The Iran War Just Derailed the Housing Recovery

Housing was stabilizing for the first time in three years. Then the war reignited inflation and pushed mortgage rates higher, threatening the brewing recovery in the economy's most important sector.

Housing, or residential investment more specifically, is unquestionably the most important and leading sector of the economy.

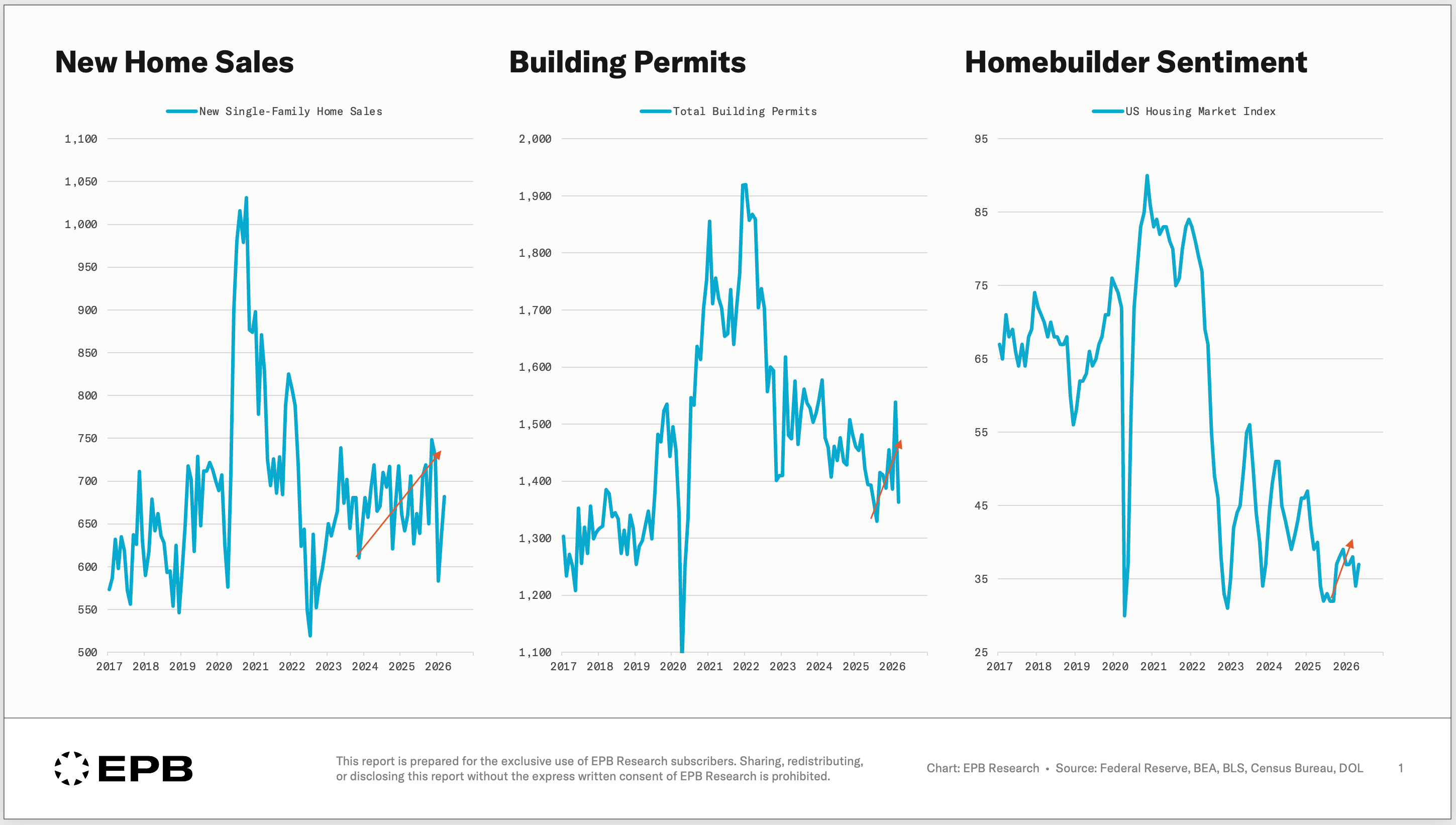

Two months ago, the housing market was showing fragile signs of stabilization. New home sales had recovered from the August 2025 lows, building permits had bounced off the cycle bottom, and homebuilder sentiment was beginning to stabilize. The most interest-rate-sensitive indicators in the economy were starting to suggest the worst of the housing downturn might be behind us.

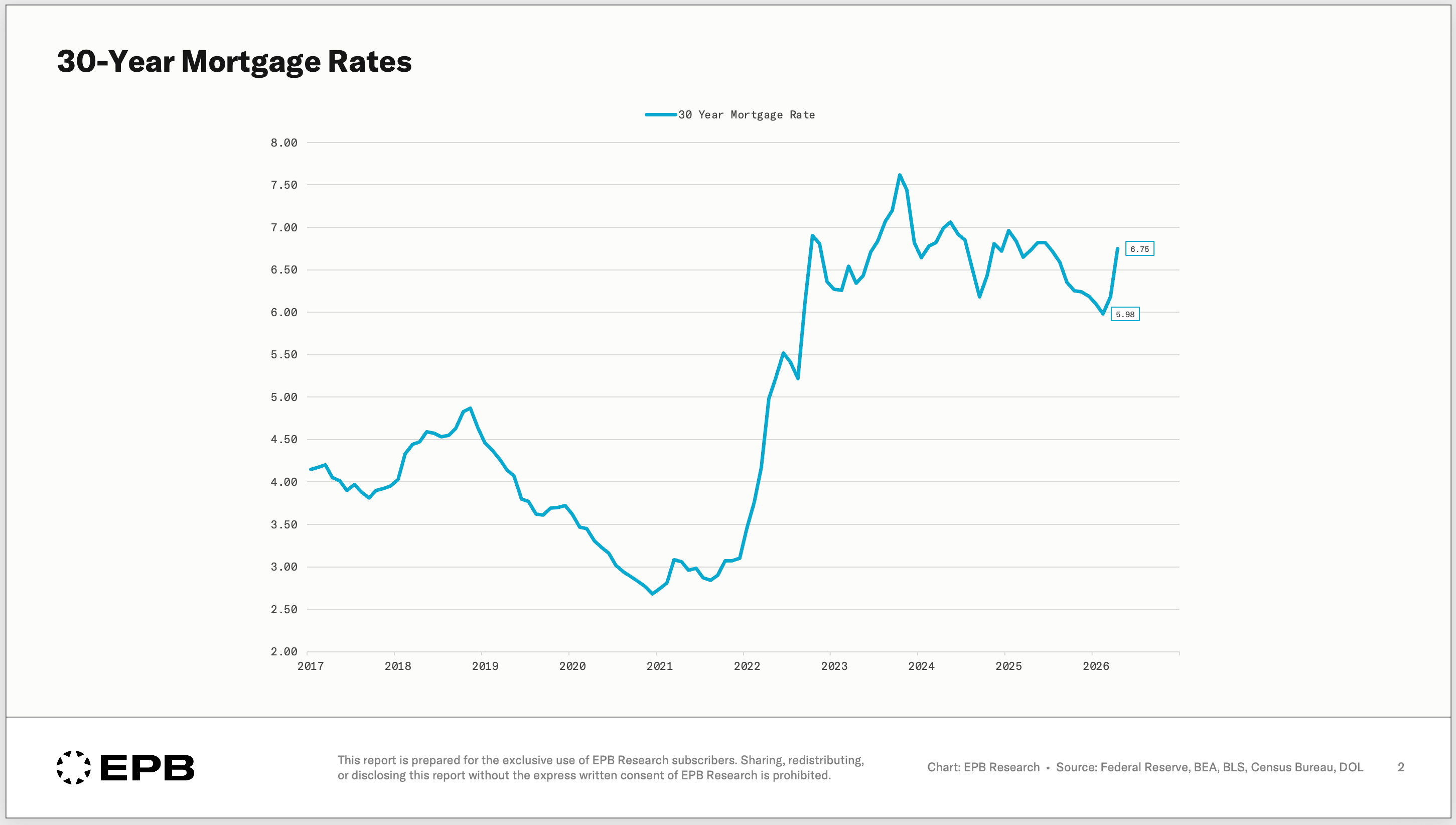

However, that stabilization was based on one key assumption: that monetary policy would continue to move towards lower interest rates. Before the Iran War started, there were 2-3 interest rate cuts priced in, and mortgage rates were starting to fall into the 5% range.

Then the spike in oil prices and the fear of more widespread shortages reignited inflation concerns. Mortgage rates moved back to the mid-6% range as markets are now pricing zero rate cuts.

The fragile stabilization emerging in the leading housing indicators is now at serious risk of reversal. A continued slowdown in housing construction comes at a very bad time, as new completed inventory is piling up and homebuilders face an ever harsher squeeze in profit margins.

In this post, we’ll review the sequence of the housing cycle, where it stands today, and how the surge in interest rates disrupted what was an emerging recovery in residential construction.

The Housing Sequence

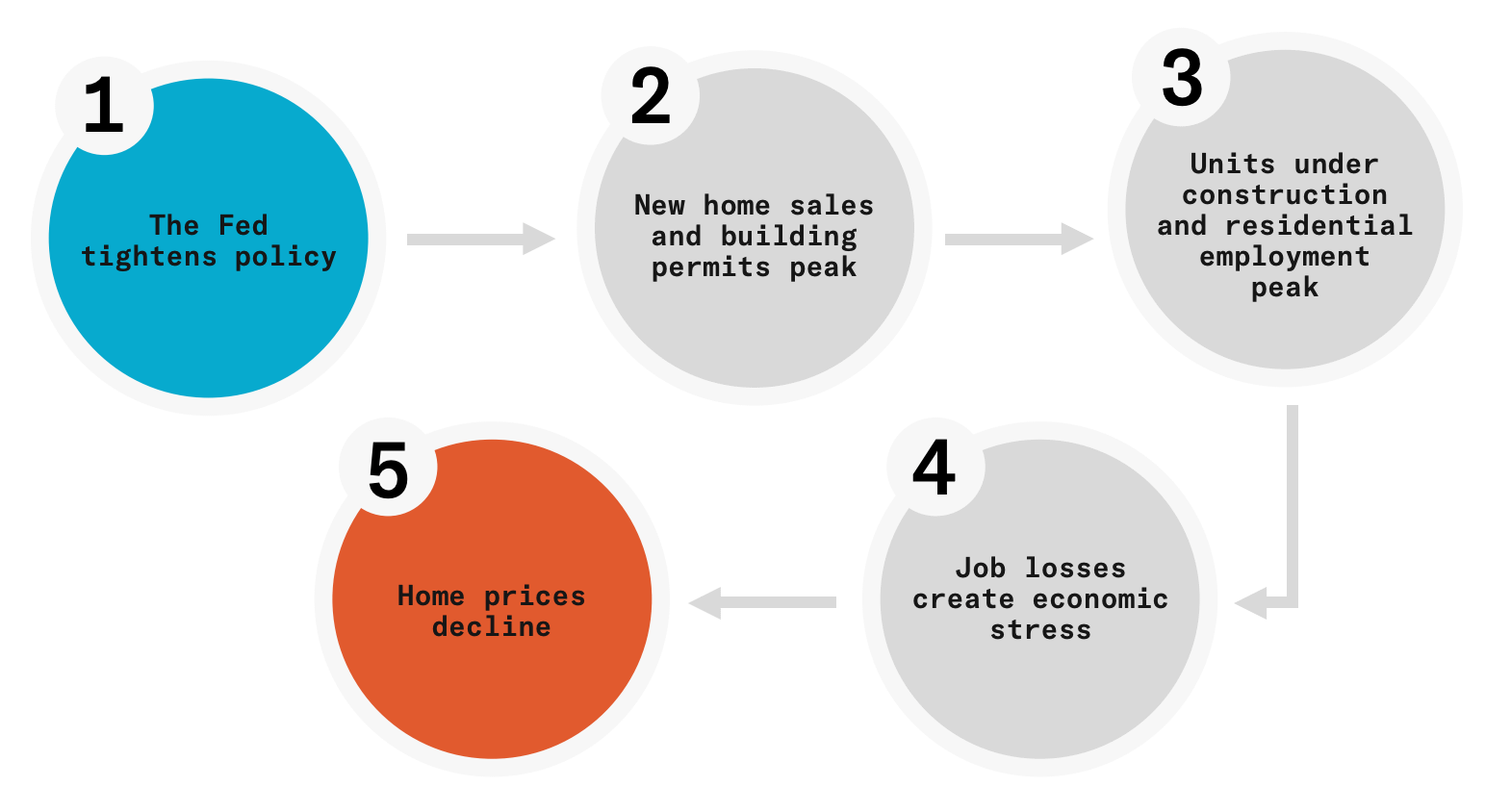

Housing follows a repeatable sequence. Every cycle follows the same pattern. New home sales peak first, and building permits follow. Then the number of housing units under construction declines, and as a result, residential construction employment drops. Home prices are the last domino, often moving 18-36 months after the sequence began.

The full sequence, including infographics and the 2008 case study, is mapped in our Free Residential Construction Cycle Guide, available for download at https://www.epbresearch.com/housing.

The Leading Layer

Mortgage rates are the input variable for the entire housing sequence. The expected path of interest rates shifted from one suggesting mortgage rates in the 5% range by year-end to one holding in the mid-6% range, with no relief in sight. That is a massive change in the early part of the housing sequence and another rug pull in a series of head fakes for the housing cycle recovery.

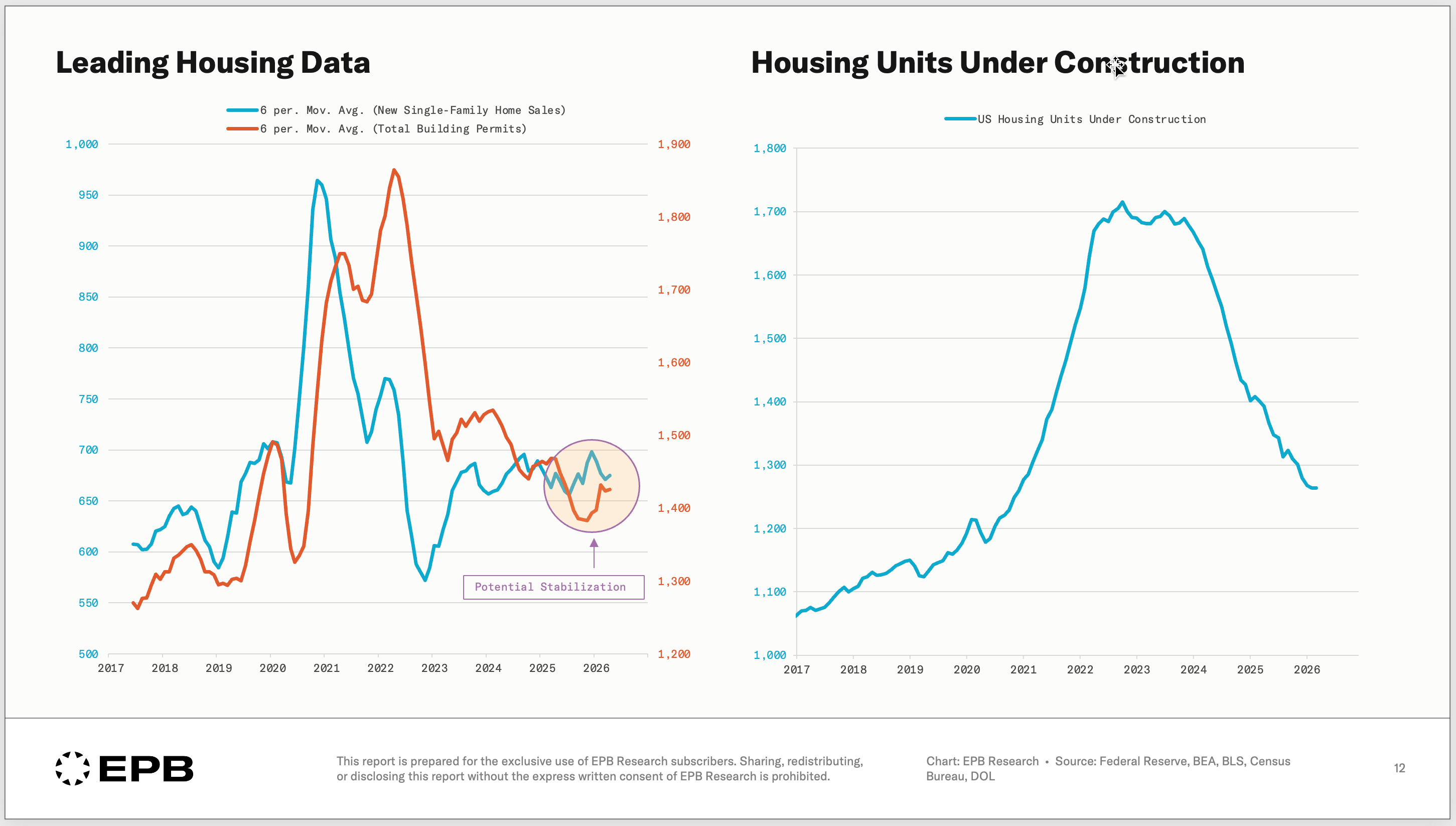

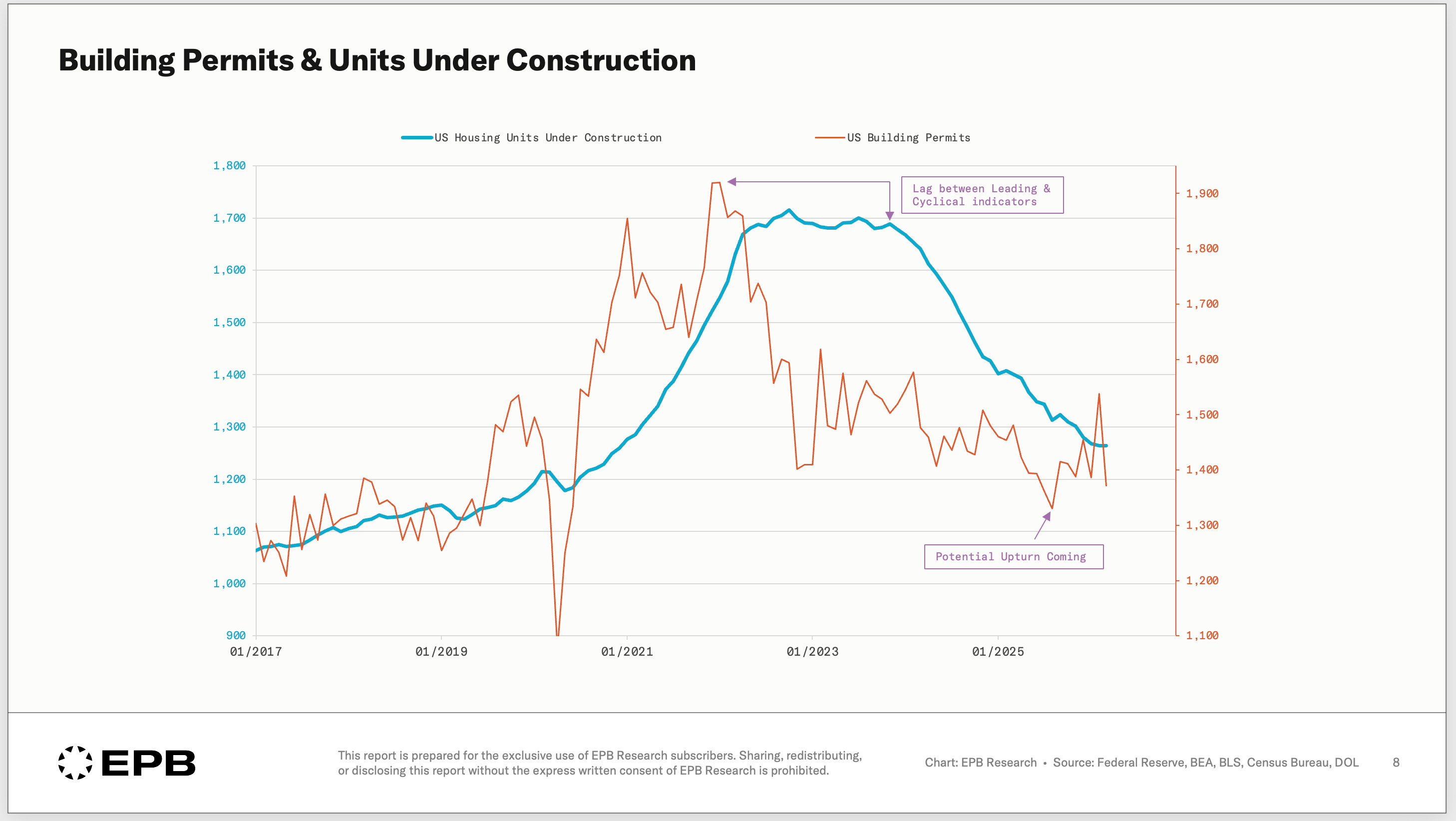

Building permits and new home sales were responding to the prior easier path. Permits bottomed at 1.3 million in August 2025 and recovered to 1.45 million by December. New home sales went from averaging low 600,000 units to 764,000 in November. The data was starting to suggest the leading indicators had found a floor. The strength of the acceleration was in question, but the worst was over.

Homebuilder sentiment had stabilized over the same window, holding above the readings registered in the fall of 2025.

When all three variables move or stabilize together right after a big shift in monetary policy inputs, like mortgage rates, it is the type of cluster behavior our framework looks for. The cluster was stabilizing and turning up.

The Cyclical Layer

While the leading layer was showing tentative recovery, the cyclical layer never participated.

The number of housing units under construction continued to decline through the entire stabilization window. This is normal because there is a lag between the most leading variables and the actual construction activity. Given the stabilization we had started to see, there was optimism that a bottom in housing construction was coming soon.

The problem with this now-disrupted stabilization is that the cyclical variables never stopped declining. So if the leading variables turn lower again due to higher interest rates and inflation fears, the downturn in actual construction activity will not let up.

This also comes at a bad time for homebuilders because their inventory situation is much less healthy.

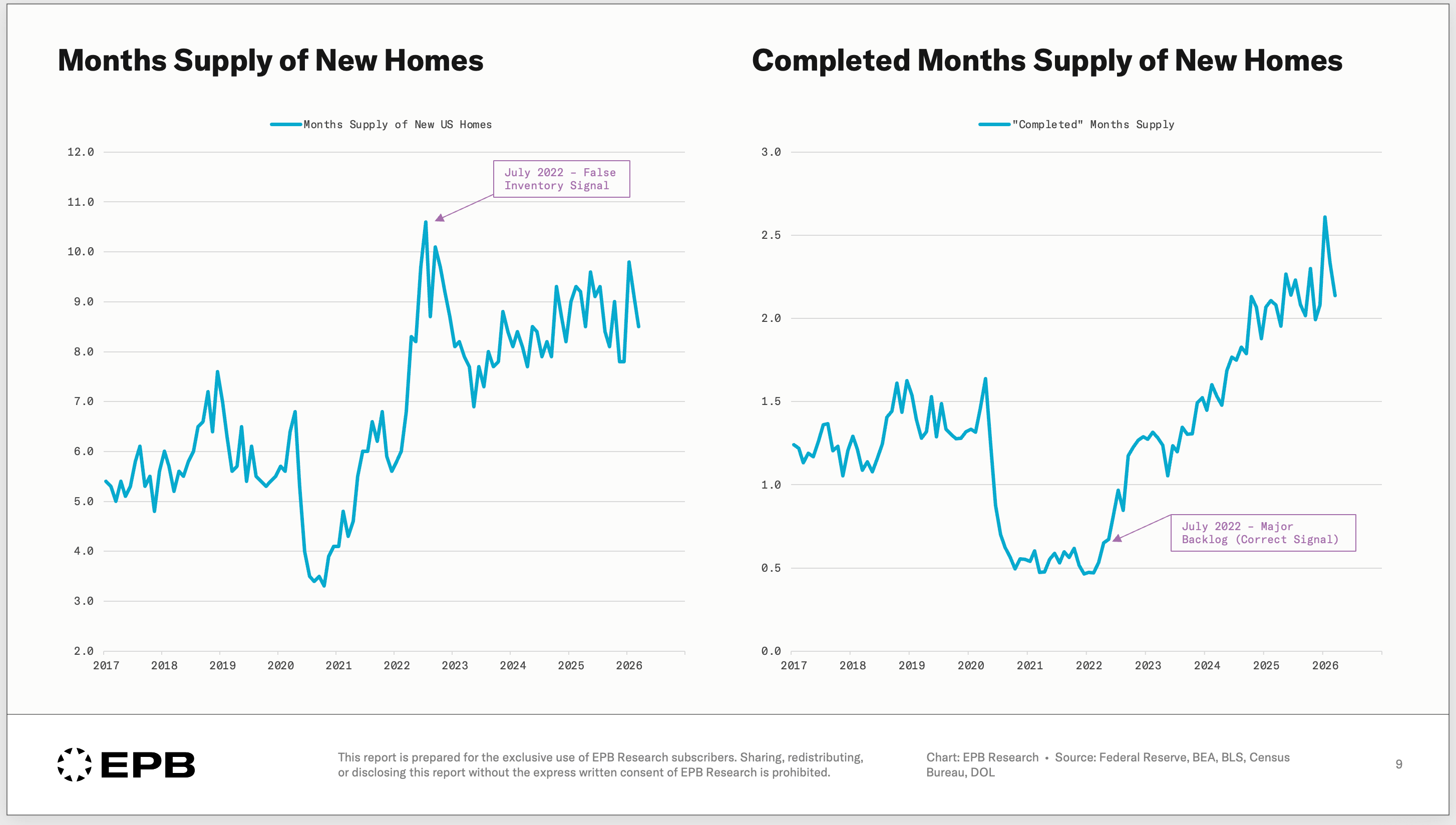

As we covered in a previous article, it’s not just the level of inventory that matters for builders, but more importantly, it's the level of completed inventory that has the biggest impact on profit margins.

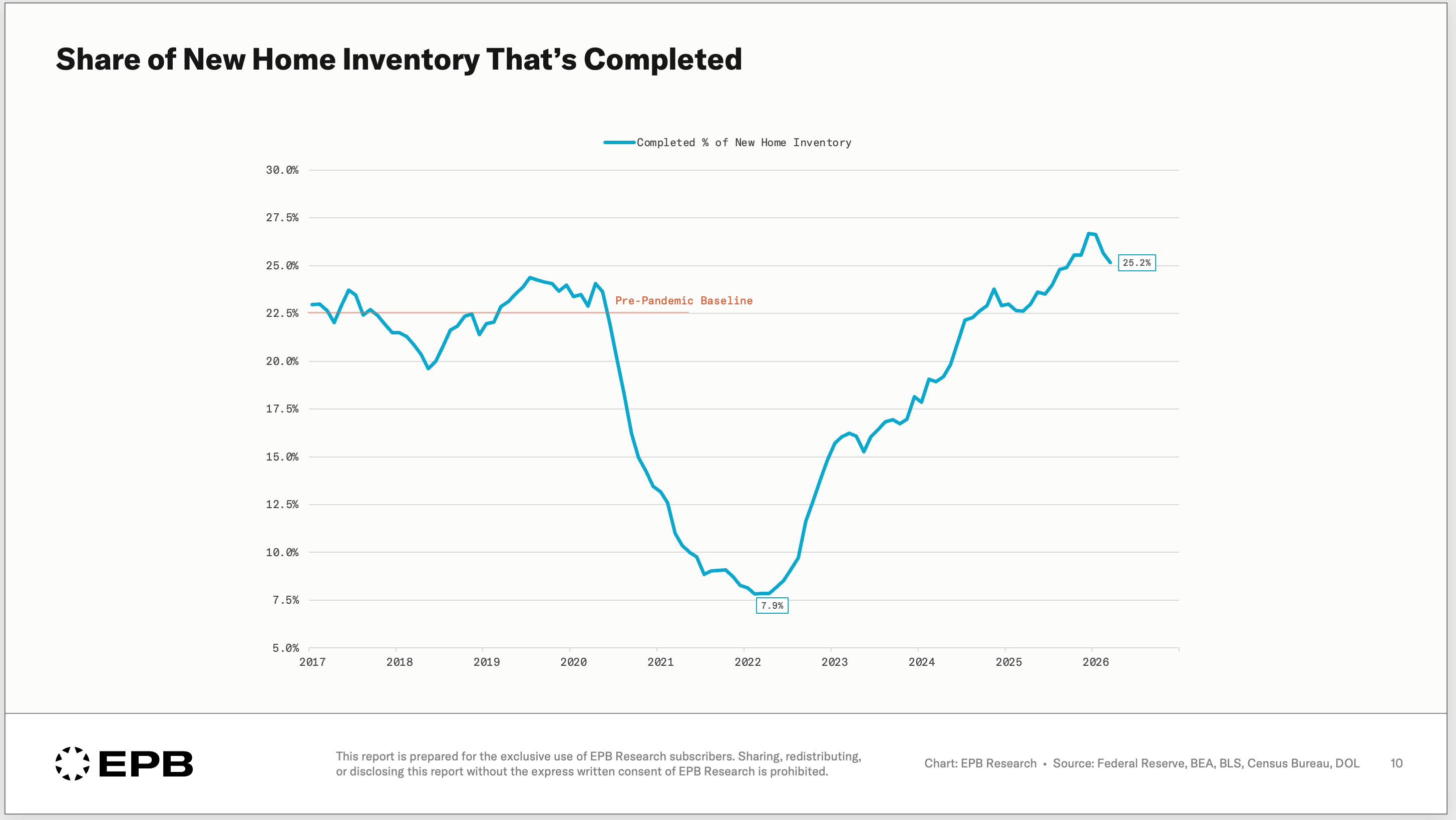

The share of new homes for sale that are completed sits above 25% and is moving closer to 30%.

In 2022, when months supply last spiked above 10, only 8% of that inventory was completed, so there was a huge backlog of construction despite looking like an inventory glut on the surface. Today, that inventory situation is worse despite a lower months supply.

This difference is the entire ballgame for builder profit margins.

In 2022, builders could slow starts and let the pipeline drain. The homes were not built yet. Over 90% of the listed inventory was not started or was under construction.

There was nothing to discount.

Today, a much larger share of inventory consists of finished homes. Completed homes have more carrying costs with no revenue. Builders have more pressure to move them. That means incentives, discounts, and margin compression.

From Margin Compression to Job Losses

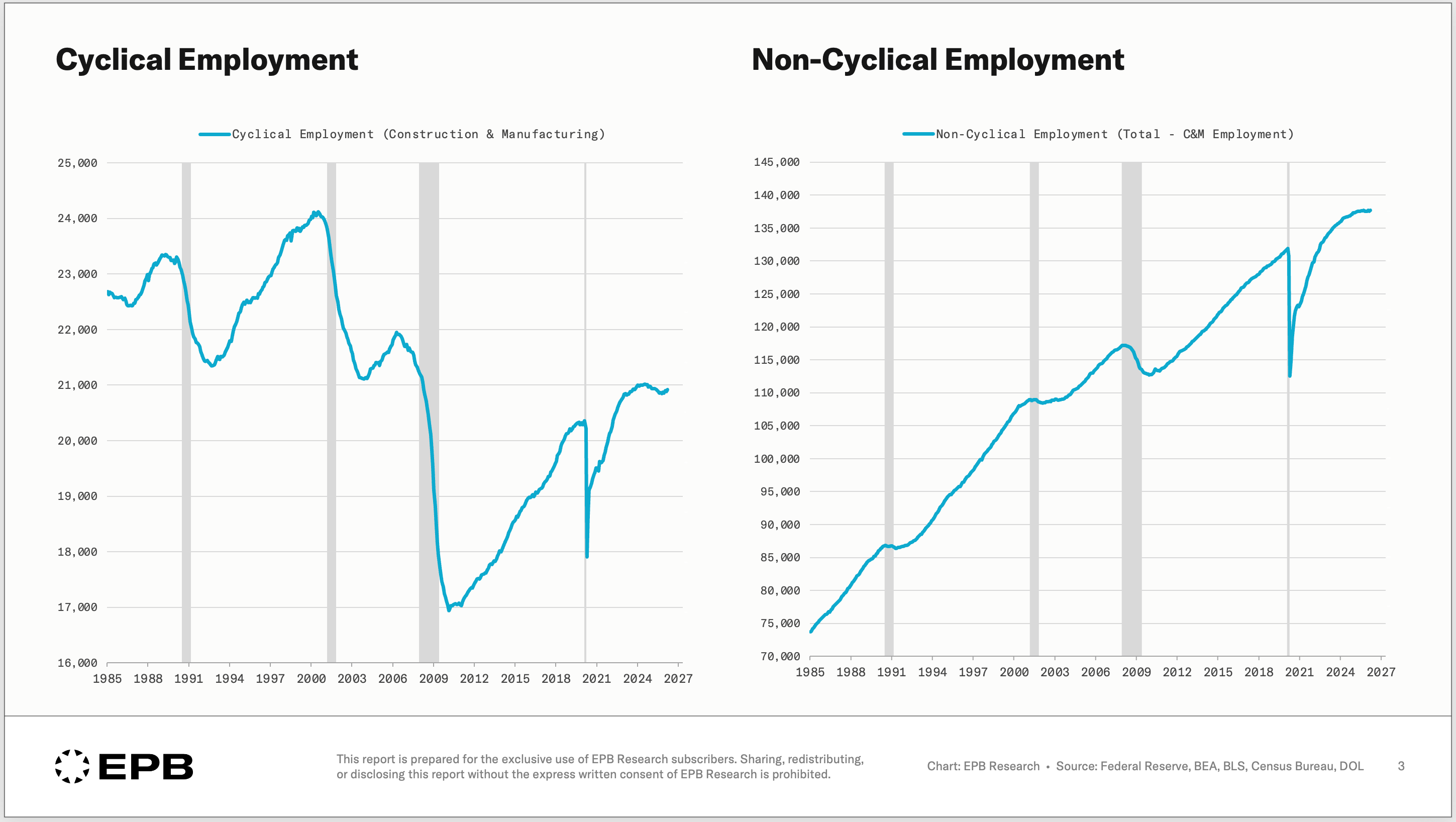

The Cyclical Economy (housing and manufacturing) is where the recession really occurs. Not because construction and manufacturing are large shares of GDP. Because their amplitude is so large that they account for the majority of job losses in every modern recession.

The transmission mechanism from slowing demand to layoffs runs through profit margins. When margins compress, layoffs follow. When layoffs hit, workers stop discretionary spending, credit defaults rise, and only then does services spending start to slow. This is the recessionary sequence, and it must flow through every step. Every domino must fall.

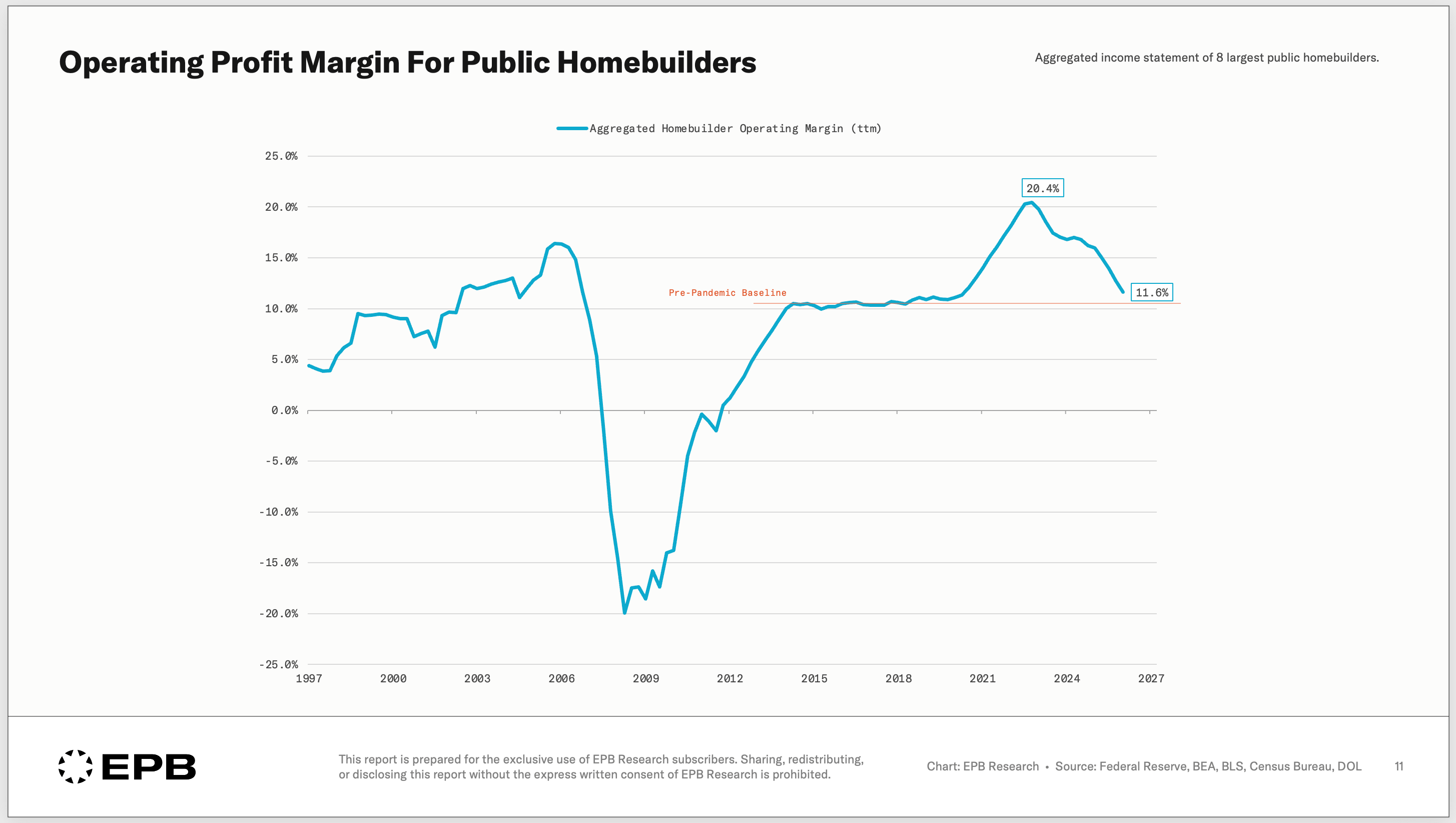

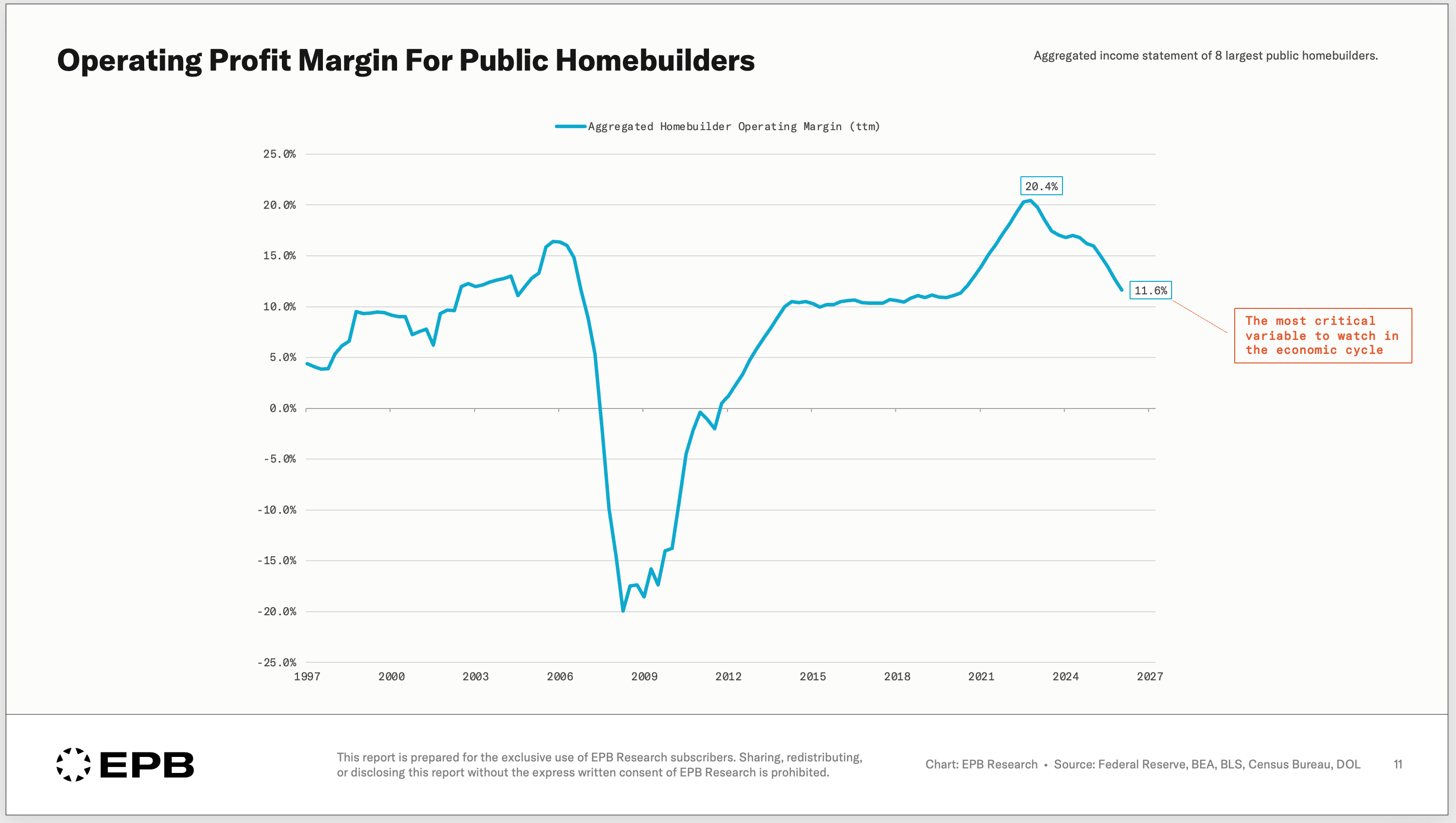

The buffer that has prevented this sequence from completing for three years has been the extraordinarily high level of starting profit margins. Homebuilders entered this period with margins near 20%. That cushion is why units under construction have declined materially without triggering large construction layoffs.

But buffers are finite. A completed inventory share nearing 30%, combined with months supply already elevated and now facing another potential downshift in sales volume, is the combination that compresses margins toward the threshold where layoffs become unavoidable.

Where the Sequence Stands Today

The leading housing indicators have lost the variable that was supporting their stabilization. The cyclical indicators never stopped declining and are now at risk of falling further. Builder profit margins have absorbed three years of cyclical weakness because they started so high, but that buffer is closer to the layoff threshold than at any point in this cycle.

Despite a slowdown in this part of the economy for three years, the housing sequence has not completed. There have not been large residential construction layoffs.

No layoffs in housing and manufacturing, no recession.

But the important framework condition, namely profit margins, that prevented this cycle from completing, is now under even more serious pressure.

This is a huge shift because the housing cycle was starting to stabilize, which would have removed the only vulnerability in the economy.

The AI and technology Capex cycle is keeping many sectors strong, including manufacturing. Housing was the one leg that could cause the economy to fold, and it was stabilizing.

This spike in interest rates puts housing back in a vulnerable position, and it's absolutely the most critical area of the economy to watch.

Since the housing cycle is the most important area of the economy to watch, we put together a Residential Construction Cycle Guide that maps the full five-step housing sequence. It tells you exactly what indicators to follow and in what order.

You can grab the free PDF guide below.

Which Housing Recovery?

The words “Iran war” appeared once in this article (twice if you count the title).

For such a sensationalized title, I’d expect a little more insight into the connection between the war on the other side of the globe and the housing industry here. Not denying their connection, but this was not EPBs best work…