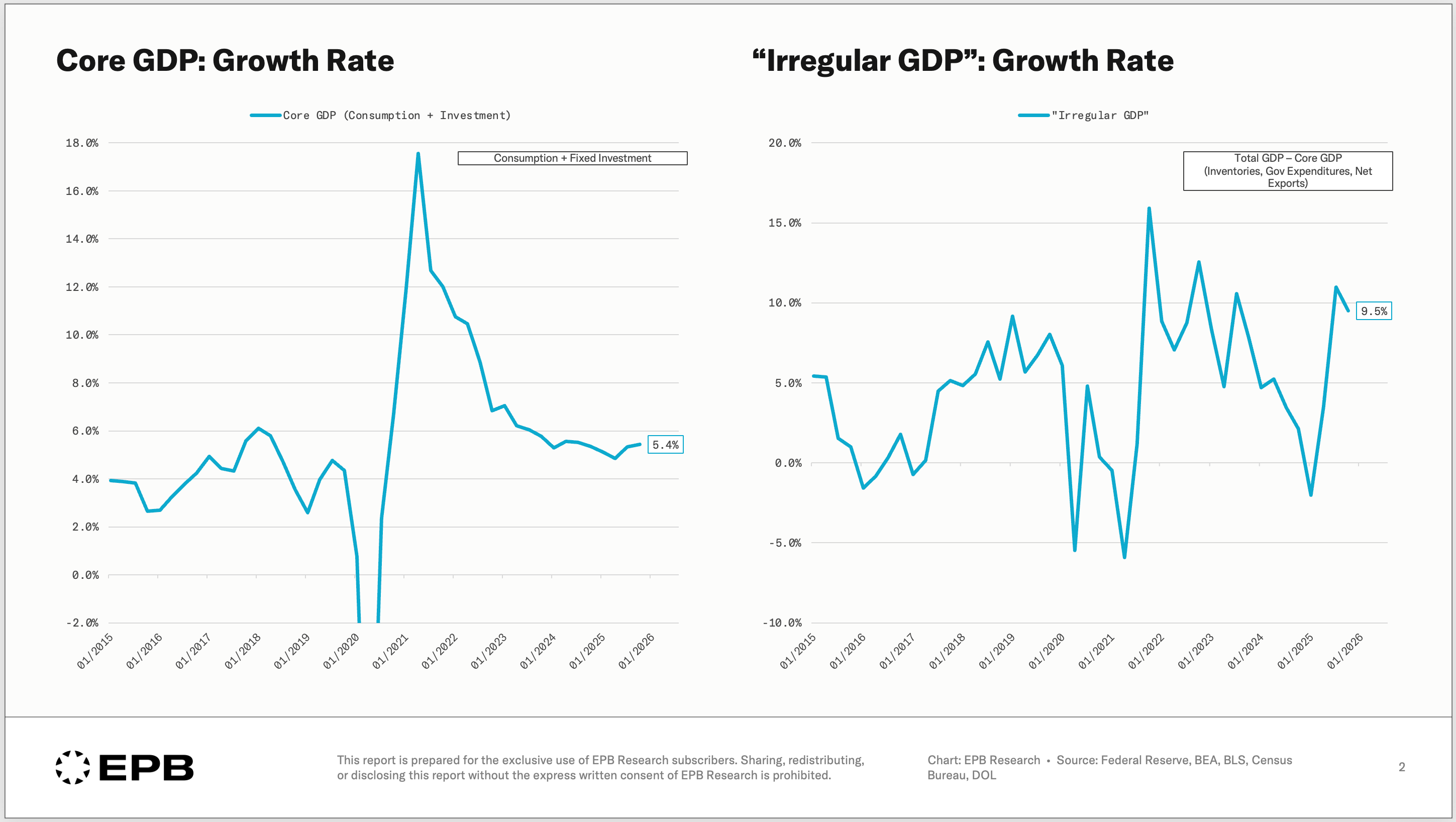

At EPB Research, we don’t like to analyze total or headline GDP.

We break economic growth into layers, removing the components that carry no cyclical signal, until we’re left with the parts of the economy that actually drive the business cycle.

The first cut starts with total GDP and removes inventories, government expenditures, and net exports, which we call “Irregular GDP.”

These components are volatile, policy-driven, and provide almost no useful information about where the private economy is headed. What remains is Core GDP, or simply: consumption + fixed investment.

Core GDP is running at a 5.4% annualzied pace in nominal terms. This is still a reasonably strong pace of growth with no glaring signs of stress. But we’re not done.

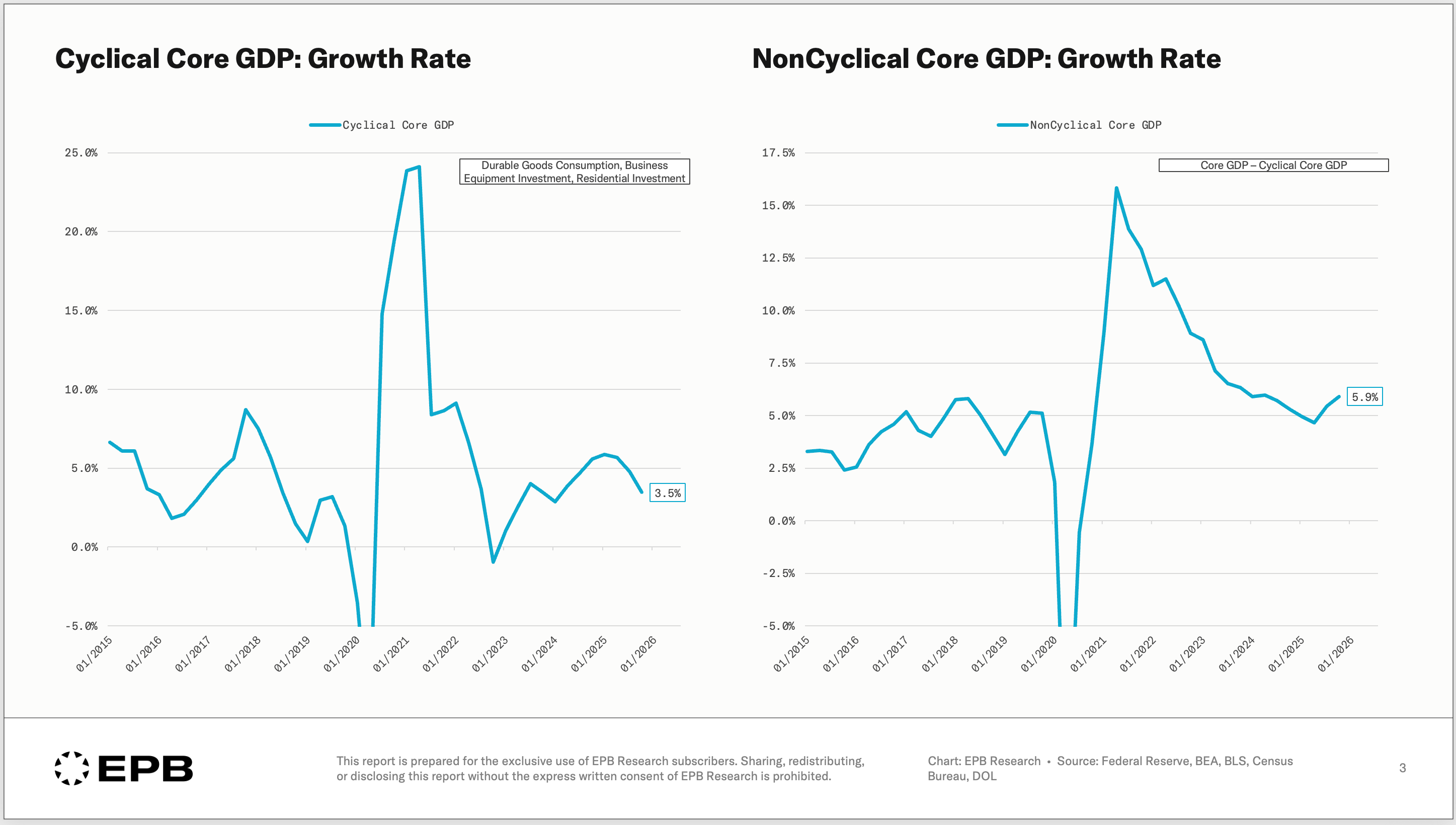

Core GDP breaks into two distinct components: Cyclical GDP and Non-Cyclical GDP.

The non-cyclical portion, which is mostly services consumption and investment in nonresidential structures, is highly stable and not materially impacted by changes in monetary policy.

Non-Cyclical GDP is stable and currently growing at 5.9% in nominal terms. Watching the non-cyclical portion of GDP tells you almost nothing about where the economy is going next because the impacts of monetary policy are not felt in these areas.

The impact of monetary policy is felt in the Cyclical portion of the economy.

The cyclical economy, comprised of durable goods consumption, residential investment, and business equipment investment, is where all the meaningful fluctuation occurs.

This is the 20% of the economy that drives 100% of recessions.

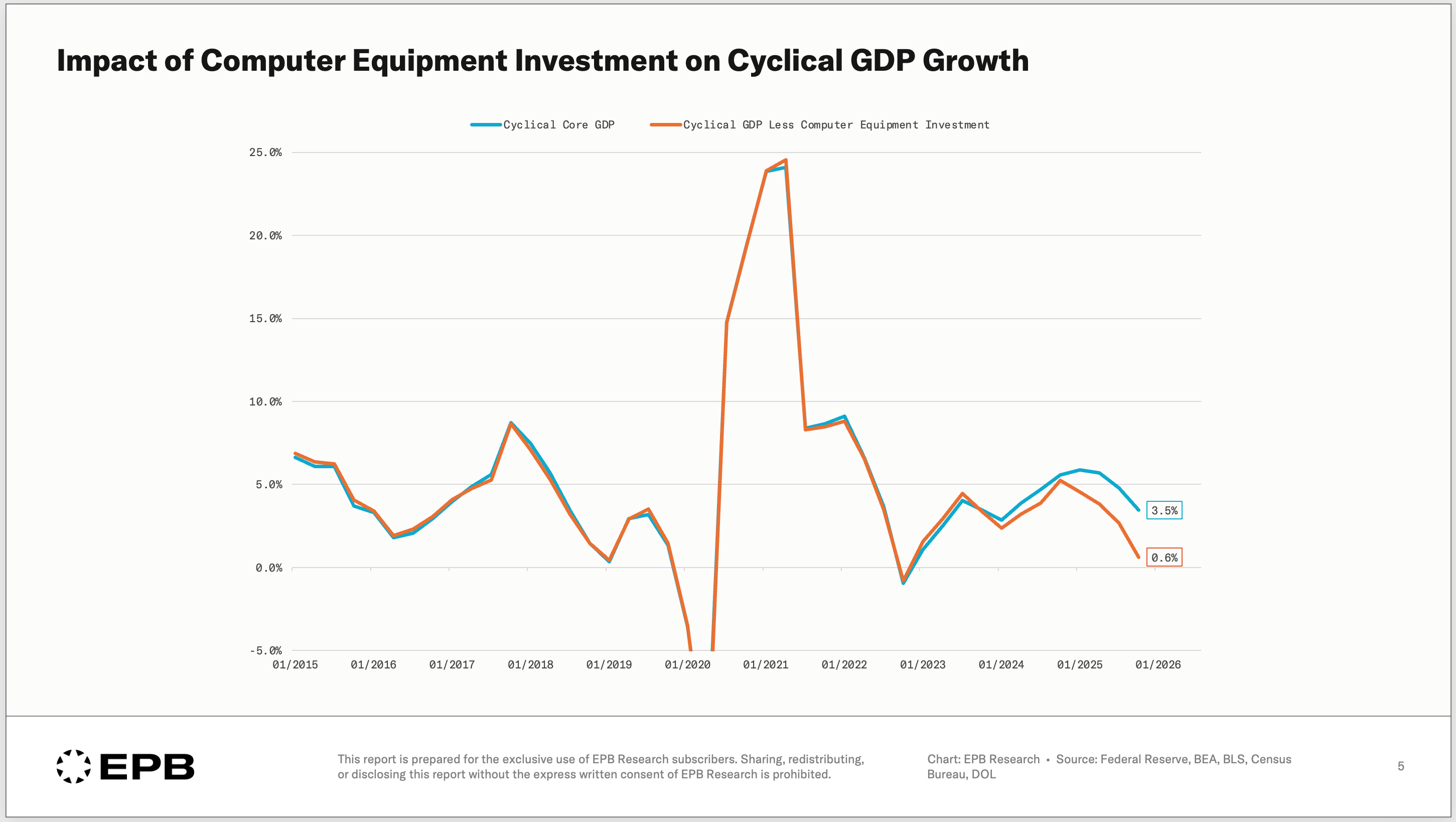

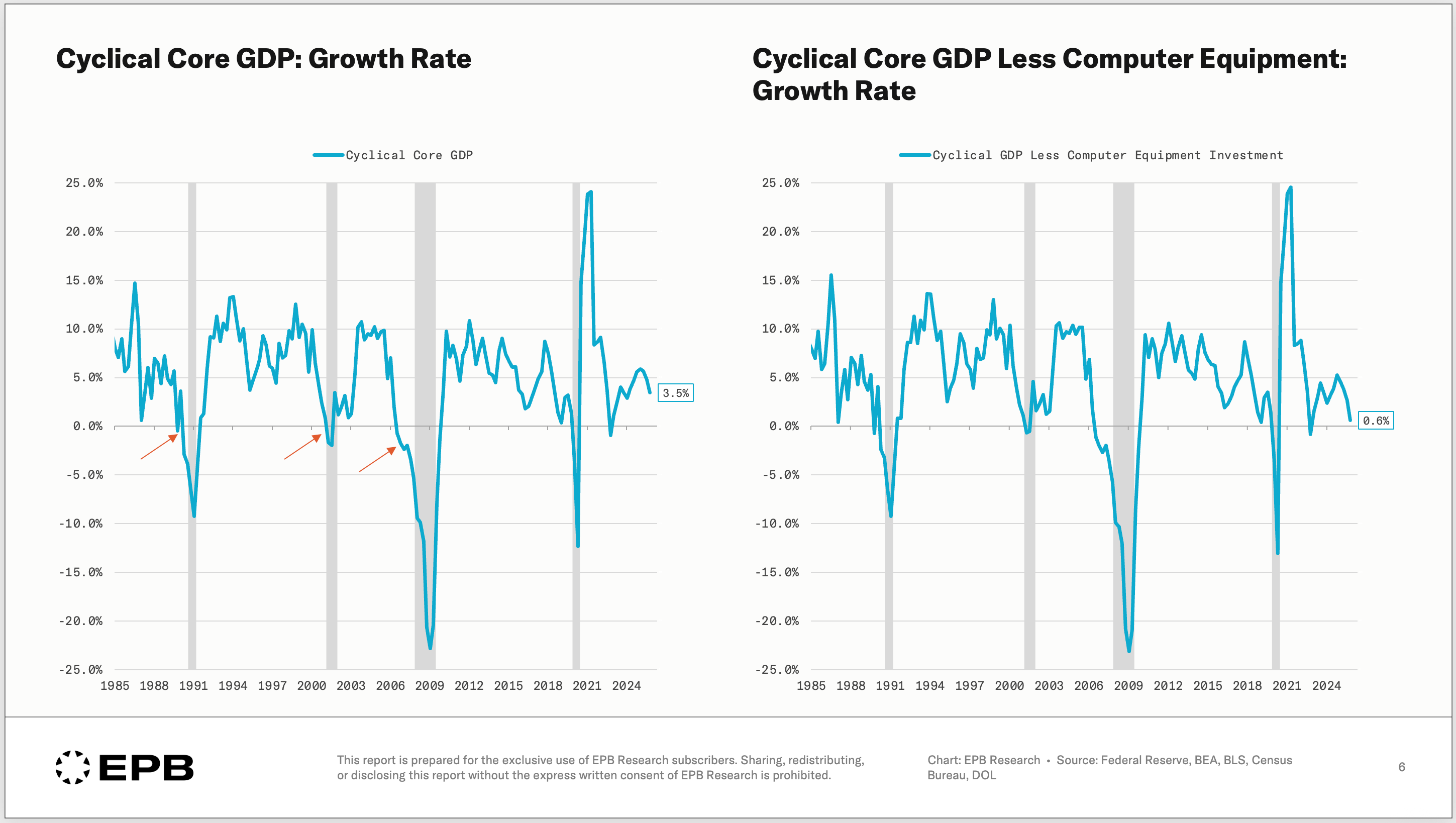

Cyclical GDP is rising at a 3.5% annualized pace, which is actually not alarming on its own. The Cyclical portion of GDP always contracts into recessionary periods - even in nominal dollars - so a 3.5% growth rate is actually reassuring.

But it’s what’s inside that 3.5% that matters.

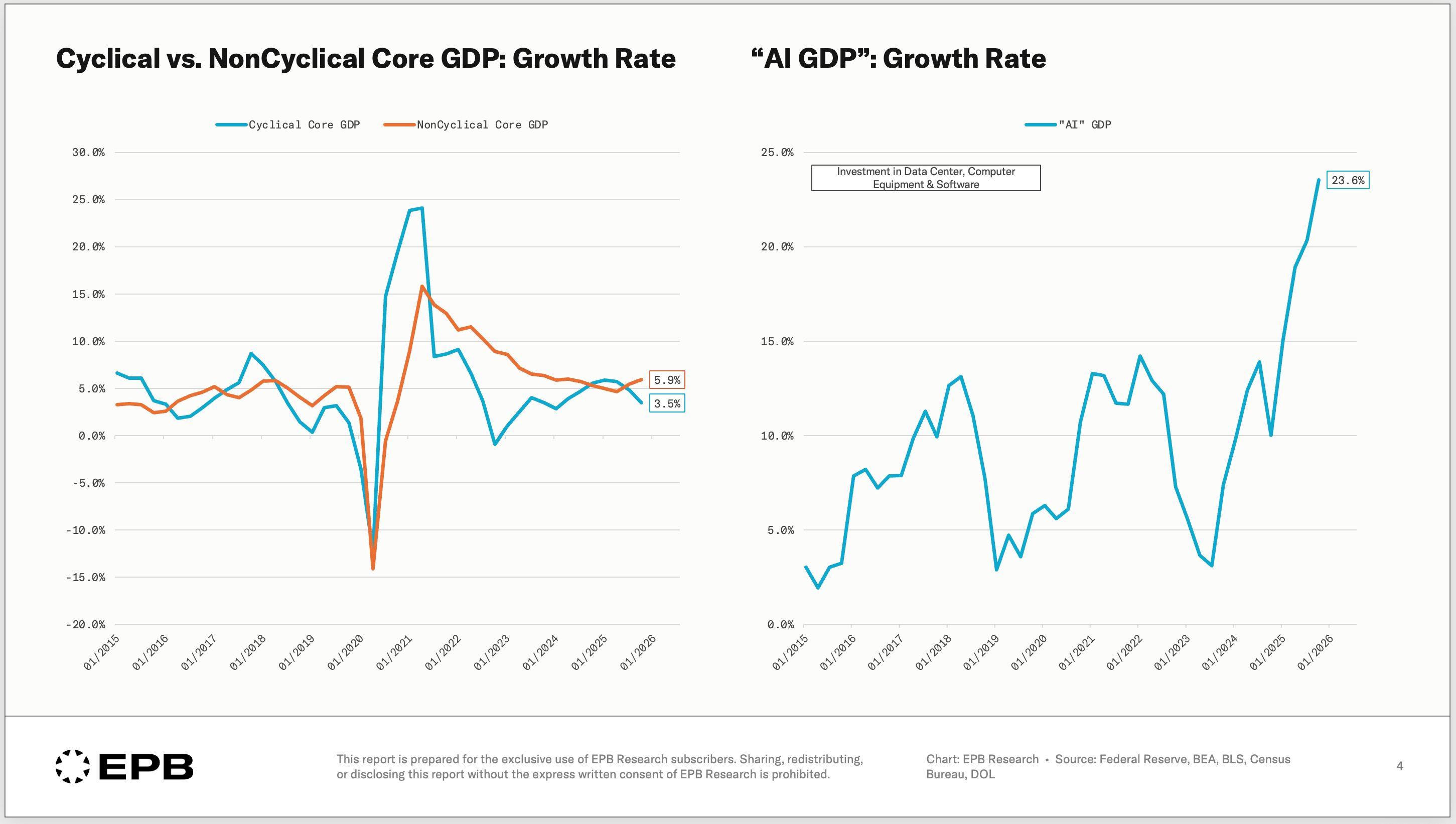

The AI Distortion

While it’s very difficult to isolate the specific parts of the GDP accounts directly affected by AI spending, we can roughly approximate the impact by examining the growth rates of data center investment, computer equipment investment, and software investment.

These three buckets of GDP, what we call “AI GDP,” are growing at a whopping 24% annualized pace, exploding since late 2023.

This is clearly an extraordinary growth rate, reflecting a massive wave of capital expenditure on AI infrastructure from the world's largest technology companies.

Isolating this category of growth is not to say it doesn’t matter. Quite the opposite. This is real investment and real economic activity.

The Impact on Cyclical GDP

Cyclical GDP measures durable goods consumption, business equipment investment, and residential investment.

Computer equipment investment is a very narrow slice of business equipment investment and a driver of our “AI GDP” bucket.

When we strip out computer equipment investment from Cyclical GDP, the growth rate falls from 3.5% to 0.6%. Computer equipment investment represents just 6% of Cyclical Core GDP, yet it accounts for nearly the entire difference between a cyclical economy that looks relatively stable and one that is essentially stagnant and flashing recession.

In the chart above, for most of the period from 2015 through 2019, Cyclical GDP and Cyclical GDP less computer equipment tracked each other closely. The gap between them was minimal, and that made sense since computer equipment was just 6% of the total.

Today, that gap is as wide as it has ever been, and it's masking real weakness within the traditional interest rate-sensitive sectors that are in need of policy support.

What the Rest of the Cyclical Economy Is Saying

Without the major contribution from computer equipment investment and Cyclical GDP is on the verge of contraction.

Historically, nominal contractions in Cyclical GDP are recessionary. There was a brief and minor contraction in 2022, but the labor market was strong, and this was largely driven by the exhaustion of pent-up demand during the COVID-spending spree that was quickly reversed.

The interest rate sensitive, big-ticket parts of the economy that respond most directly to monetary policy have been under sustained pressure.

Why This Matters for Monetary Policy

It is clear that the cyclical economy, stripped of AI investment, is not overheating. It is barely moving. These sectors are in need of monetary policy support as they are the traditional engine of economic growth.

The counterargument is that AI investment is still economic activity, still generating income, still supporting employment in technology and construction, and that is true.

The question is not whether AI investment is real today. The question is whether it can sustain its current pace indefinitely and whether it can continue to offset weakness in every other part of the cyclical economy.

The Bottom Line

Now, it’s not accurate to say that AI investment is keeping the economy out of recession, despite all the charts and data we have just reviewed. Cyclical GDP excluding computer equipment investment is still not contracting, but it’s decelerating and stagnating, and the risk is that it will continue to slide.

This would be a different conversation if Cyclical GDP was contracting at -5%, but the economy was still avoiding recession. That is likely what you’d think if you only listened to mainstream analysis, but that is not supported by the data.

The facts are that total GDP is running at a 6% nominal pace. The ever-important Cyclical portion of GDP is growing at a 3.5% pace, but if we remove a narrow 6% slice of computer equipment investment, we drop to a stagnant 0.6% (negative in real terms).

That is not a sign of broad economic strength. It is a sign of an economy that remains more dependent on monetary policy support than the aggregate data suggests.

Hopefully, the head-scratching decline in interest rates amongst seemingly strong headline figures should be less confusing after this growth breakdown.

EPB Research subscribers receive regular updates on the full Business Cycle Sequence, including granular breakdowns of each cyclical component and what the latest data means for monetary policy, corporate profits, and the labor market.

Great note EPB!

This week former ABN AMRO chief economist and now independent commentator Han de Jong showed the US AI capex boom in Dutch export figures:

'Alleged AI bubble visible in our exports

The volume of Dutch goods exports was 7.1% higher in December than a year earlier. This isn't a unique percentage, but historically, and aside from the "echo" of the coronavirus pandemic, it is quite exceptional, as shown in the first graph. For 2025 as a whole, the growth in Dutch goods exports was 3.3%, much better than the 1.8% decline in 2024. This growth, and especially the 7.1% figure in December, is remarkable, given the geopolitical developments.

In response to the import tariffs announced by Donald Trump on April 2nd, "Liberation Day," the IMF lowered its forecast for world trade growth in 2025 from 3.25% to 1.7%. However, according to monthly figures from the CPB (Netherlands Bureau for Economic Policy Analysis), global goods trade grew by a remarkable 4.4% up to and including November of last year. Such an IMF forecast is a major blunder. It also shows that while our exports performed very well in 2025, we are certainly not alone in this.

CBS reports that machinery made a significant contribution to the strong export growth in December. The following graph shows production trends in the mechanical engineering and chemical industries. As elsewhere in Europe, production in the chemical industry has declined sharply in recent years. In December, production was around 25-30% lower than before the European gas price surge in 2022. And just like in Germany, there's no sign of any recovery, even though the European gas price has fallen sharply in absolute terms compared to 2022. Policymakers show little urgency in halting or reversing this trend. The pursuit of strategic autonomy is apparently of little relevance here.

The graph also shows that production in mechanical engineering rose sharply from 2017 to 2023, then fell back, but picked up sharply again from mid-2025 onwards. Note that the axes in the graph differ in scale and that the growth in production in mechanical engineering is much stronger than the decline in the chemical industry. In December 2025, production volume in mechanical engineering was approximately three times higher than in January 2017. Production was also almost 7% higher than in June. This is therefore consistent with the export figures.

It is almost inevitable that the IT sector is the driving force here, and in particular everything related to artificial intelligence. ASML's excellent operating results for the last quarter of 2025, for example, and the company's positive expectations for the near future are consistent with this. Elsewhere in the world, you also see all sorts of signs of the strong and accelerating growth in investments in AI.'

https://crystalcleareconomics.nl/index.php/2026/02/17/vermeende-ai-bubbel-zichtbaar-in-onze-export/