Where U.S. Growth Went

The Hidden Link Between Government Size, Vanishing Net Investment, and Stagnant Real Incomes

The US economy can no longer generate the real income gains or improvements in the general standard of living it once did, which fueled a sense of optimism and prosperity.

As real income gains continued to fall short of society’s expectations, calls for government solutions grew louder, but ultimately, these efforts worsened the problem.

The main issue is that real income growth is tied to productivity gains, and sustained increases in productivity growth require what’s called “capital deepening,” or more (and better) machinery, equipment, and physical infrastructure for workers, allowing each person to produce more in the same amount of time.

This capital deepening process requires continued investment in physical goods and infrastructure, and over the last several decades, the US economy has invested less and less in these critical areas.

In this post, we’ll explore why the rate of private investment has been declining, how this has impacted our population's standard of living, how we can fix it, and where the economy is heading if we don’t.

How The Standard of Living Improves

The standard of living or the perception of prosperity improves when real income grows at a sufficient pace for the average person. Real income, or income after accounting for inflation, is tied to productivity growth.

An economy can only consume what it produces (not counting the trade deficit…we will get there).

If you want to consume more, you have to produce more. Producing more per hour is productivity, and that’s the only way real incomes rise.

If wages go up but productivity doesn’t, prices just rise to match the increase in wages. You earn more dollars, but it buys the same amount of stuff, and nothing changed.

To produce more, it's helpful to have more and better equipment, machinery, or infrastructure to work with.

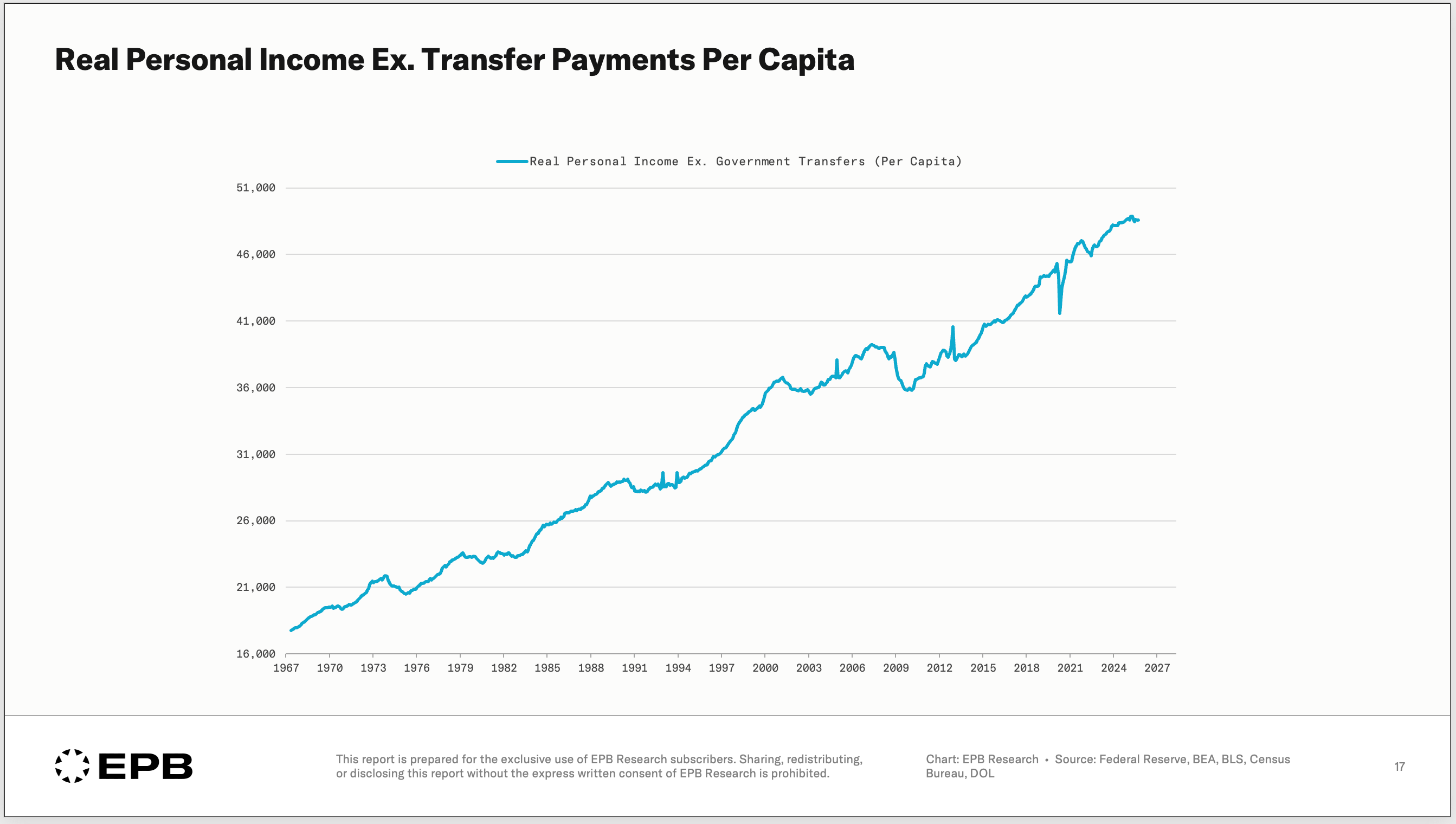

This chart shows real personal income per capita excluding government transfer payments. Essentially, we are measuring all the income the private sector can generate on its own, adjusted for inflation, per person. At the end of 2025, this amounted to roughly $48,500 per person. We’ll refer to this measure simply as real income.

Real income has increased over time, rising from $20,000 in the early 1970s to almost $49,000 today. It’s essential that real income increases over time, but the rate of increase is what’s really critical and easy to lose sight of.

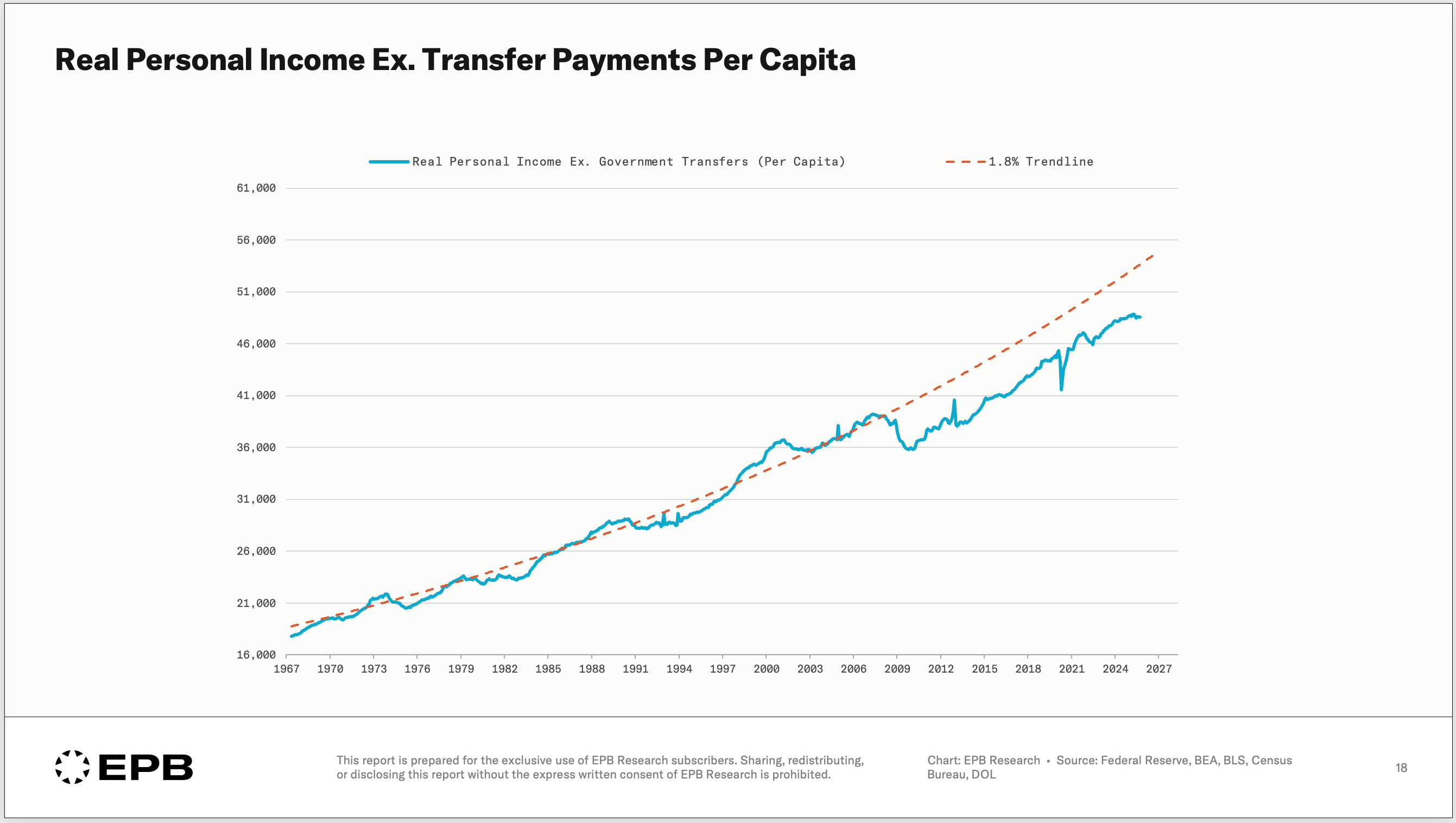

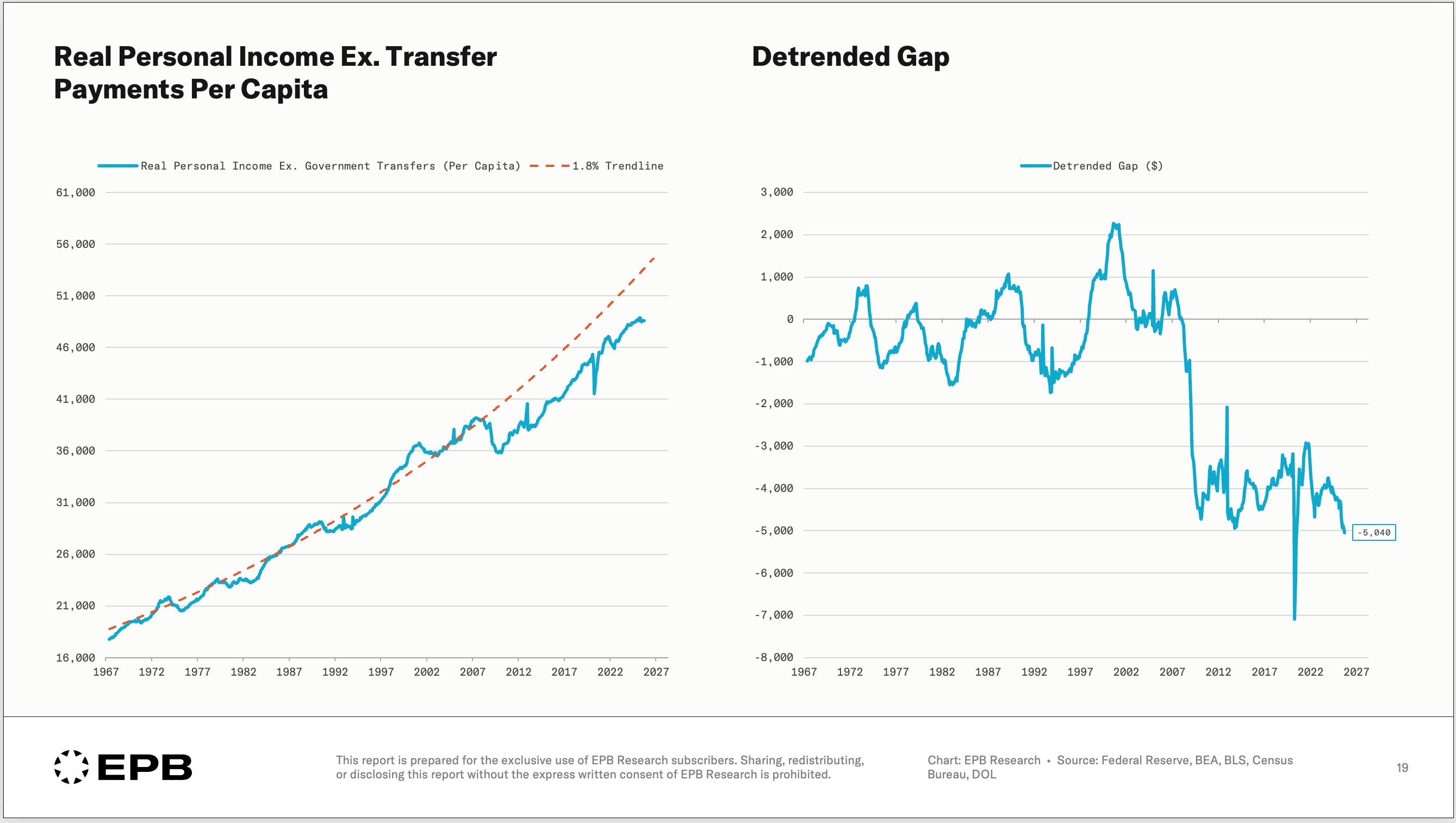

From the 1960s through 2007, real income increased at a 1.8% pace. After the 2008 recession, real income dropped and never regained the 1.8% trend line as it did after all recessionary periods in the prior four decades.

Had real income growth remained on the 1.8% trendline, the US economy would be generating closer to $53,500 per capita, $5,000 more per capita, or $20,000 more for a family of four.

For many decades, people grew to expect a certain level of real income growth or a certain pace of improvement in their standard of living.

Just as with financial investments in the stock market, small changes in the rate of compounding are hard to see year to year but can grow enormously over many decades.

Shifting the growth rate in real income from 1.8% to 1.3% can’t be felt over one year. But over 18 years, the average person is almost 10% worse off than they would have been had we stayed on the same trend.

What would the average family of four be able to do with an extra $20,000 per year? Reduce debt, pay for child care, increase savings? Or, looked at in reverse, this $20,000 gap is what many families expected in 2005 or 2006 as they projected future income, and this shortfall has been plugged with debt.

It should be clear why most people feel they are not keeping up or their standard of living is not improving as fast as they expected, because for the average person, it’s not. This becomes even worse when looking at the bottom percentage of the income spectrum, since the averages are actually improved by the very wealthy. But why is it happening?

We know that real income is tied to productivity and that real income growth has shifted down. Even a decline from a 1.8% trend to a 1.3% trend has created problems that have grown very large over the last two decades.

This problem has its roots in a lack of investment.

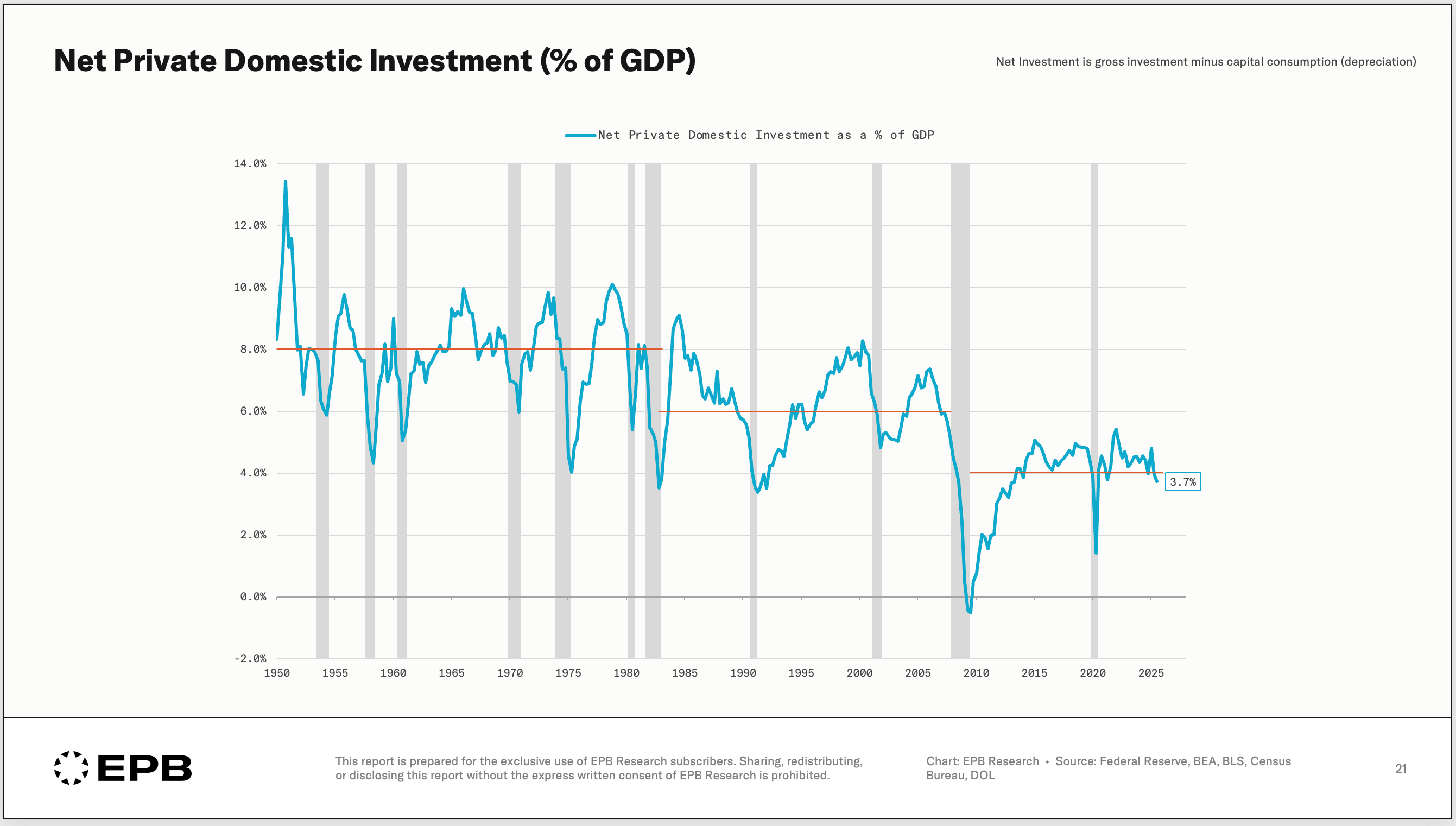

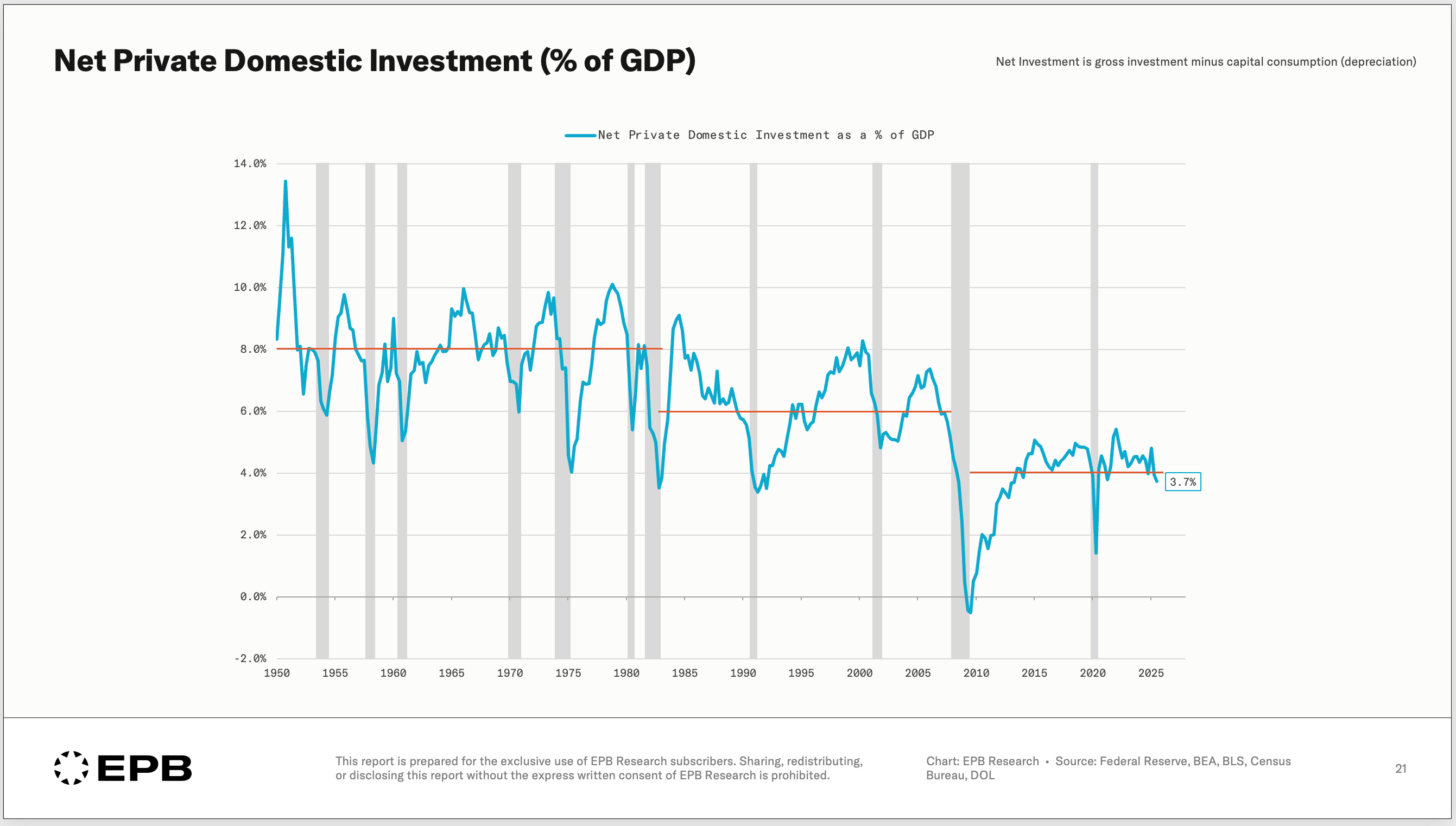

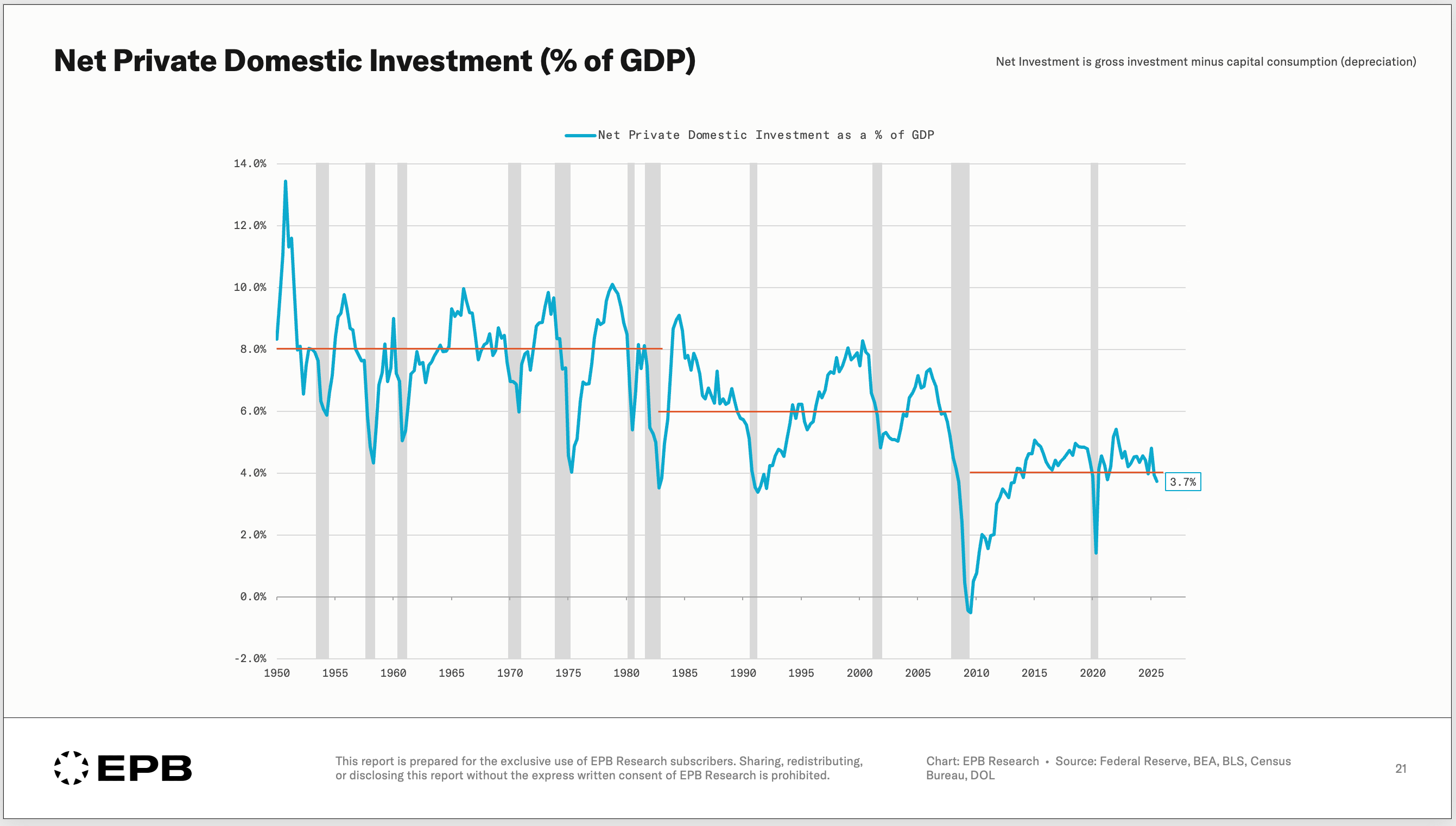

Net private investment measures how much the private sector is investing in structures, equipment, and intellectual property after accounting for depreciation. The economy has to spend a certain amount of money just to stand still because roads, machinery, and buildings get worn out over time, and money needs to be spent simply to offset this erosion.

Net investment measures how much the economy is investing in new structures and equipment after accounting for this wear and tear.

From 1950 to 1980, we invested about 8% of GDP. From 1980 to 2007, we invested about 6% of GDP, and from 2009 to 2025, about 4% of GDP.

If we maintained just a 6% net investment rate, that would be the equivalent of $600 billion of new investment each year - investment that we are not making today.

But why?

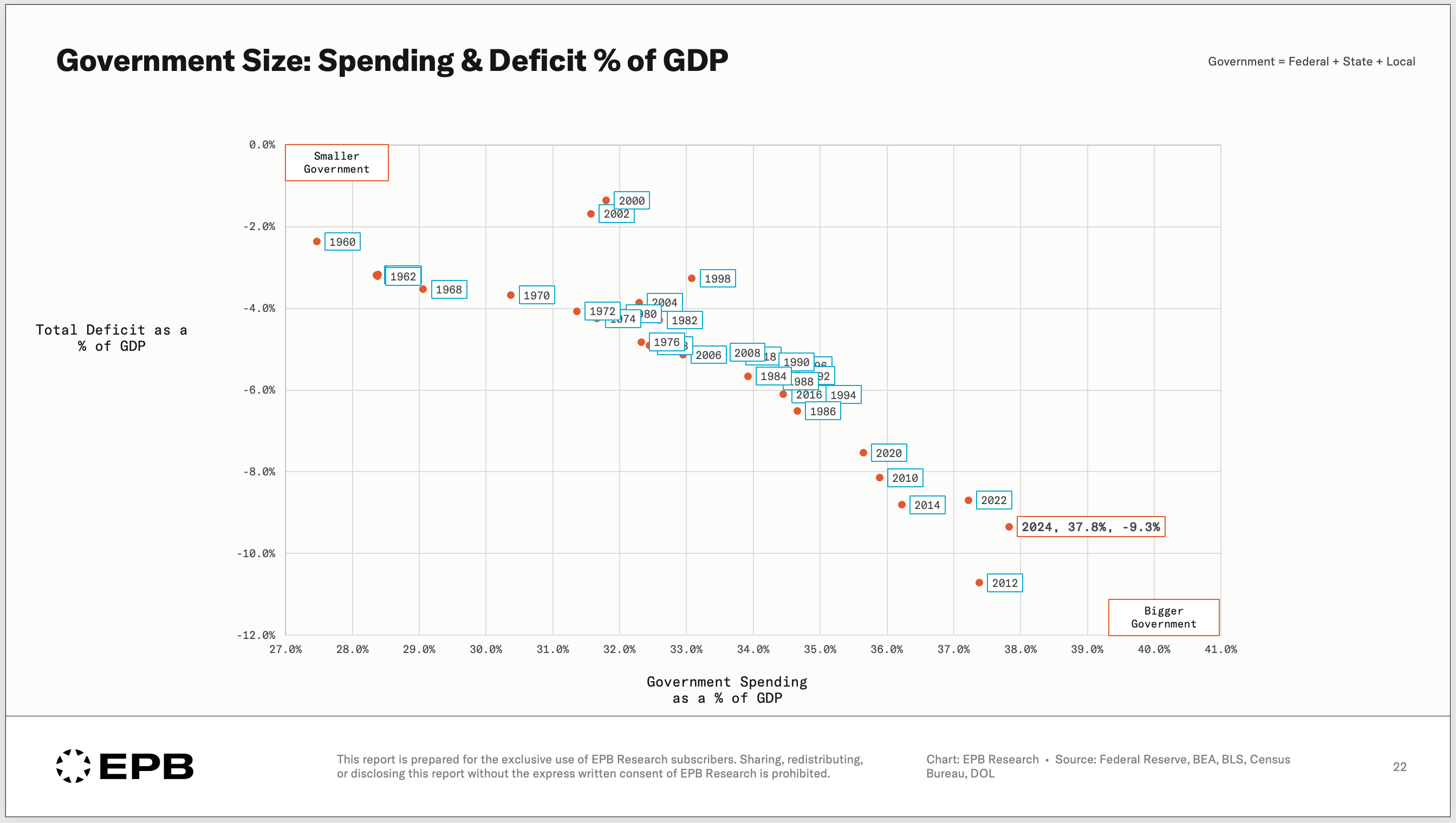

There are several reasons for this decline in investment, but they mainly stem from an increase in government size.

Government Size & Net Private Investment

There are certain mathematical identities that describe the economy, and one critical formula is the National Savings & Investment Identity.

The National Savings & Investment Identity explains the relationships among private-sector savings, private-sector investment, government budget deficits, and the trade deficit, with the opposite of the trade deficit being foreign capital inflows.

Domestic saving plus foreign saving must equal private investment plus government borrowing.

This can be written as:

Budget Deficit = Private Savings - Private Investment + Trade Deficit

In other words, if the US budget deficit increases, private savings must increase, private investment must fall, or the trade deficit must widen (or some combination of the three).

Since the US budget deficit has increased faster than the trade deficit, it’s been necessary for private savings to increase or private investment to fall.

Private saving is the opposite of private consumption, and in the United States, we are not keen on reducing consumption, so the burden has led to a decline in private investment.

Beyond the mathematical identity that has caused a decline in net private investment due to larger government budget deficits, there are also shifting incentives arising from a larger government spending firehose.

When government spending and deficits rise as a share of GDP, private investors face increasing uncertainty about future taxes, regulations, and the rules of the game. Long-term capital projects like factories, machinery, and infrastructure require committing resources today for returns that materialize over decades, exposing investors to years of unpredictable policy risk.

Rational actors respond by shortening investment horizons, maximizing liquidity, and favoring financial engineering over real engineering.

Talent flows toward rent-seeking behavior and navigating government rather than building productive capacity.

The result is a secular decline in net investment, a slower-growing capital stock, and compounding productivity erosion.

Fixing The Problem: Is It Even Possible?

Of course, the growing government size and budget deficits are not the only reasons the rate of net investment has declined in the United States, but they are certainly the largest factors.

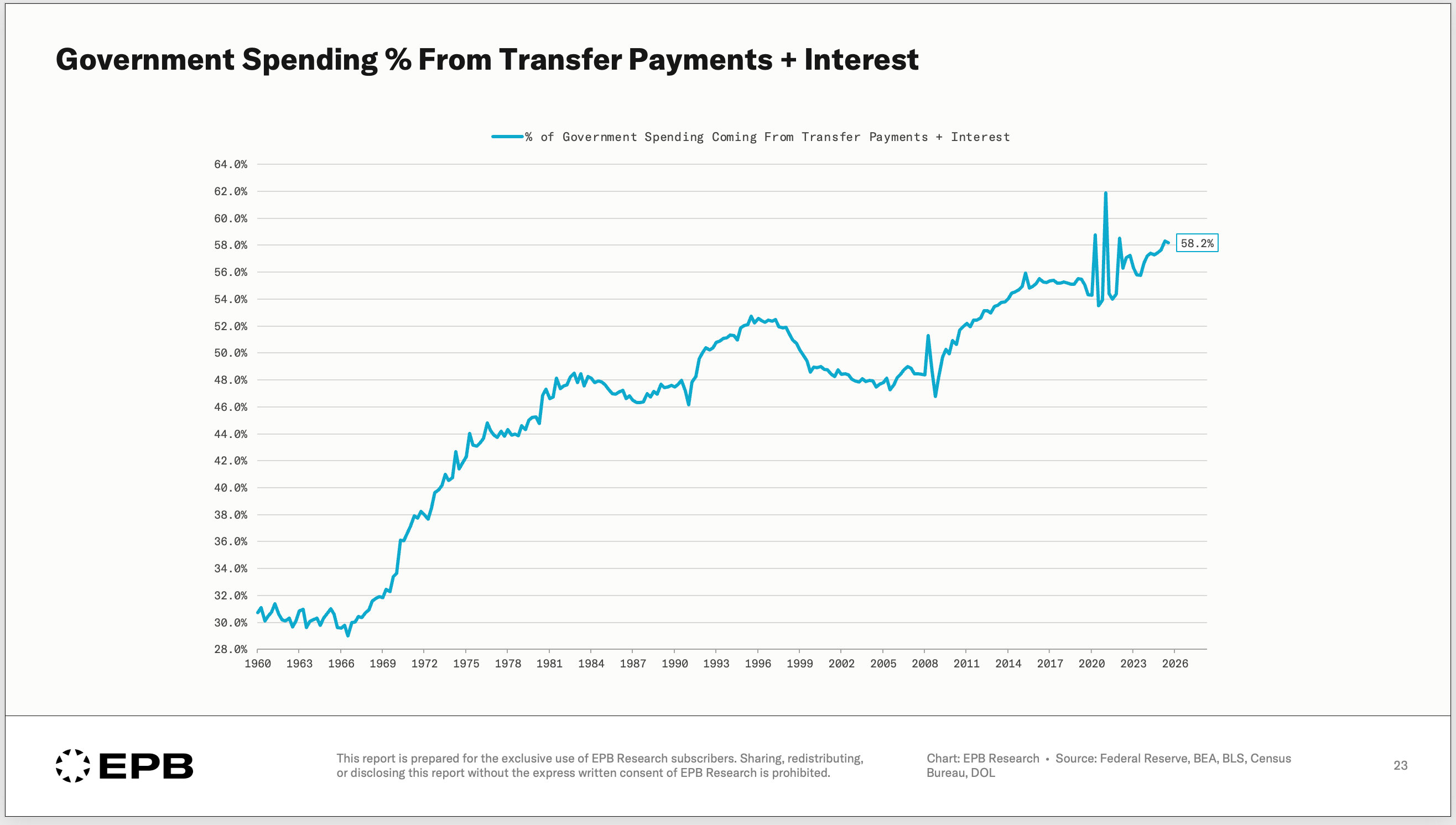

Fixing the problem is extremely difficult if we agree that the deficit is the largest driver, because the United States is structurally locked into higher spending through Social Security, Medicare, and Medicaid, which make up the bulk of what are called transfer payments.

Transfer payments and interest are now 58% of all government spending, which is more than $11 trillion when factoring in federal, state, and local governments.

If reducing spending is not politically feasible, increasing taxes can close the budget deficit, but that is an equally unpopular political platform.

If we assume government budget deficits will grow in the future, then the trade deficit must increase to maintain our current rates of consumption and domestic investment.

Tariff policy is designed to close the trade deficit, which is why this is a dangerous path if reducing the budget deficit is not a simultaneous plan.

Even still, it’s unlikely the trade deficit can grow at the same speed as the budget deficits are growing, even if we wanted to. So the mathematical result is lower consumption or lower investment, or some combination of the two.

A continued decline in the rate of net investment is almost assured.

Where We Are Going & What You Can Do About It

As the rate of net investment continues to stair-step lower as it has over the last several decades, productivity growth will falter.

A lower and lower rate of net investment over time means worse and less reliable roads, airports, power grids, machinery, train stations, power plants, and factories.

Decaying infrastructure leads to lower productivity outcomes, which in turn lead to lower rates of real income growth.

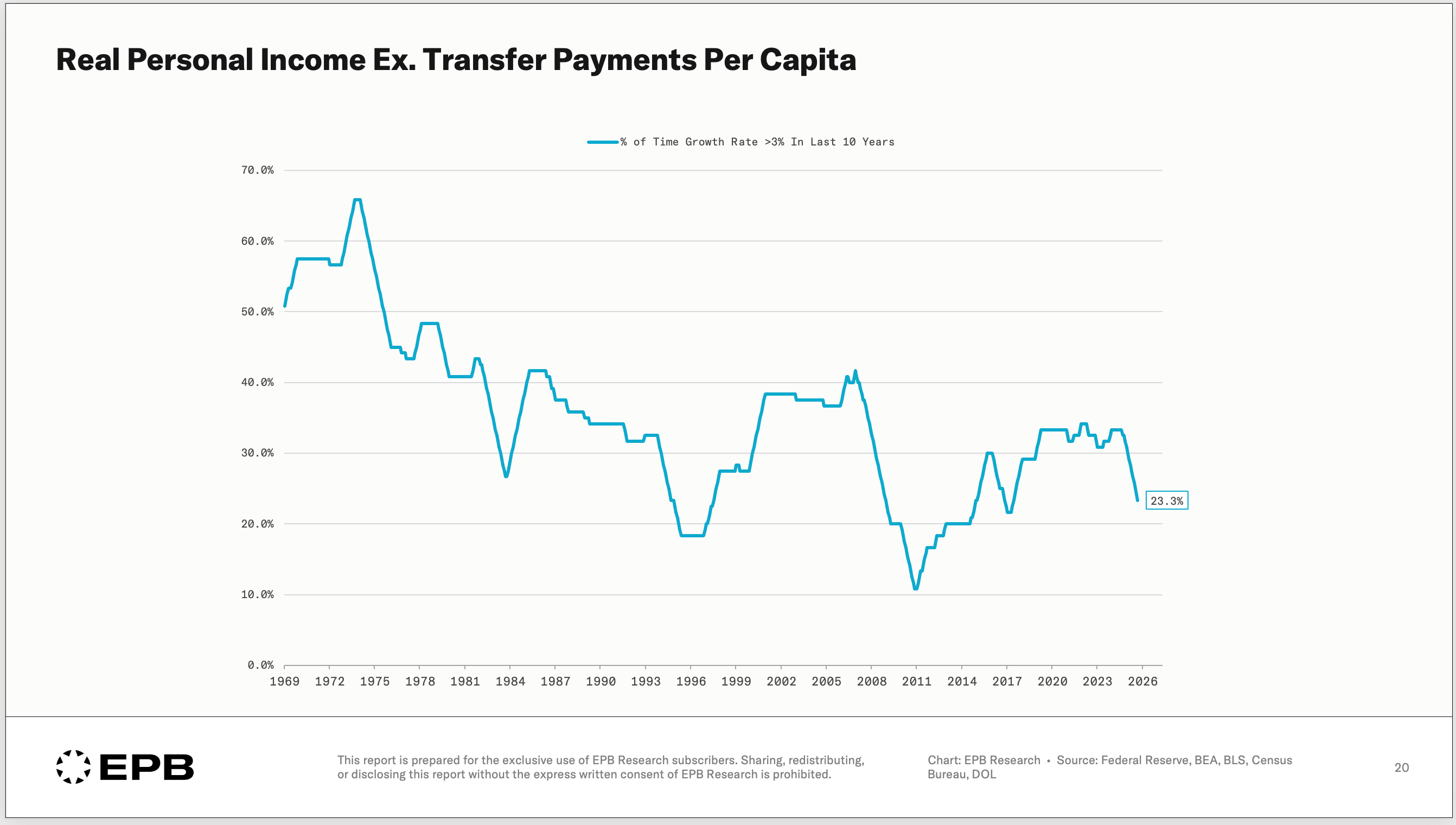

This chart shows the percentage of time real income growth exceeded 3% over rolling 10-year periods.

So in the early 1970s, real income growth exceeded 3% more than 60% of the time. Today, real income growth has exceeded 3% just 23% of the time in the last 10 years.

This will continue to slide, reducing the average person's sense of prosperity and leaving out the people at the bottom of the income structure.

Savings equals investment, and the core issue is that the US doesn’t save.

Savings is essential, and one thing you can do is zig while everyone is zagging. Increasing your personal savings rate is likely the best antidote to a society with a savings deficiency.

Wealth and power will accumulate to the companies that are capital-light and monopoly-like in pricing power, which is why these well-known companies have been and likely will continue to be strong investments. But importantly, these gains have been built on an increasingly unstable foundation that will continue to erode if we remain on this same path, which many find unavoidable.

Thanks Eric. Although this is shocking and scary, everyone, especially political and business leaders need to read this. I hope this article is read by people everywhere so that we can understand the enormity of this problem.

Excellent piece.