The Economy Has 158 Million Jobs. Less Than 15% Matter For Recessions.

Most analysts watch total nonfarm payrolls and see stability. A narrow slice of the labor market generates virtually every recessionary job loss — and it peaks years before anyone notices.

If you wait for total nonfarm payrolls to turn negative before calling a recession, you will be right every time, but useful none of the time.

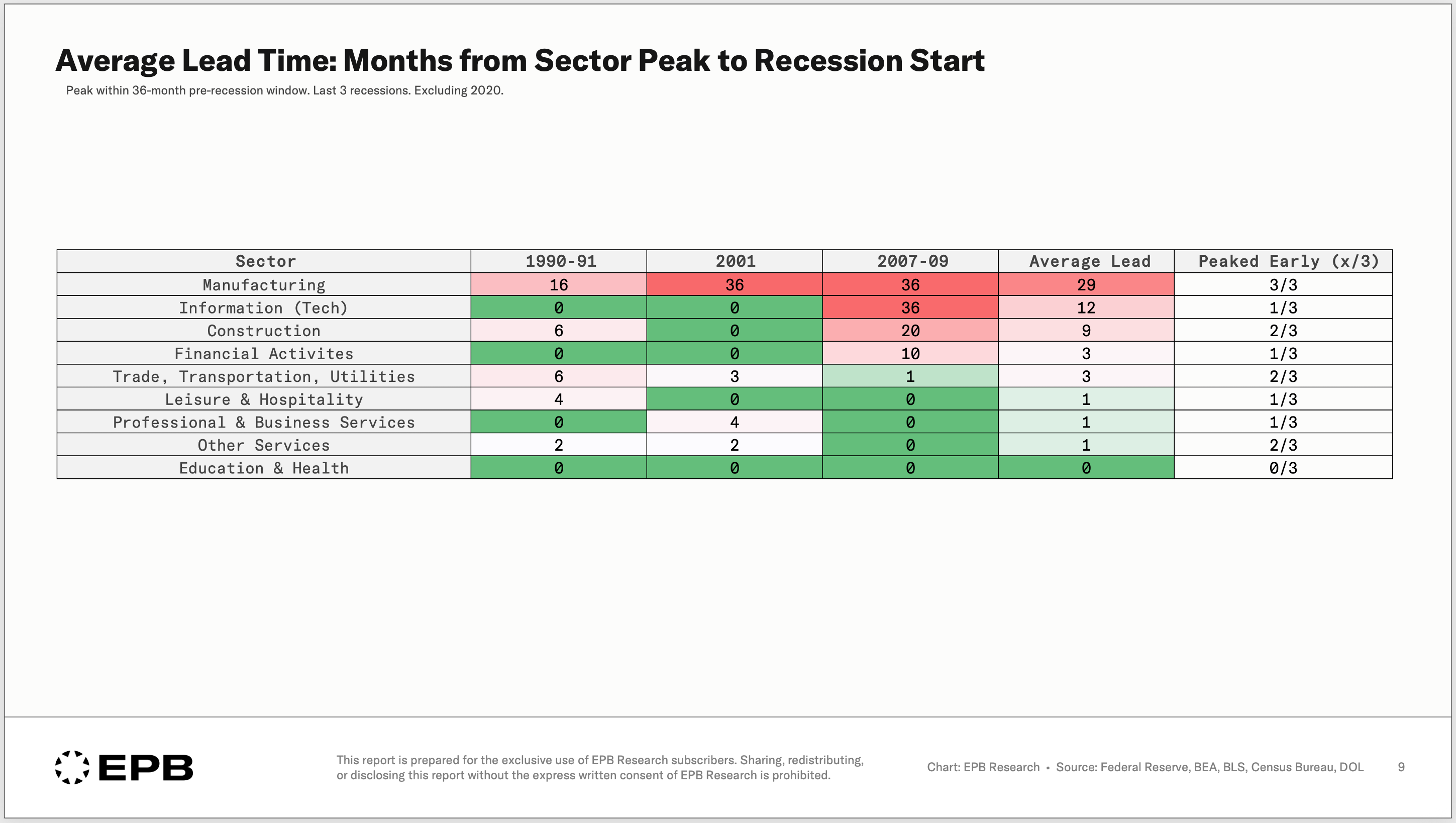

Across the last three recessions, manufacturing jobs peaked an average of 29 months before the downturn officially started. Construction jobs had an average lead time of 9 months.

The headline number gives virtually zero warning.

The economy has 158 million payrolls, but only 13% of them really matter for recessions.

Construction and manufacturing are the 21 million jobs in the economy responsible for nearly all the booms and busts. They account for virtually 100% of private-sector job losses in recessions and have the longest average warning signal. They move first, and they move the most.

To see this framework applied to current data every week, join the free EPB Research newsletter.

When you sign up, you also get our free Housing Cycle Guide, which shows you the exact sequence of how job losses develop in the residential construction sector - the most important sector in the economy.

In this post, we will highlight the importance of construction and manufacturing jobs as the driver of recessions, and your best warning signal, and why focusing on total payrolls or even the larger service sector jobs is a horrible idea.

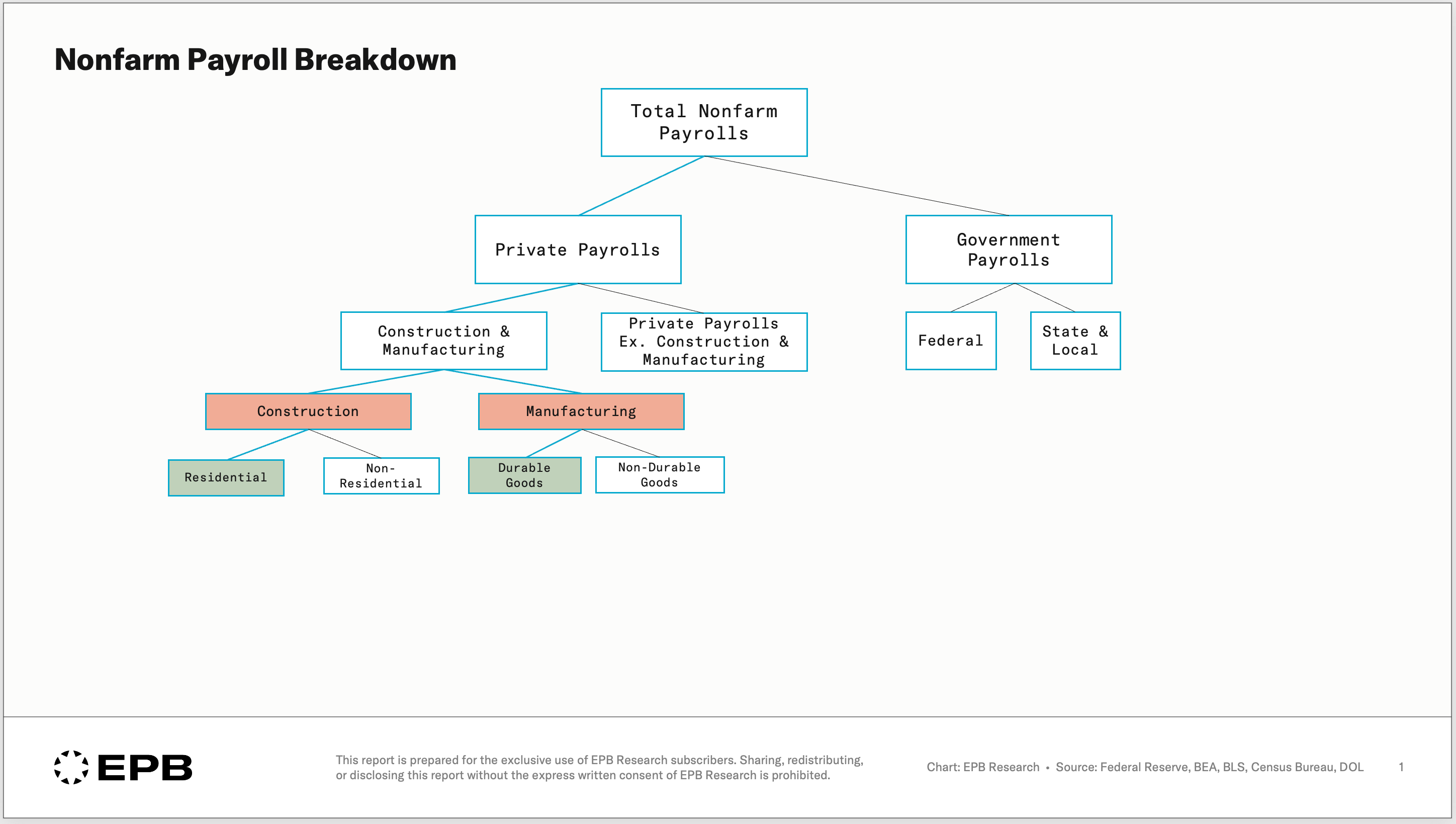

Breaking Down Nonfarm Payrolls

Total nonfarm payrolls can be split between government and private-sector jobs.

Within the private sector, there are 9 major sectors. This chart shows a flowchart of nonfarm payrolls, peeling back the layers to arrive at the most important areas of the labor market.

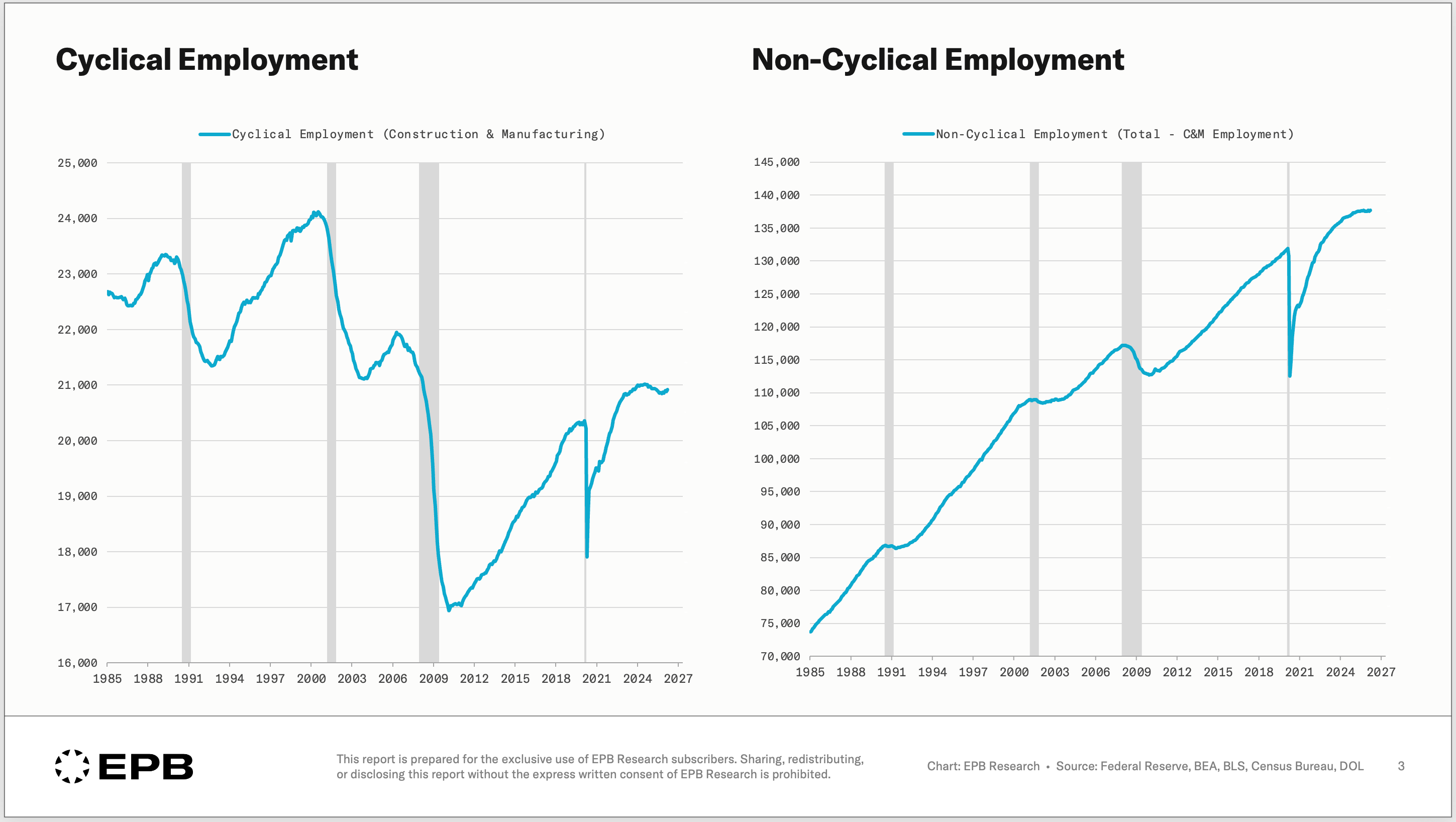

After the split between private jobs and government jobs, there are cyclical jobs (construction & manufacturing) and everything else, or non-cyclical jobs.

There’s another layer below both construction and manufacturing - the split between residential and non-residential, and the split between durable goods and non-durable goods.

Before getting too specific, we have to establish why construction & manufacturing jobs are the only sectors that truly matter for recessionary developments.

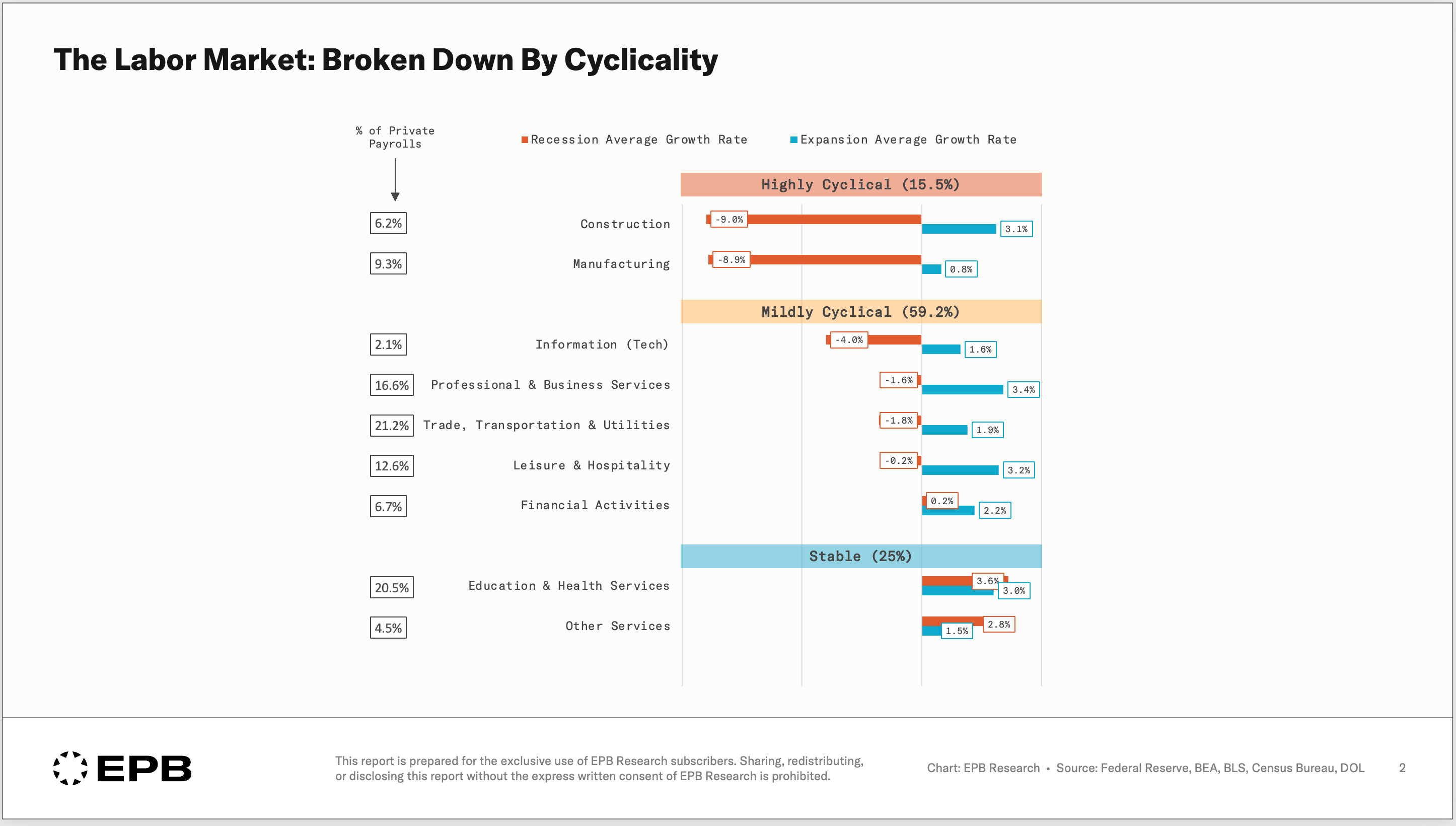

This chart shows the 9 main private-sector categories and their respective average growth rates during expansionary and recessionary periods.

The difference between the average expansionary growth rate and recessionary growth rate is what we call the expansion-recession spread.

Construction has the largest spread, over 12%, closely followed by manufacturing. Together, these two sectors are only 15.5% of private payrolls, but the volatility or the difference in behavior during expansions and recessions is way larger than any other sector in the economy.

60% of the private sector labor market is what we’d call mildly cyclical - showing a modest spread in performance between expansions and recessions.

The remaining 25% of the private sector labor market is completely stable, showing virtually no difference in performance between expansions and recessions, with the largest component of this group being education and health care services.

Construction and manufacturing are clearly in a category of their own, driving all the cyclicality or all the booms and busts, while the rest of the labor market, over 100 million jobs, experiences very little decline during recessions.

Hiring conditions may change for these non-cyclical jobs. There may be times when it's harder or easier to get hired, but massive and sustained job losses in these categories are a byproduct of the damage in the cyclical sectors, not a warning signal.

15% of Private Sector Payrolls. 100% of the Job Losses.

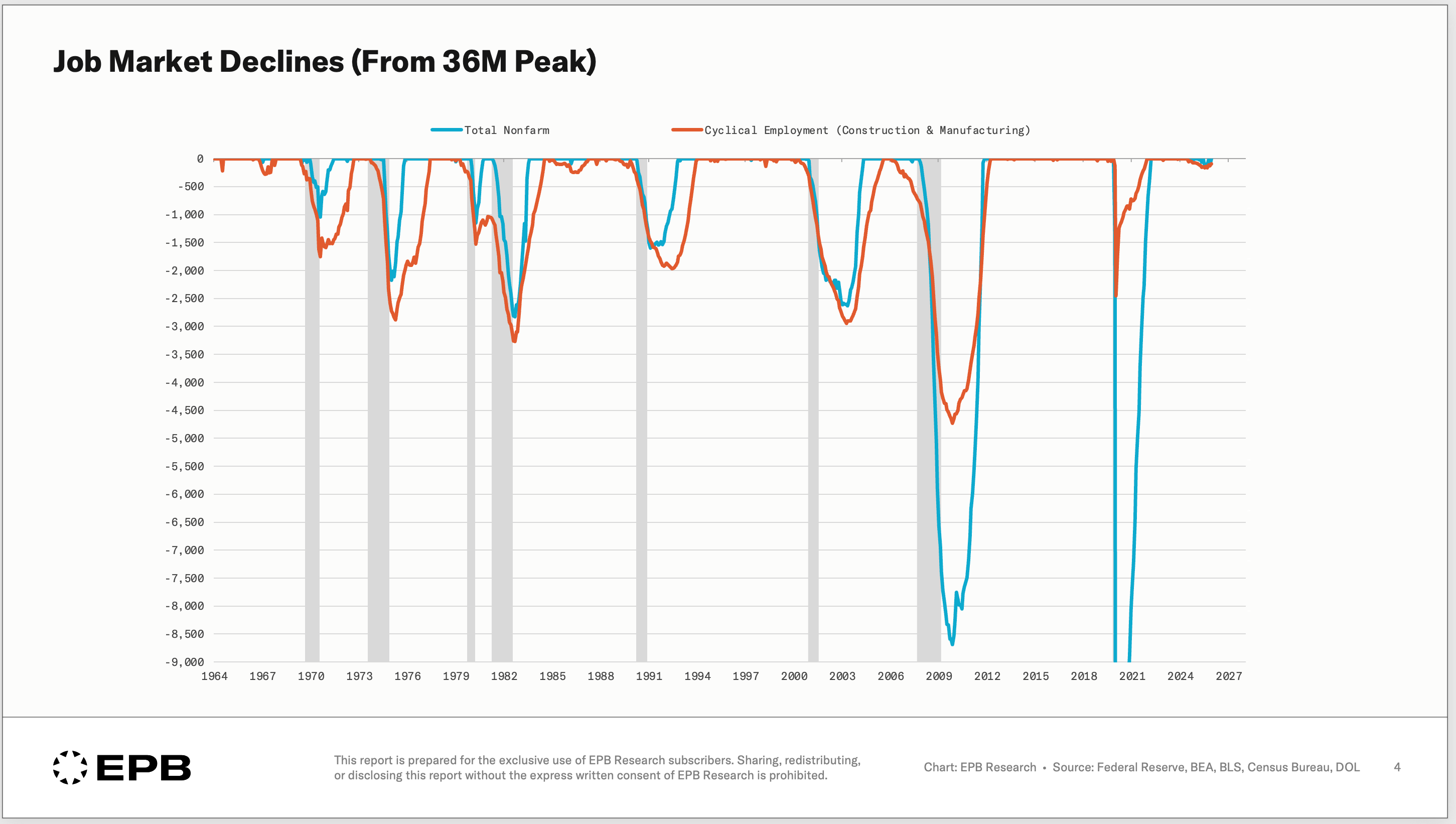

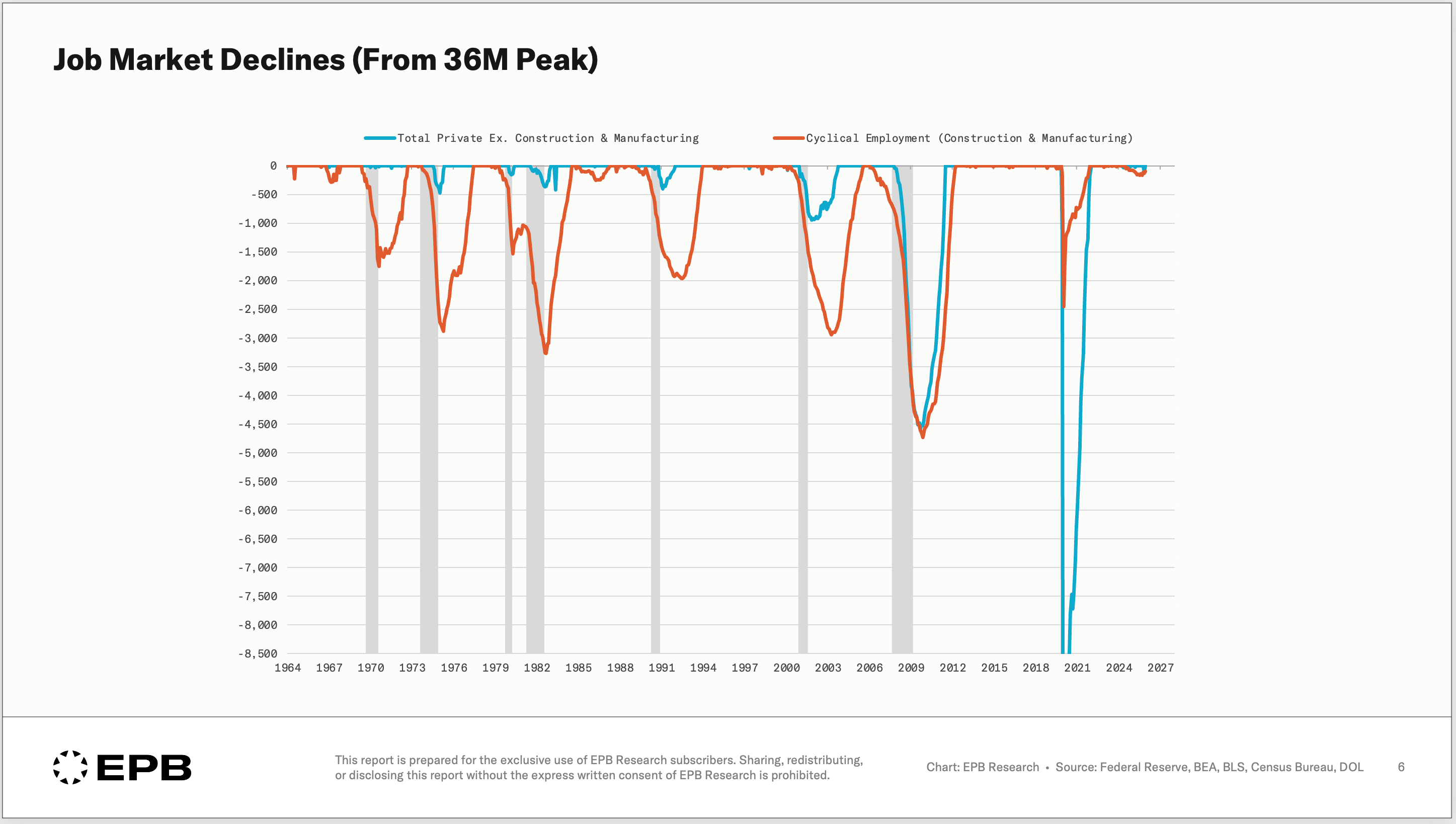

This chart plots the decline in construction and manufacturing jobs and in all jobs.

In every recession from 1970 through 2001, construction and manufacturing lost more jobs than the rest of the economy. That means all jobs, excluding construction and manufacturing, actually added jobs through the recession.

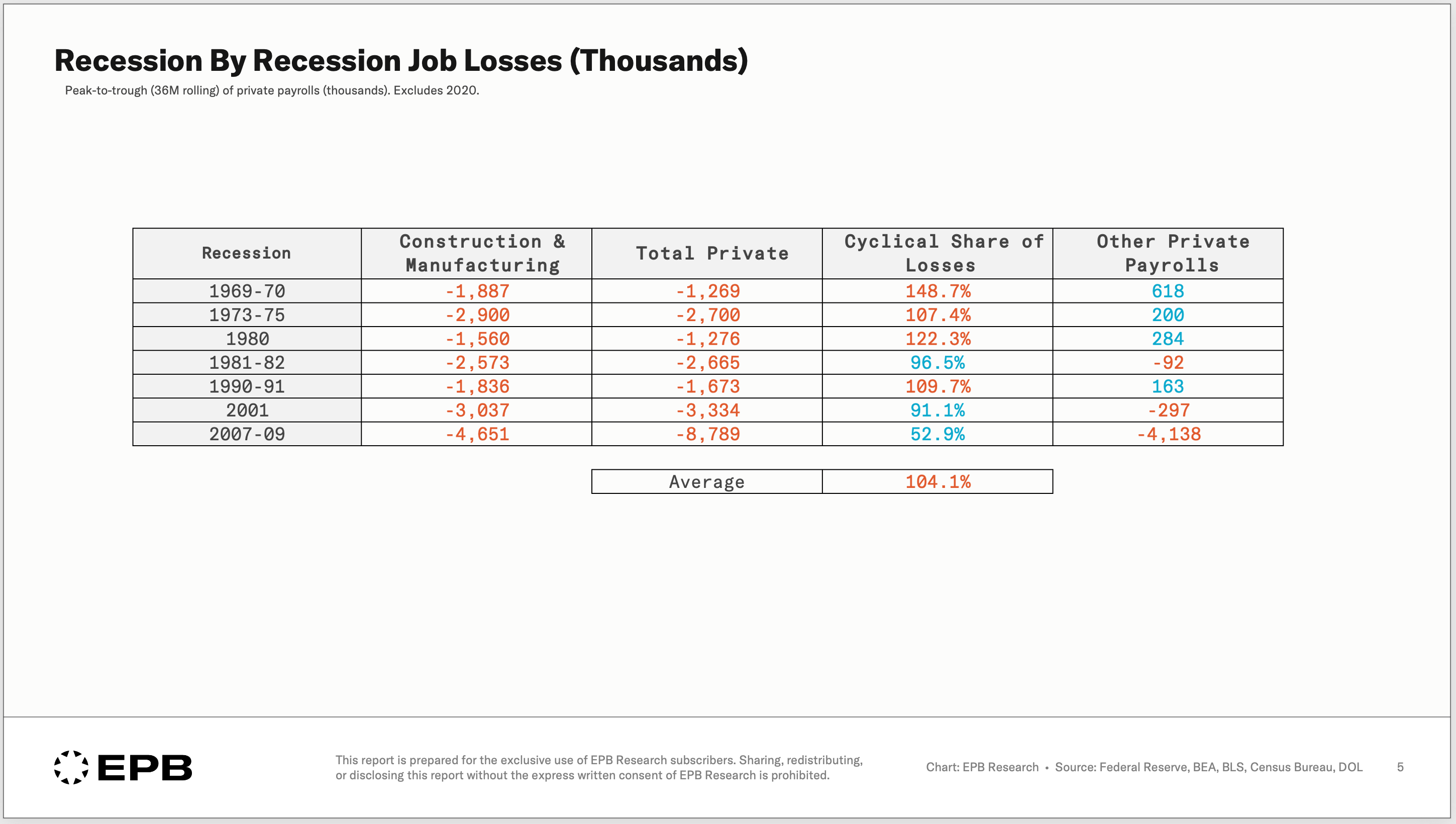

This table shows the total job losses in construction & manufacturing and the total private-sector job losses in each recession.

In four of the last seven recessions, cyclical jobs accounted for more than 100% of private sector job losses.

In two of the last seven recessions, cyclical jobs were more than 90% of total job losses.

The 2008 financial crisis showed that cyclical jobs accounted for 52.9% of private-sector job losses, but only because the recession became so severe and morphed into a banking crisis, which led to job losses everywhere.

Even so, cyclical jobs accounted for 53% of all job losses, even though they represented just 18% of private jobs at the end of 2007.

If the importance of construction and manufacturing jobs over everything else is not already clear, this chart shows cyclical job losses and job losses for all private jobs excluding construction and manufacturing.

The importance of a sector, particularly for the labor market, is not tied to its size. Just because we are a services economy by size, does not mean those jobs matter more for the business cycle.

Just because construction and manufacturing account for only 13% of private payrolls today doesn’t mean they won’t account for more than 50% of all job losses in the next recession.

Big Doesn’t Mean Important. Most Sectors Never Decline

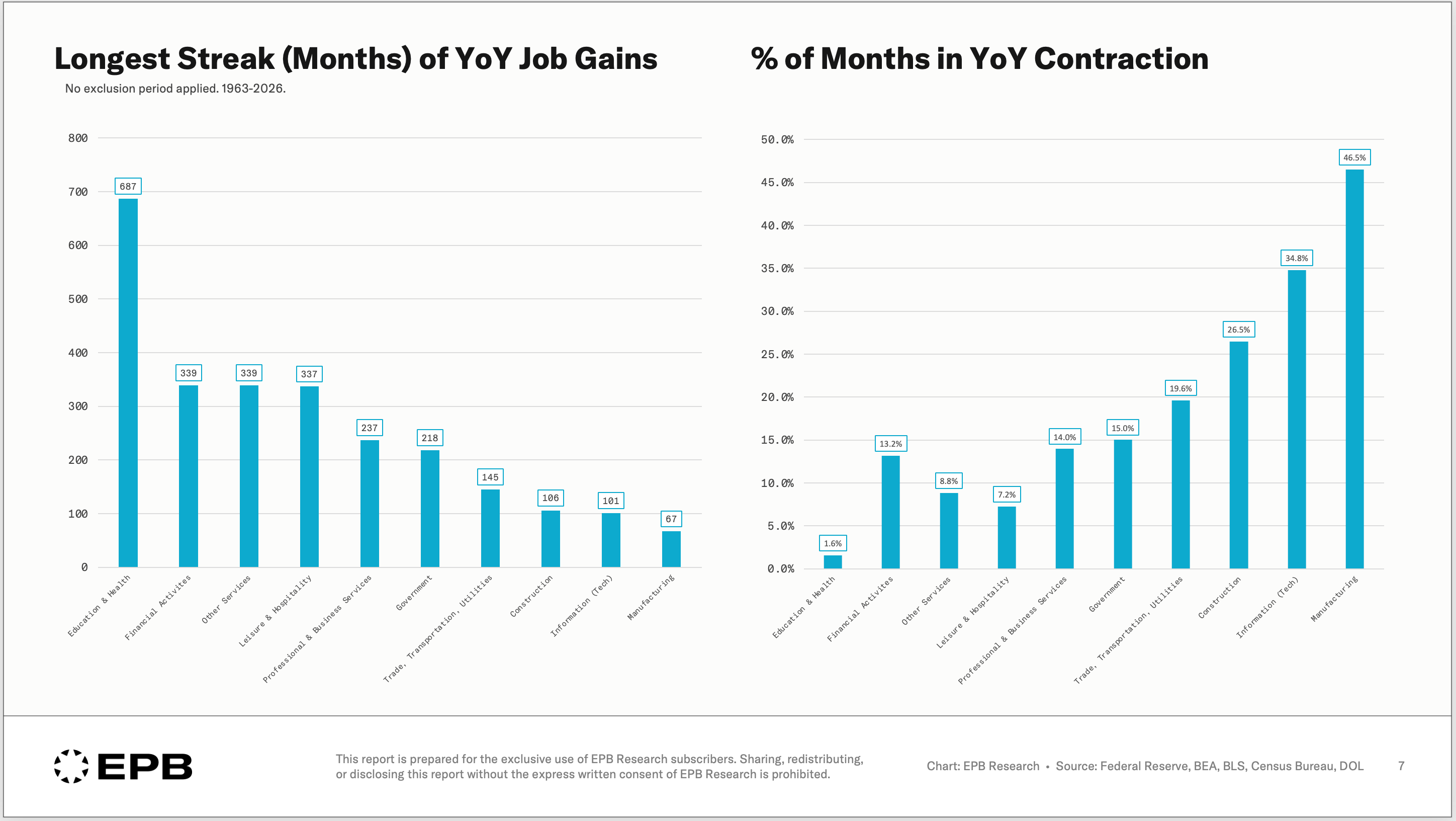

This chart shows the longest streak each sector has had without year-over-year job losses on the left, and the percent of time each sector spends in contraction on the right.

Important in this context doesn’t mean socially important; it means important for business cycle dynamics.

Education and healthcare jobs had a streak of 687 months without year-over-year job losses, which is over 57 years! The streak would have been even longer had it not been for the pandemic.

Education and healthcare jobs have only contracted in 1.6% of months since 1963.

Compare this to construction, which had a max streak of 106 months and contracts 26.5% of the time, or manufacturing, which has a max streak of 67 months and contracts almost 50% of the time.

Since we know there are sectors that virtually never contract, why include them in the analysis of cyclical or recessionary dynamics? Their stability dilutes the signal, under the hood, that develops in the more volatile, economy-sensitive sectors.

Construction and manufacturing move the most, and they move first. This is the signal.

Construction & Manufacturing: Your Best Warning Signal

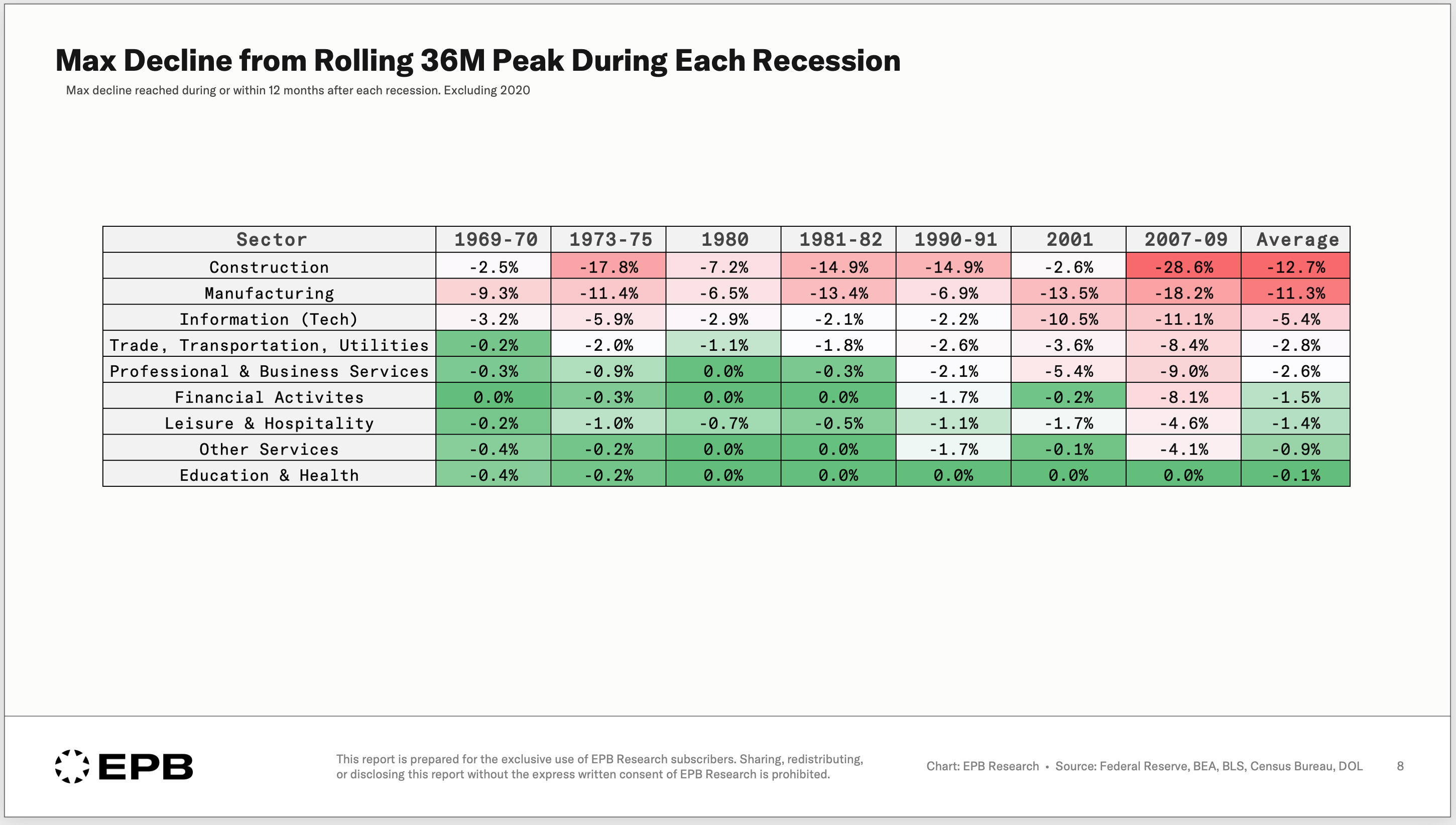

From peak to trough, across seven recessions, construction jobs declined an average of 12.7%. Manufacturing declined 11.3%.

The next-closest sector in terms of percentage decline during recessions is information technology, with an average of 5.4%.

Financial activities, leisure and hospitality, education, healthcare, and other services all show an average decline of less than 2%.

Construction and manufacturing clearly decline the most.

They also decline the earliest. Manufacturing jobs peaked ahead of the last 3 recessions with an average lead time of 29 months. Some of this is due to the secular decline in manufacturing jobs, but even normalizing for that factor places manufacturing at the top of the list in terms of lead time.

Construction jobs peaked an average of 9 months ahead of the last three recessions, with a 20-month lead time ahead of the 2008 recession.

Technology ranks second on this list, but it only declined ahead of 1 recession, 2008, and this was still an artifact of the 2001 recession, when the tech sector shed jobs for over a decade straight, so this is not a reliable signal.

The point is that construction and manufacturing jobs decline the most, decline earliest, and provide the only true cyclical or recessionary signal in the labor market.

Key Takeaway & How To Monitor The Labor Market

Construction and manufacturing account for just 13% of private payrolls today, but those 21 million jobs are the most important in the entire economy in terms of business-cycle or recessionary signals. The rest is noise.

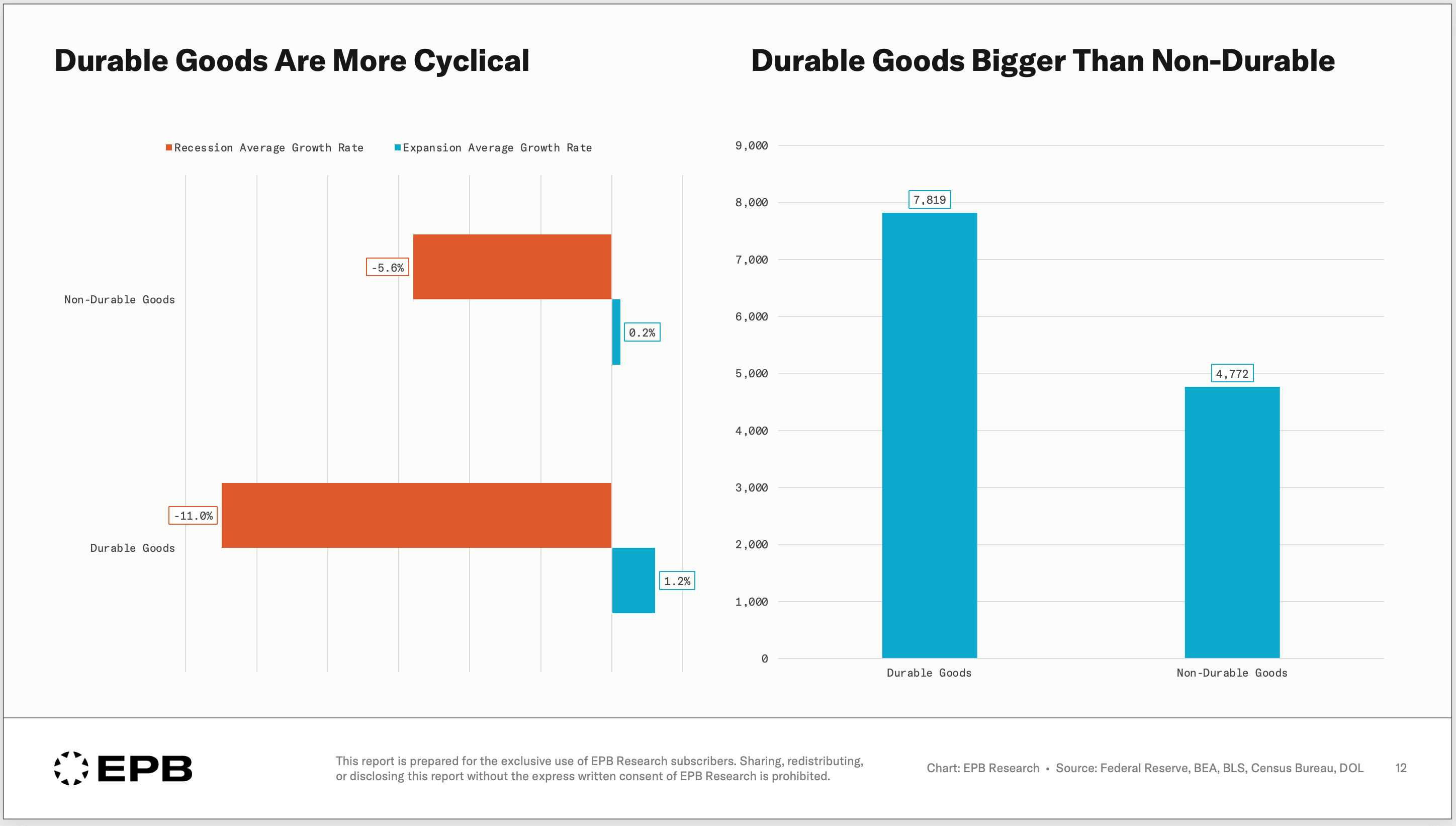

Within construction and manufacturing, we can narrow it down even further.

Durable goods have a much larger expansion-recession spread than non-durables, 12.2% versus 5.8%. Durables also carry 7.8 million jobs compared to 4.7 million for non-durables.

Durable goods are more cyclical and larger than non-durable goods and thus, the more important component within the manufacturing sector.

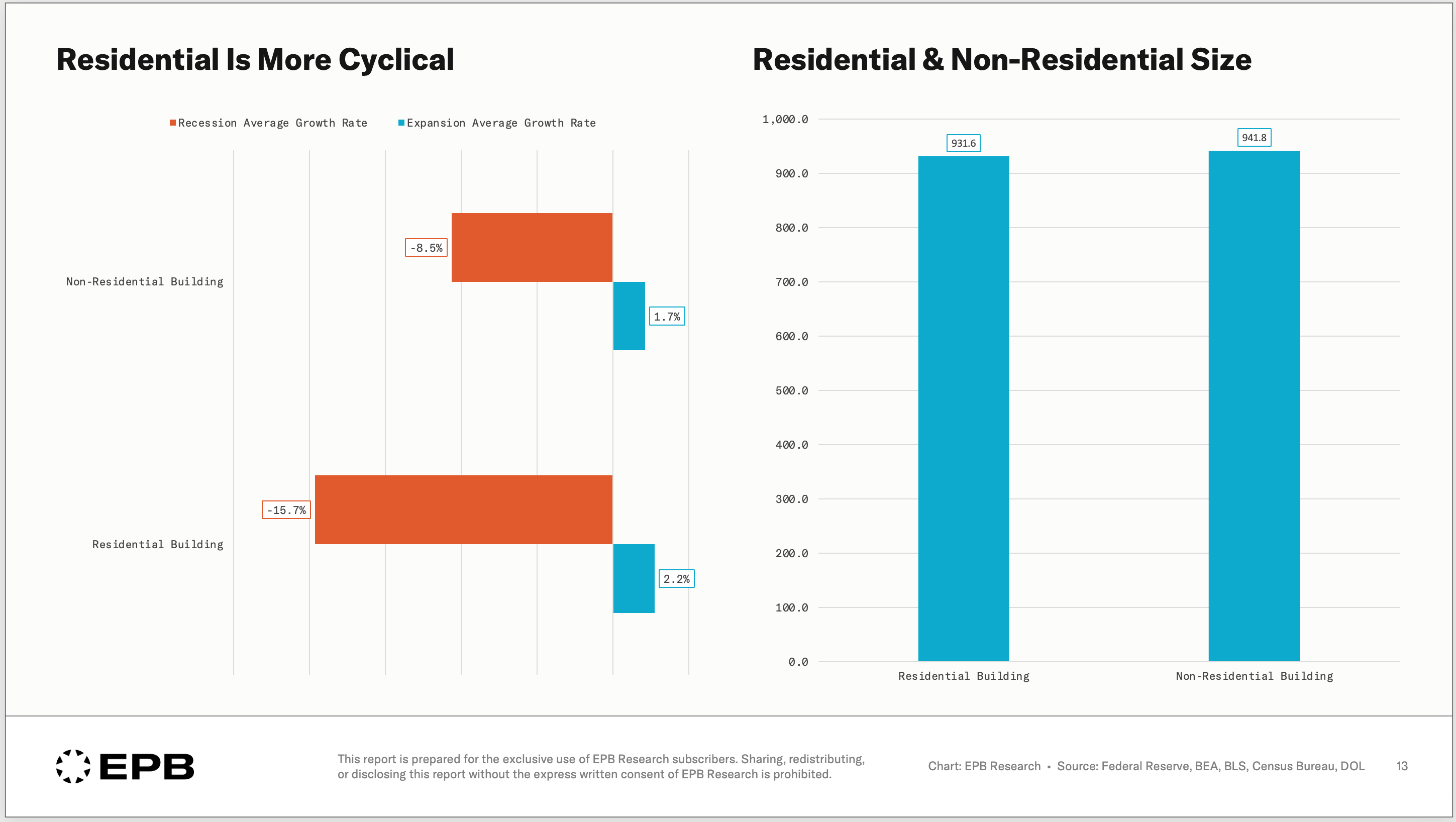

Residential building and non-residential building each hold a bit less than 950,000 jobs - almost the same size.

But residential jobs are far more cyclical, carrying a much larger expansion-recession spread.

Residential construction is more interest-rate-sensitive and faster-moving than non-residential construction, making it a more important focus within the construction sector.

The economy has 158 million payrolls, and the jobs report the media scrutinizes each month treats all these jobs as equal.

The business cycle runs on the narrow slice of construction and manufacturing jobs that account for up to 100% of all job losses during recessions, with residential construction and durable goods manufacturing driving the biggest swings.

Focusing on the headline numbers will never provide an early warning sign, as the important cyclical signal is buried by non-cyclical jobs like education and health care, which can go 50 years without contracting.

At EPB Research, we focus on the construction and manufacturing portions of the labor market in detail, uncovering signals within residential construction and durable goods manufacturing that provide the earliest warning signs the business cycle has to offer.

To see this framework applied to current data every week, join the free EPB Research newsletter.

When you sign up, you also get our free Housing Cycle Guide, which shows you the exact sequence of how job losses develop in the residential construction sector - the most important sector in the economy.

Excellent. Well written.

Appreciated if you could take that further beyond the historical observations and into the contextual present?

Challenge for the weekend perhaps?!