The Housing Recession That Never Came — And The One That's Quietly Underway

In 2022, months supply hit a level not seen since 2008, but a housing recession never came. This metric explains why.

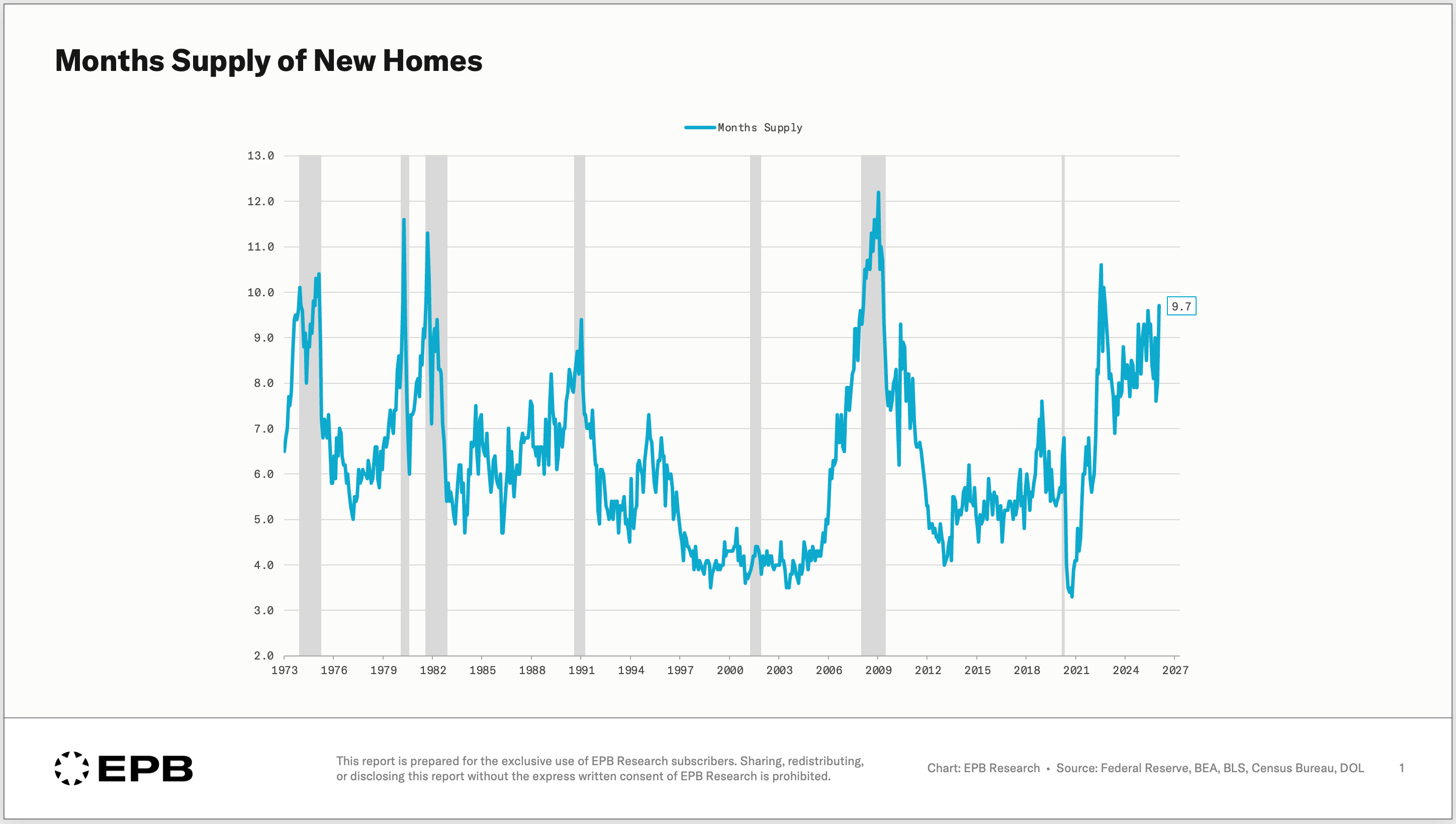

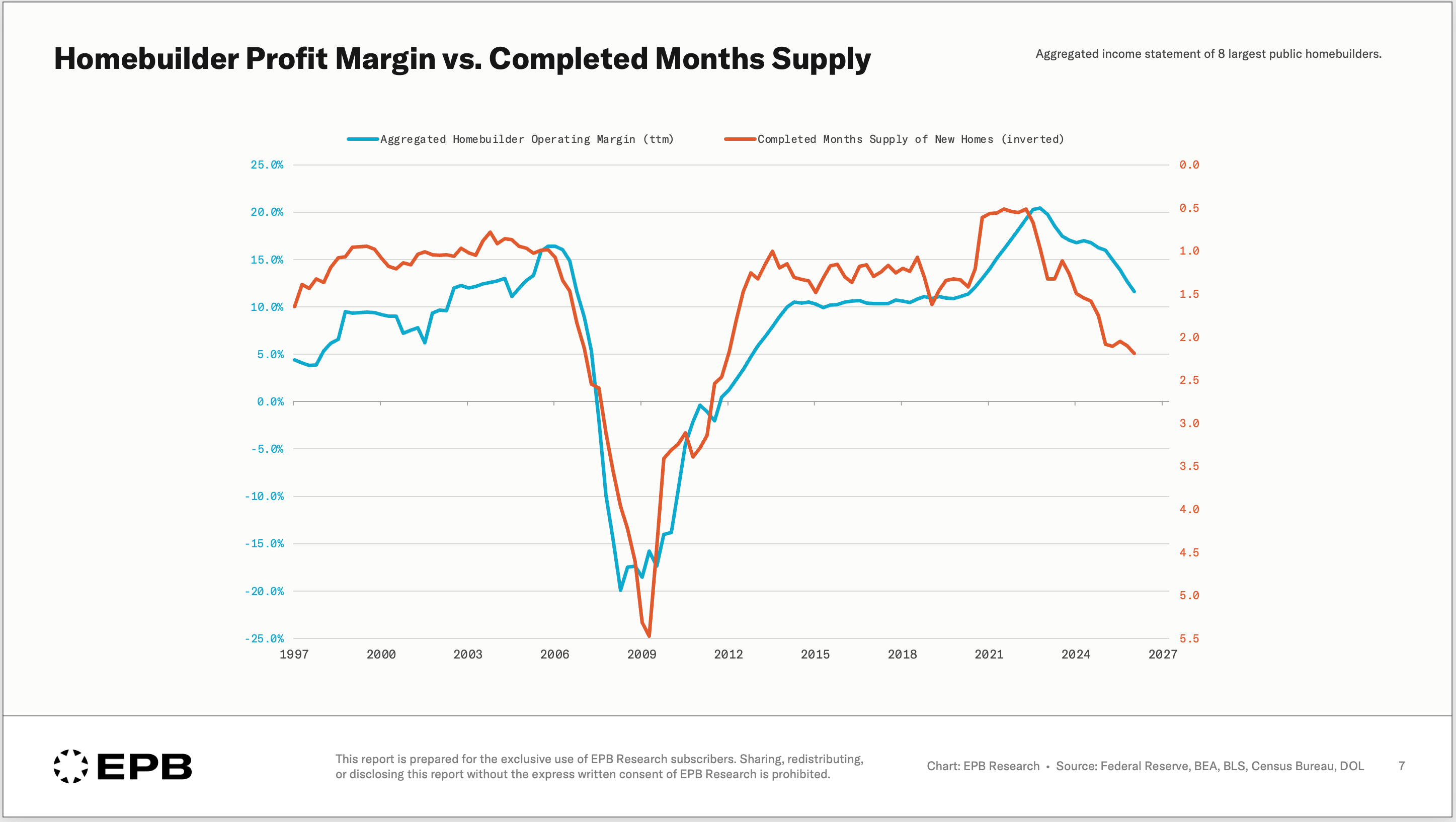

In July 2022, the months supply of new homes hit 10.6 — higher than it reached before the 2008 housing crash.

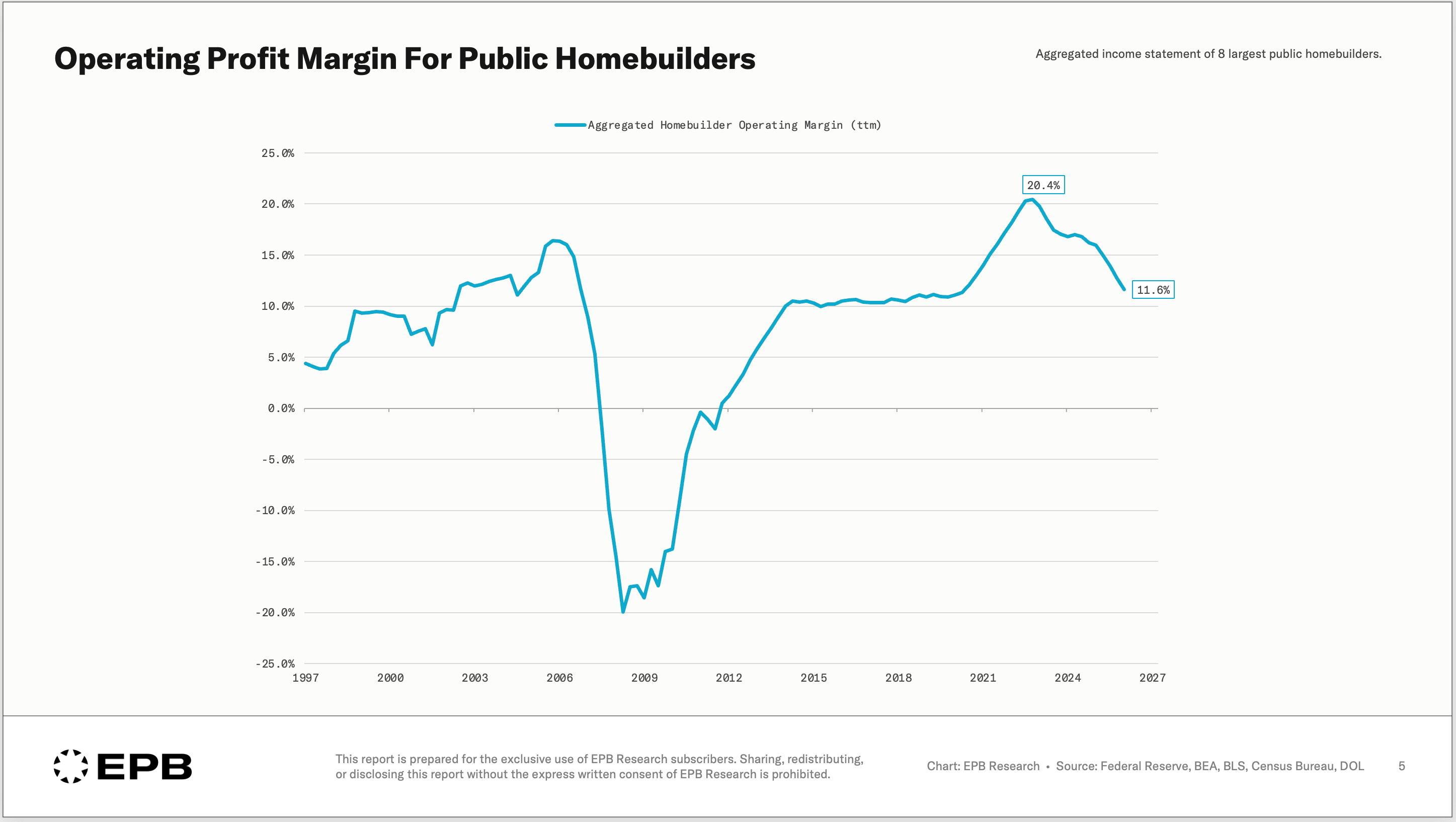

At the exact same moment, the eight largest public homebuilders posted operating margins of 20.4%, the highest level in their recorded history.

High inventory and high profit margins for homebuilders…two things that are not supposed to happen at the same time. In fact, this is the first time in history this occurred, leading to what is now known as the “housing recession that never came.”

In this post, we’ll review the extremely reliable track record of the months supply metric, how it failed in 2022, what we’ve done to correct it, and what the improved metric says about the housing cycle today.

Before diving into the post, I want to make sure you download our free housing cycle guide. It’s a highly detailed PDF that, step by step, walks through the exact sequence of the housing cycle, with updated graphics and visuals to help you properly interpret incoming housing data.

The Track Record of New Housing Months Supply

Months supply of newly constructed homes has been one of the best leading indicators of the residential construction cycle, and thus, the overall business cycle.

When the months supply of new home inventory increased, that signaled an oversupply of inventory relative to sales, a precursor to companies pulling back on new construction, reducing employment, and creating a downturn in associated industries.

A months supply above 7.0 was almost always associated with a recession, and certainly when months supply rose above 8.0.

The 2001 recession was a unique case, and the only recession in the last 60+ years that did not have a housing downturn associated with it.

But in every other case, housing was a primary driver of recessionary conditions, and months supply was the best metric.

However, that measure failed in 2022 as the months supply of new homes exploded to nearly 11.0, but construction continued, job losses didn’t come, and the economy never entered a recession.

Months supply has remained elevated, in historical recession territory since 2022.

Why has this measure failed?

Why Months Supply Failed In 2022

New homes can be listed as “inventory” when a housing unit is:

Not started

Under construction

Completed

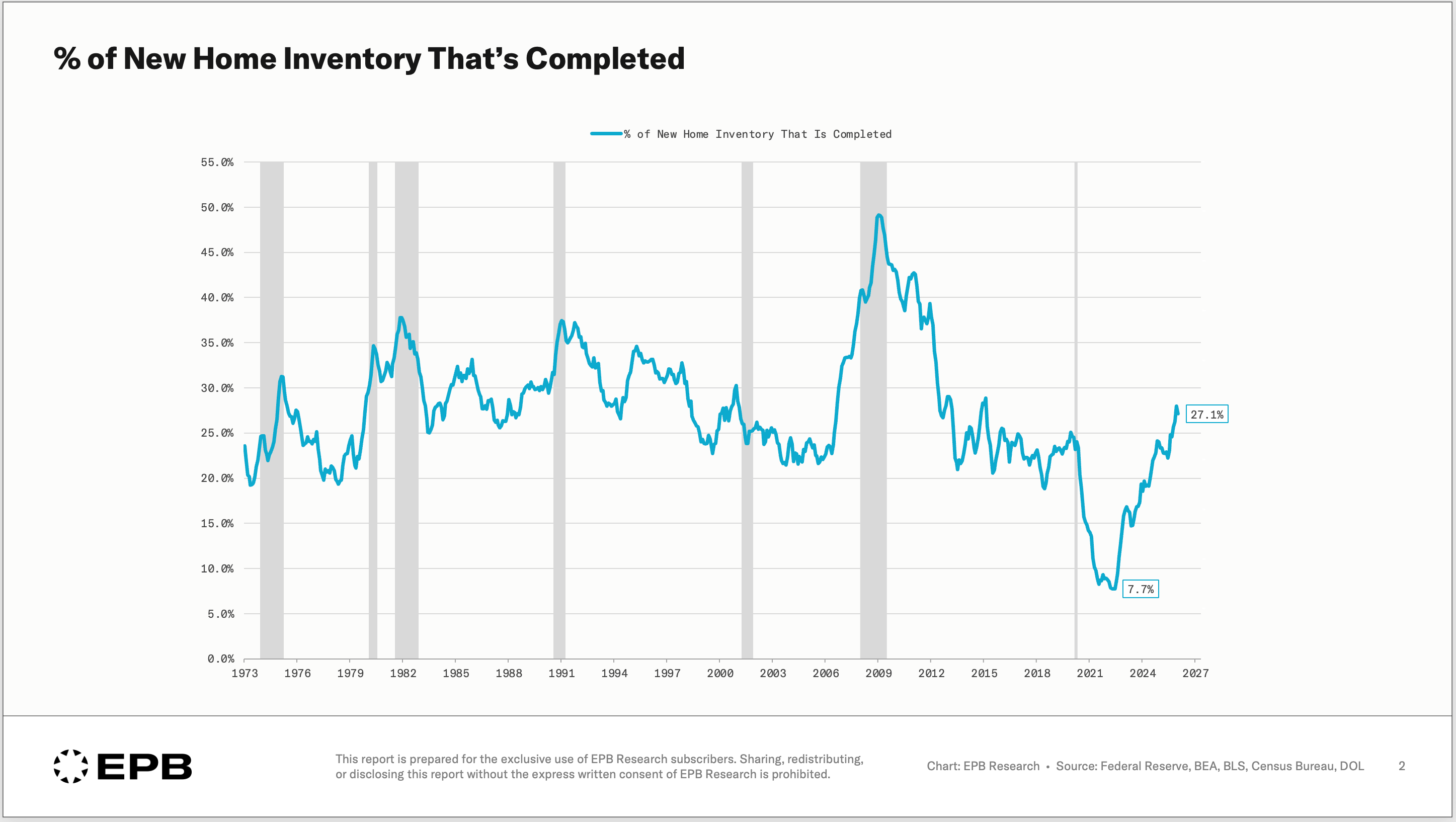

In 2022, when months supply surged above 10.0, almost none of that inventory was completed.

In fact, in 2022, the percentage of new home inventory listed as “completed” was below 8%, the lowest level on record.

This meant that 92% of the “inventory” was either “not started” or “under construction.”

A months supply of 10.0 with 50% of that inventory completed is far different than a months supply of 10.0 with 10% of that inventory completed.

Historically, builders carried a relatively stable portion of inventory as completed, around 20% - 30%, but due to the pandemic and supply disruptions, this number fell out of balance to the point where builders were carrying less than 10% of their inventory as completed.

This situation never happened before, thus never requiring an improved metric, but clearly, months supply lacked the detail to be an effective indicator in all environments and completed months supply is better.

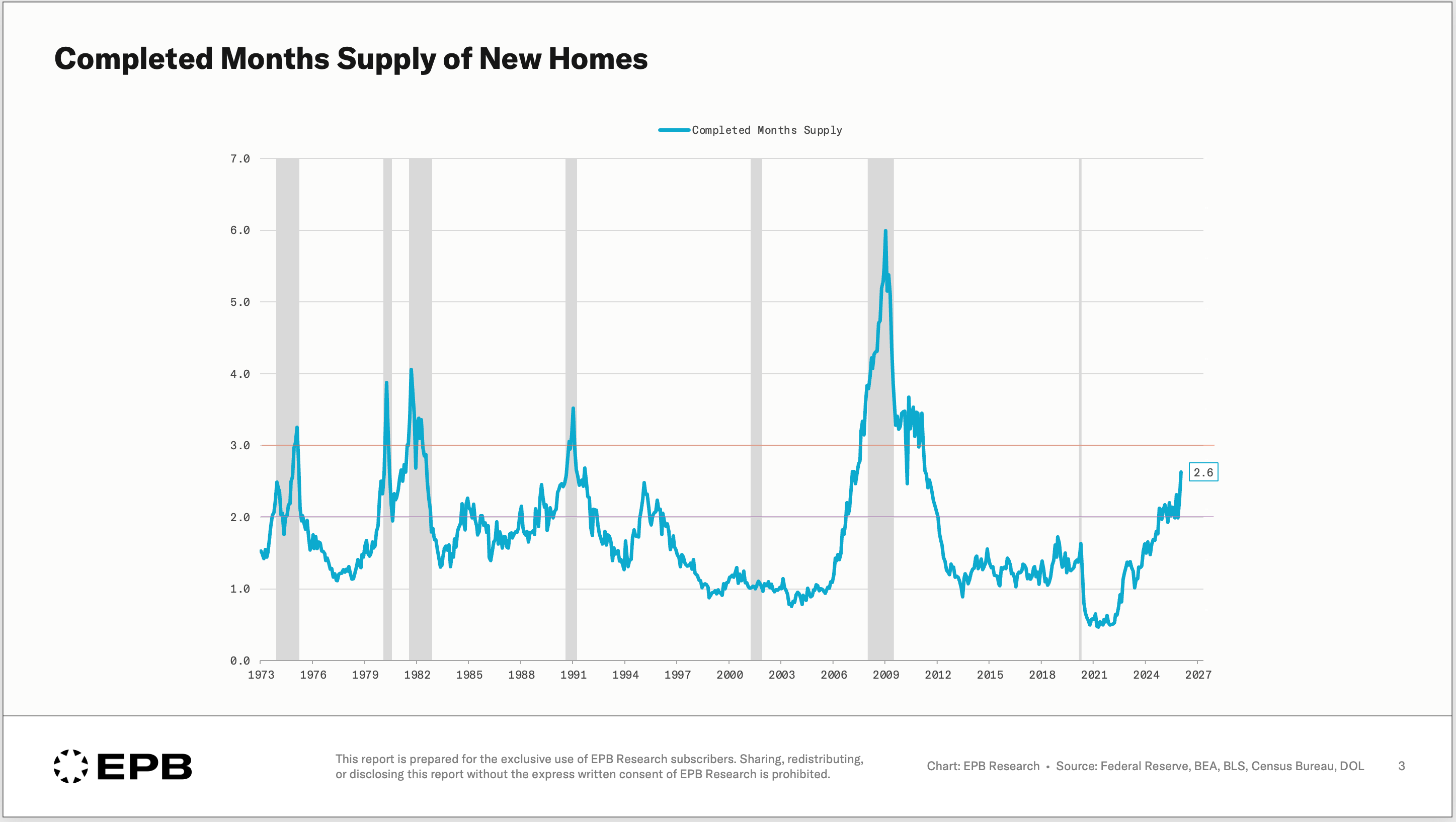

A Better Metric: “Completed Months Supply”

Completed months supply, or the months supply level * the percentage of that inventory marked as “completed” performed just as well as the regular months supply measure in all previous recessions and was not subject to the false signal in 2022.

In fact, completed months supply fell to the lowest level on record in 2022, indicating a huge backlog of construction, despite what may have been declining sales volumes.

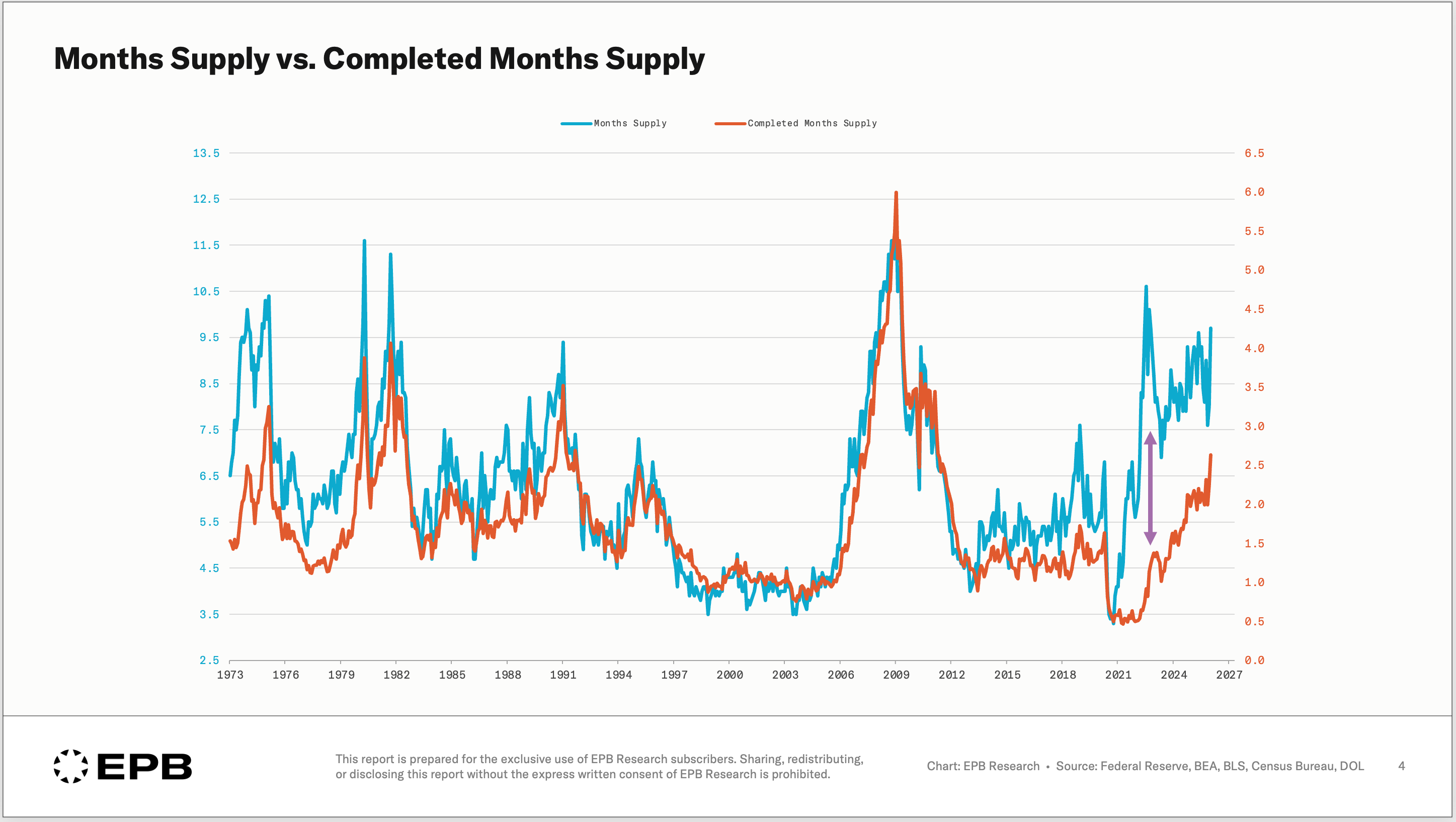

A gap between these two measures was historically non-existent, but when the gap opened in 2022, it was the completed months supply measure that was correct.

Where The Housing Cycle Is Headed

The residential construction cycle is the most important driver of the overall economy. A tightening of monetary policy leads to less affordable housing, a decline in new home sales, a pullback in construction, a fall in employment, and the classic economic stress that manifests from higher unemployment in the early industries.

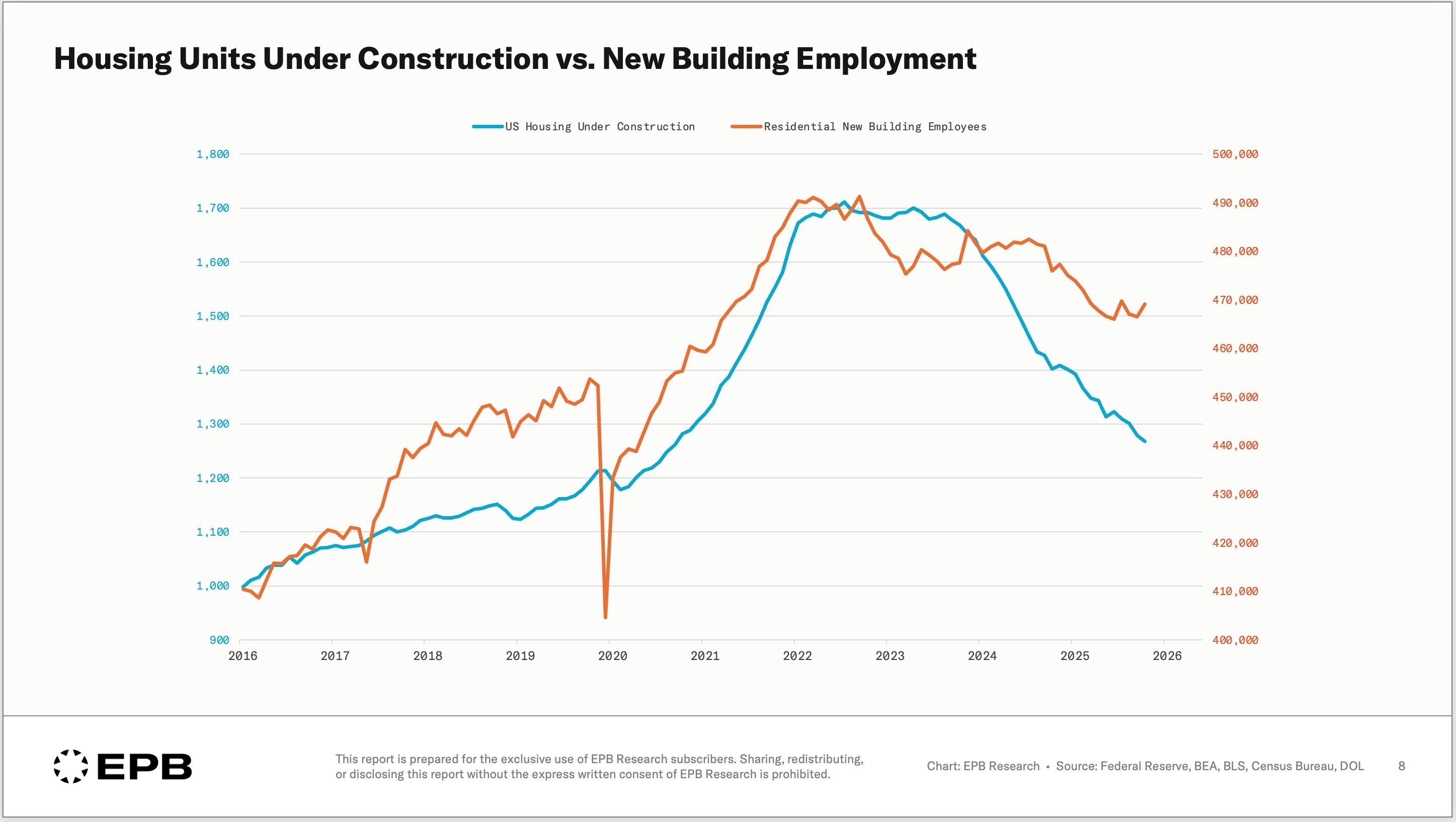

This cycle, there was a tightening of monetary policy in 2022, which led to a pullback in home sales, but construction activity continued and stayed elevated until 2024 due to the historic backlog of completed homes.

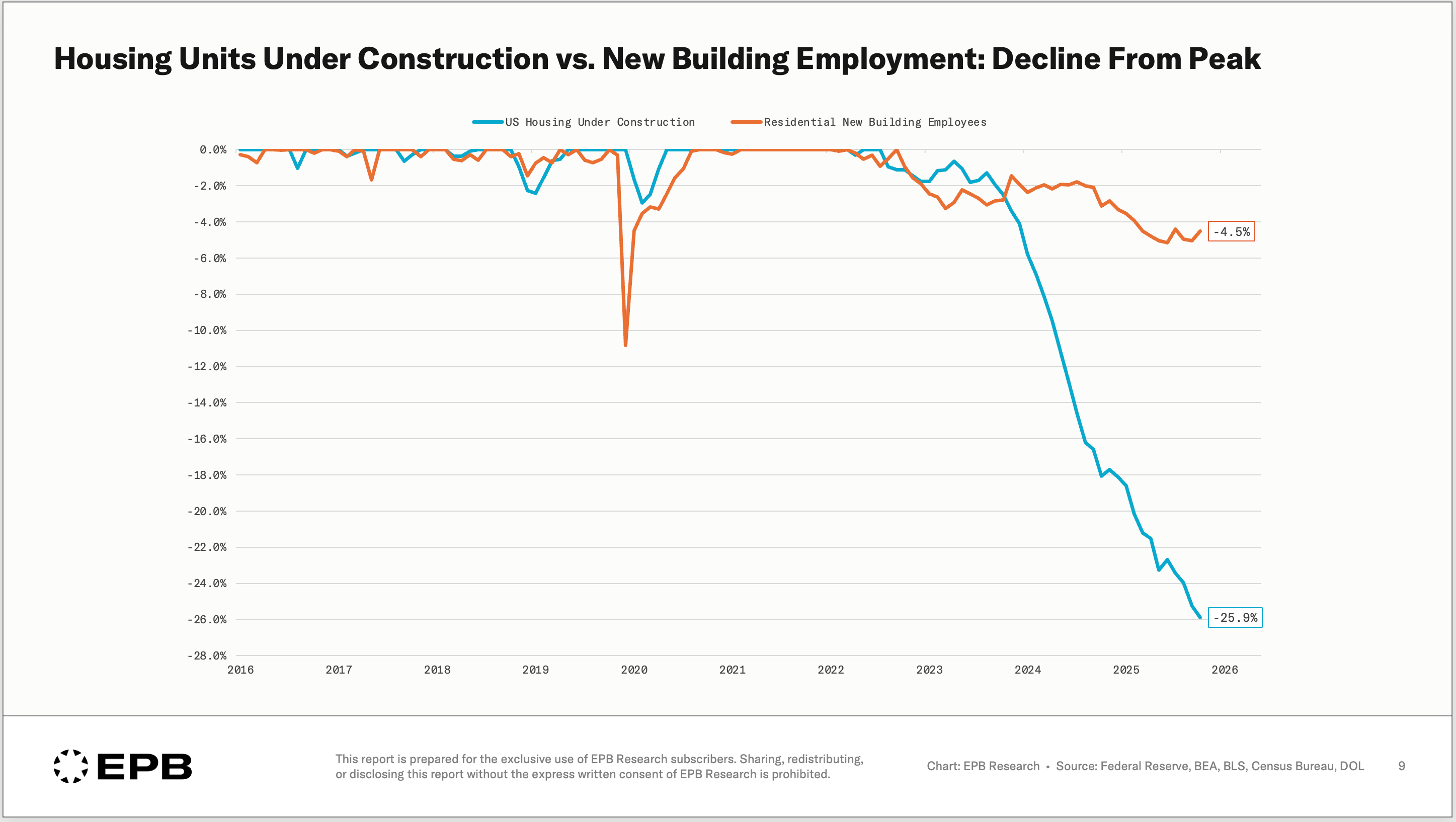

As that backlog cleared, eventually, the number of housing units under construction started to decline, and normally, that comes with a decline in residential construction employment.

This cycle, however, a nearly 30% decline in the number of housing units under construction has so far only come with a 4.5% decline in residential builder employment.

The only way for companies to have a massive drop in production volumes but a limited drop in employment is for the difference to come out of profit margins.

If a business sees activity levels decline without reducing costs, profit margins must compress, and that’s exactly what happened.

Profit margins for the largest homebuilders declined from 20.4% in 2022 to less than 12% today, an 800bps decline in margins.

What’s been unique is that because margins started at 20%, builders were able to stomach the 800bps hit to margins without panicking.

At any other point in history, that magnitude of margin compression would have been too much to handle.

Before the pandemic, profit margins were highly stable at 10%. An 8% decline would have put profit margins at 2%, leading to a massive reduction in jobs. But this cycle, an 800bps decline in margins has left builders still in a more profitable position than they were from 2012 to 2020.

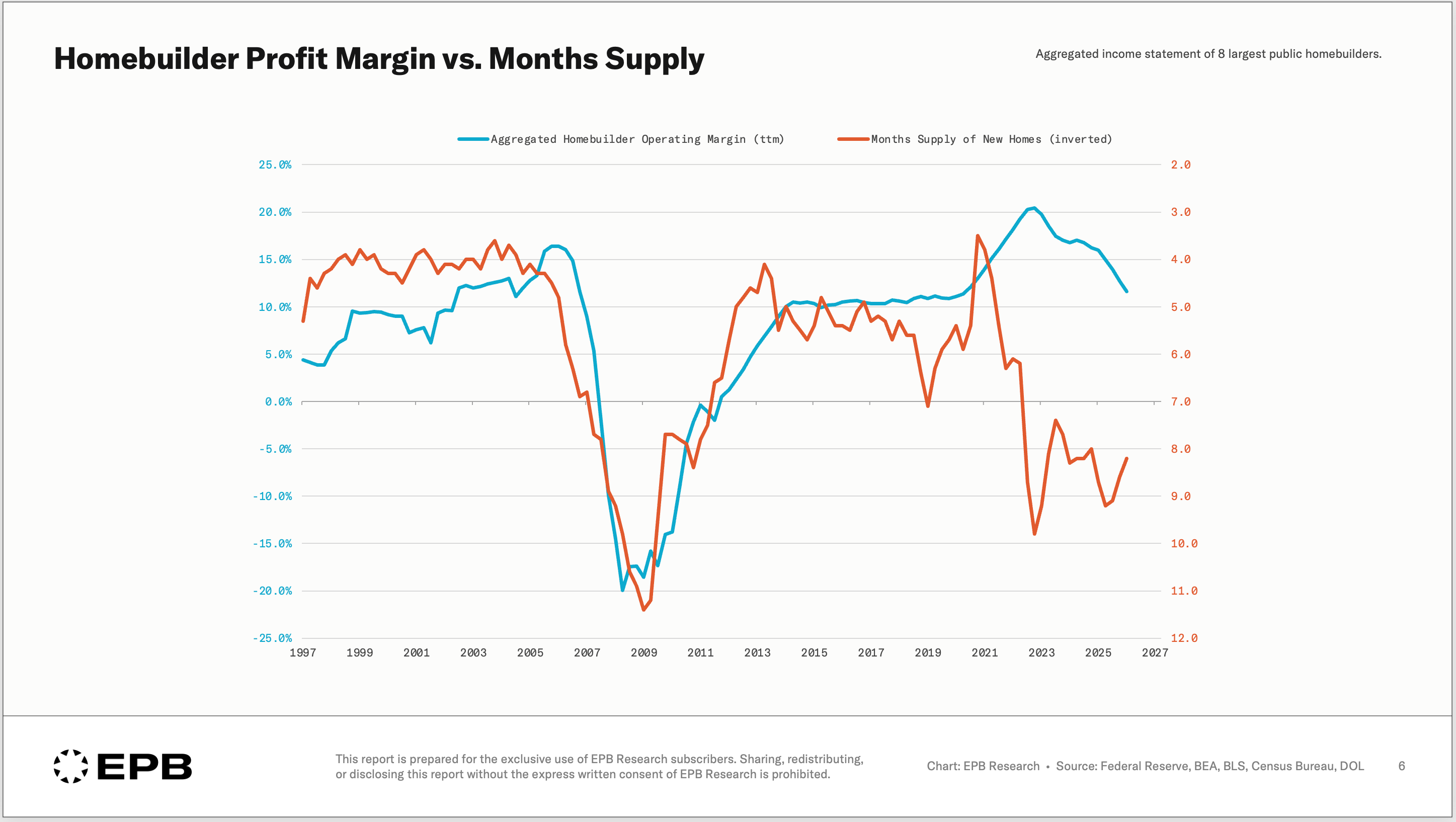

Historically, the standard months supply measure, inverted in this chart, has been a leading indicator of profit margins, but it decoupled in 2022.

The completed months supply measure, inverted, has been equally as good in the past, and did not decouple in 2022.

Builders are increasingly carrying more of their inventory as completed, which is a more expensive situation than carrying raw land, putting more pressure on the already declining profit margins.

And with the affordability problem in the housing market still extreme, the pace of new home sales will remain sluggish, forcing companies to continue reducing construction activity or carry even more completed inventory.

In either case, the residential construction cycle still hasn’t turned higher. It’s been the same cycle since 2022, just massively drawn out by major construction backlogs and extreme profit margins in the aftermath of the pandemic.

The broader economy will be relatively unimpacted until we see the cycle play out further in residential construction, with material job losses, because it’s the early-stage job losses in sectors like construction that create the problems for the rest of the economy.

Our free Residential Construction Cycle guide walks through the full housing sequence - step by step.

It is the deeper framework behind the completed months supply metric and the signals that come before and after it.

When you download the PDF, you also join our free weekly newsletter, which provides updates on our entire process and framework, along with some more business cycle teachings.

If you found this report helpful, please consider sharing it with your network!

Why profit margins were not hit given the 800 bps. compression in operating margins? "But this cycle, an 800bps decline in margins has left builders still in a more profitable position than they were from 2012 to 2020." Why were they more profitable than before the op. margin compression?

The completed months supply reframe is one of the more useful methodological corrections I've seen applied to housing cycle analysis — it's a clean example of how a reliable indicator can produce a false signal when the underlying composition shifts in a way the metric wasn't designed to capture. The pandemic supply chain disruption essentially broke the historical relationship between inventory counts and actual market pressure, and builders were rational to keep building through it given the backlog. What's worth sitting with now is the margin compression story: 800 basis points off peak sounds alarming, but the fact that builders started from 20% means they're still operating above their pre-pandemic norm — which is exactly why employment hasn't cracked yet. The signal to watch isn't the margin decline itself, it's the rate at which completed inventory is accumulating relative to sales velocity, because that's what will force the employment adjustment the cycle hasn't delivered yet. Are you seeing the completed months supply metric diverge meaningfully across regions, or is the pressure fairly uniform at this point in the cycle?